Prepared by Julio César Salvador

Crypto & Financial Content Writer

Introduction

India’s stock market keeps surprising us in 2025. While Wall Street frets about rate hikes, conflicts, and clogged shipping lanes, the Nifty 50 and Sensex inch higher. Why does the rally hold? Three simple drivers: a solid GDP growth, an exploding digital economy, and millions of first‑time middle‑class shoppers.

As a smart retail investor, you do not want to watch the wave from the shore; you want to ride it. After digging through balance sheets, earnings calls, and weekly charts, we have settled on two stocks that stand out.

HDFC Bank sticks to a straightforward game plan. It lends with care, keeps costs in check, and wins deposits one customer at a time. That discipline shows up in profits, quarter after quarter.

Infosys plays a different role. It helps companies around the world move to the cloud, automate the dull stuff, and trim expenses. When a client saves money, they usually come back for more, and that feeds steady revenue growth.

Owning both stocks gives you exposure to India’s two strongest growth engines: finance and technology. Together, they bring balance, resilience, and real upside potential to your portfolio.

1. HDFC Bank Ltd

Company Overview

Picture the bank that every second Indian seems to know by name. That’s HDFC Bank.

Since merging with HDFC Ltd in 2023, it has welcomed more than 120 million customers—urban professionals tapping on apps, shopkeepers in small towns, and farmers swiping cards at roadside kiosks. Indian Regulators label it “systemically important,” yet it still feels close to the ground, mixing everyday loans, corporate cash management, SME lifelines, and easy‑to‑use digital tools into one smooth engine.

Keep reading; in just a few minutes you might be itching to put your cash to work inside this banking giant.

Fundamental Analysis

Based on the latest data:

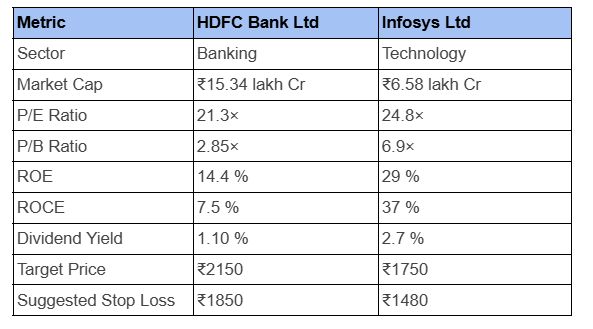

- Market cap: ~₹15.3 lakh crore

- P/E ratio: ~21.7×

- P/B ratio: ~2.8×

- ROE: ~14.4 %

- ROCE: ~7.5 %

- Dividend yield: ~1.1 %

This is what numbers show:

Think of HDFC Bank as a big, reliable engine that moves your money forward without drama. At about 22 times earnings and 2.8 times book, you pay a fair price for proven growth rather than chasing hype.

The bank earns roughly fourteen paise on every rupee of equity, well above its funding cost, and keeps bad loans to a minimum. A 1.1 percent dividend may look small, yet it has crept higher year after year and signals confidence from management. With a market value above ₹15 lakh crore and surplus capital still to deploy, you get size, quality, and headroom for profits to compound quietly while you sleep.

That combination makes it a cornerstone holding for any India focused portfolio today.

Technical Analysis

HDFC Bank trades around ₹2,000, just 1 % below its 52-week high.

Momentum is still positive:

- RSI at 59 suggests buyers still have room before the stock gets overbought

- MACD has turned positive, hinting at continued upward pressure

- 50- and 200-day moving averages sit tight around ₹1,950–₹1,970, acting as strong support

A breakout above ₹2,040, especially on strong volume, could trigger a ₹80–₹100 rally — just like it has in the past.

Buy Rationale

Here’s why HDFC Bank deserves a spot in a retail investor portfolio:

- It holds trusted leadership in private banking with a wide, balanced product range.

- The post-merger integration with HDFC Ltd strengthens its mortgage and credit franchises.

- Digital services like PhonePe and SmartWealth drive cross-selling and revenue diversification.

