Current Summary: Today, we find that the U.S. financial media has started to pay widespread attention to the inversion problem in the two-year and ten-year U.S. Treasury yields. Today, the high number stands at nearly 50 basis points, the highest since August 2000, and this number has been a consistent, well-tested, and never-missed measure of U.S. recession. That is why the economic establishment has been playing the Fed off .

And the reason for the sudden expansion of U.S. debt differentiation has been introduced for the past two days, that is, there has been a large amount of money withdrawn from U.S. debt. Unlike last weekend, although there was money left the market, there will still be different funds coming into U.S. debt after the U.S. stock market opened. After all, the current yield is already very high, the default of U.S. debt may be too low, so buying U.S. debt is almost risk-free, and U.S. debt is very deep in the secondary market ,

That suggests that money will have little to lose in terms of principal if it wants to get out early, especially for many large companies that have Treasuries in their pockets. And from yesterday's opening of U.S. stocks to now, there is almost no trend of money entering U.S. Treasury bonds, and on the contrary, U.S. Treasury yields are still rising. Even if the two- and three-year periods are slightly down, the relative increase is a drop in the bucket.

One-year Treasury bonds, in particular, have gone from being the highest yields ever, and I even looked at the domestic banks' earnings, and the 3.3% R1 risk-free yield for a year was virtually non-existent, and I believe that this yield would be snapped up even at home, but it went from nowhere in the United States, to still rising this morning. In this case, it is clear that a large amount of money has been leaving the Treasury market.

And the direction of funds also needs to be constantly concerned, if entering the precious metals market, gold is a good target, it is also the main haven asset in times of macro changes, such as the Russia-Ukraine conflict just occurred when the price of gold rose sharply. But as things stand, gold is not rising, so we can rule it out.

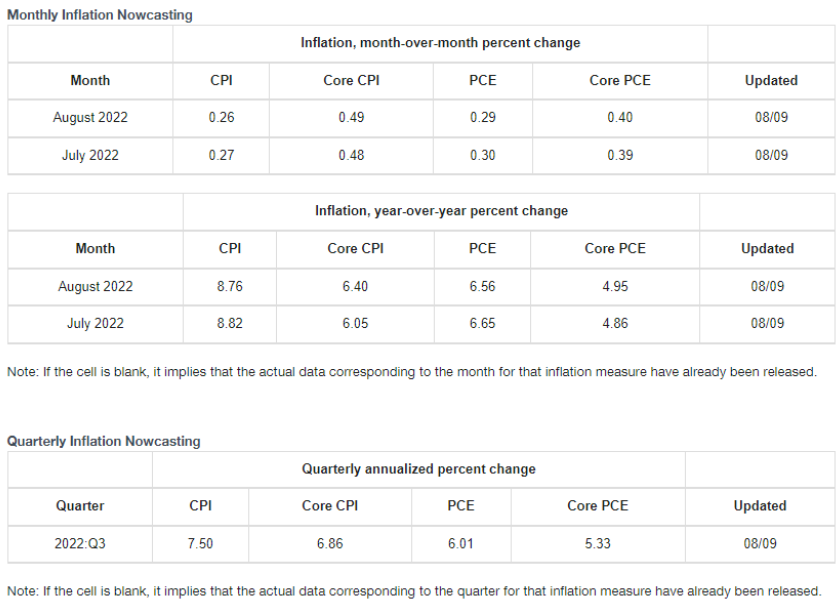

Then whether this money has entered the risk market is not clearly seen in the stock market, but the currency market can be confirmed by stabilizing the value of the currency. As of 8 am this morning, the market capitalization of USDT and USDC USDT shows no sign of increasing, while USDC is in a small selling position. Therefore, we can see that the funds out of U.S. Treasury bonds have no signs of entering the currency market, which also confirms that the funds in the currency market are still not improving. As yesterday's tweet said, the current market capitalization of money is sufficient to push BTC and ETH prices to their highs of 2021. But the reason prices have not moved up or down is not because of the money leaving the market. Rather, it is because more of the money sitting on the market does not want to turn into purchasing power. And that is precisely because the macro situation, particularly the Fed's attitude to higher interest rates, is what determines the flow of money. It is already clear that 20:30 p.m. this time, the inflation data will be released. This time, the CPI data again will determine the Fed's attitude in raising interest rates recently. More importantly, it is more important that whether or not "inflation peaked" was actually achieved. After all, when inflation reached a near 50-year high of 9.1% in June, risk markets actually rose because inflation expectations, especially those implied by the current US president, had pushed risk markets into a collective bargain.

But there was no clear indication that inflation was peaking, though the latest two days' forecasts do show a fall from around 8.9% to around 8.7%, especially after last month's experience, when bad numbers led even the White House to write that things could get worse and to inoculate markets in advance. Today, inflation data are available in less than eight hours, but there is still no official warning. This implies that the greater probability is that the aggregate (annualized) value of CPI is more likely to fall, while the annual value and the core CPI are more difficult to achieve. The core CPI, in particular, is not falling, but is likely to rise, especially given the strength of non-farm data. The Fed's interpretation of inflation this time will be unclear, so more attention will need to be paid to tonight's data, but a 75-year rate hike in September is already high expectations. A 75-basis-point rate rise and a peak in inflation are inconsistent conclusions. After all, inflation peaking is not a real concern at the moment; it is a bet that the Fed has already begun to slow down rate hikes, but is now even threatening to end the year with a federal rate of 3.75-4% - deepening the economic game. Not only does this mean that a rate hike in September is still more likely, but an ad hoc meeting in August cannot be ruled out.

Therefore, due to various influences, the purchasing power of the currency has been greatly reduced. In terms of the amount of funds transferred to the exchange, USDT's funds have once again refreshed the lowest working day transfer amount of nearly half a year, which is even lower than the weekend data of the first half of the year. And if compared with 2021, the data is even further behind, while USDC's funds are still at a relatively low level although there are some signs of an increase. This also means that purchasing power is declining in both Europe and the US.

In particular, it is clear from the fund trends that the recent funds are awaiting the release of the CPI, and that the current rush into the market is not safe. But, in relation to the decreasing amount of capital, as the CPI approaches the BTC and ETH selling pressure, the trend toward higher BTC and ETH selling pressure is not only not decreasing, but also increasing, which has been previously analyzed. More chips to worry that the release of CPI would trigger a chain reaction at the Fed that would cause the currency to fall.

Therefore, more chips will be shifted to the exchanges ahead of schedule, and they will either wait for a better opportunity or they will already leave the market ahead of schedule, especially as the rumor that US stock prices fell in Twitter yesterday was due to some institutions having known ahead of time that the CPI data was higher than expected, thus causing panic among a small portion of investors in the market, which is another reason for the increase in selling pressure. But because the amount of money is really falling. Therefore, the corresponding BTC and ETH exchange turnover also showed a downward trend, more chips are stranded on the exchange. Another reminder to price-sensitive junior partners is that if they feel they can't afford a fall in prices, it may be better to switch the chips early to the exchanges. And as last month's inflation announcements showed, the big change is the data. It's interpretation. Whereas last month's near-50-year high was interpreted as a sign that inflation had peaked, so risk markets are picking up rather than falling, this time it is more the Fed's interpretation, so even unexpected changes in inflation, consistent with market-friendly or bearish interpretations, could alter the meaning of the data itself. Therefore, the long-short two-way passive selling may not happen, reducing leverage is the safest.