- Q1 2025 results exceeded expectations, with a ~12% year-over-year profit increase.

Price Target: ₹2,150 – based on continued earnings growth and valuation expansion over 6–12 months.

Suggested Stop Loss: ₹1,850 – set below recent support levels to manage downside risk.

In short: This stock gives you trusted leadership, digital strength, and growth. For any retail investor looking for stability with upside, this stock delivers exactly that.

2. INFOSYS LTD

Company Overview

Infosys Ltd isn’t just a leader in IT services — it’s one of India’s most powerful bridges to the digital future. Founded in 1981 and headquartered in Bengaluru, the company has evolved into a trusted global partner for businesses across North America, Europe, and Asia.

Today, over 300,000 employees power its solutions in cloud computing, data analytics, AI, cybersecurity, and enterprise automation. From banks to retailers, global corporations rely on Infosys to modernize their systems, boost efficiency, and protect against rising digital threats.

As Web3 adoption grows and demand for secure, scalable tech soars, Infosys is in the right place, at the right time.

For retail investors, this isn’t just a strong stock. It’s a gateway to the technologies shaping tomorrow’s economy.

Fundamental Analysis

According to recent data, these are key metrics:

- Market Cap: ₹658,000

- P/E Ratio: ~24–25×

- P/B Ratio: ~6.9×

- Return on Equity (ROE): ~29–30%

- Return on Capital Employed (ROCE): ~37%

- Dividend Yield: ~2.7%

What the numbers say about Infosys — and why it matters to you

- A P/E ratio in the 24–25× range tells us one thing: the market trusts Infosys to keep delivering profits, quarter after quarter, without wild swings.

- With a ROE near 30 % and ROCE above 35 %, Infosys isn’t just earning — it’s squeezing every rupee of capital for maximum value. That’s the kind of efficiency you want in a long-term hold.

- The ~2.7 % dividend yield offers more than just passive income. It shows management confidence and gives you real cash while the stock works in the background.

- Yes, the valuation is higher than some peers — but for good reason. Infosys offers global exposure, sticky clients, and a front-row seat to tech trends like AI, cybersecurity, and Web3.

In short: these numbers don’t just look good on paper. They tell the story of a company built for performance, stability, and long-term upside.

Technical Analysis

Current signals are mixed but leaning positive:

- The stock trades around ₹1,580, near its 50‑day EMA (~₹1,595). The 200‑day EMA sits around ₹1,660 — acting as longer‑term support/resistance.

- RSI sits near 48 (neutral), with stochastic indicators and ADX suggesting early-stage momentum.

- Overall, price is consolidating within recent ranges, hinting at a potential breakout once key levels are tested.

Target Price: ₹1,750 — based on modest earnings growth and breaching the 200‑day EMA.

Stop Loss: ₹1,480 — placed just below recent support levels to manage risk.

3. Comparison Table HDFC Bank vs. Infosys

Let’s do a quick comparison to highlight their strengths, helping you decide how each can add balance and potential to your portfolio.

Looking at the metrics above, Infosys offers investors slightly higher growth potential, with stronger profitability indicators such as a higher ROE and significantly better ROCE.

It’s clear that Infosys capitalizes efficiently on its investments, a key sign for investors seeking strong returns in the technology sector.

Meanwhile, HDFC Bank trades at more conservative valuation multiples (lower P/E and P/B), reflecting its steady, reliable performance and consistent profitability over multiple market cycles. Its lower dividend yield is typical of the banking sector, but still provides income stability.

Why Buy Both Stocks?

The rationale behind pairing these two stocks is diversification and balance.

On one hand, HDFC Bank offers steady and defensive characteristics, ideal for navigating volatile market conditions with reduced risk. On the other, Infosys provides the portfolio with exposure to rapid global technology growth, positioning investors to benefit from long-term digital transformation trends.

Combining these two stocks allows retail investors to balance safety with growth, stability with innovation, creating a more resilient portfolio structure.

4. Key Catalysts That Could Ignite a Rally in Banking & Tech

Below are three macro‑level triggers that can realistically lift both HDFC Bank and Infosys over the next 6–12 months.

4.1. Crypto & Digital‑Currency Momentum

- Stablecoins went mainstream in 2024, settling US $27.6 trillion on-chain. That’s more than Visa and Mastercard’s annual network volume combined.

- India’s own digital‑payment rails keep surging: UPI handled 18.4 billion transactions worth ₹24 lakh crore in June 2025, a 32 % jump year‑on‑year.

- The RBI’s retail e‑Rupee pilot has already signed up over six million users and crossed ₹1,000 crore in monthly volumes by mid‑2025 .

What makes this important

Greater crypto and CBDC adoption boosts demand for secure digital‑payment infrastructure. Infosys, with multiple blockchain pilots and a US $1.5 billion AI‑led digital‑transformation contract in 2025, is well‑placed to build these rails. Banks like HDFC gain float income and transaction fees as they integrate stablecoin gateways and the e‑Rupee into retail banking apps.

4.2. Government‑Driven Digital Infrastructure & Capex Boom

- India’s FY 26 budget earmarks a record ₹11.21 lakh crore for capital expenditure (3.1 % of GDP)—funds aimed at roads, rail, and digital public infrastructure (DPI).

- Global institutions call India Stack a template for inclusive growth; DPI could add up to 4 % to GDP by 2030.

Why it deserves your attention:

Large‑scale capex fuels credit demand for corporate and infrastructure projects—an immediate tail‑wind for HDFC Bank’s loan book. Simultaneously, every new digital‑public‑infra layer (eKYC, UPI, Account Aggregator) generates IT contracts that firms like Infosys routinely win.

4.3. Global AI & Tech‑Services Supercycle

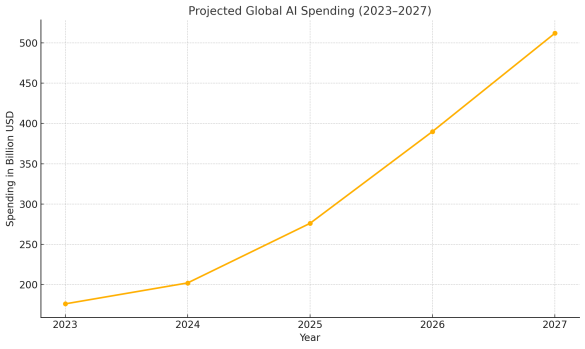

- Worldwide AI spending is forecast to reach US $512 billion by 2027, more than doubling the 2024 market size. This represents a compound annual growth rate (CAGR) of approximately 30 %, driven by strong enterprise adoption of AI, cloud, and automation technologies.

- NASSCOM expects India’s tech‑services revenue to cross US $300 billion by FY 26, up from US $282 billion in FY 25.

- Infosys continues to secure mega deals—such as a US $1.5 billion, 15‑year AI‑transformation contract announced in 2025—illustrating sustained demand for Indian IT expertise.

Projected global AI spending from 2023 to 2027 (in billion USD). Chart created by Julio Salvador based on IDC data.

Where the opportunity lies:

As global enterprises modernise with AI and cloud, Infosys captures high‑margin projects while HDFC leverages advanced analytics to sharpen credit scoring and cross‑sell. The tech‑services boom therefore reinforces growth in both sectors.

Bottom Line for Retail Investors

Crypto adoption, record government investment in digital infrastructure, and the global rise of AI are building powerful growth paths for both India’s top private bank and its leading tech giant.

Owning HDFC Bank gives you a stable, low-volatility position in India’s booming credit and payments market. Infosys, on the other hand, connects you directly to global digital transformation spending, including high-margin AI and cloud projects.

They create a portfolio that boosts your assets by earning passive income, growing in value, and giving you exposure to trends that are shaping the future of money.

4. Conclusion & Recommendations

Summary of findings

HDFC Bank provides steady income, strong risk management, and resilience through India’s economic cycles. Infosys brings a clear growth engine powered by global demand for cloud services, artificial intelligence, digital transformation, and decentralized finance.

Sector outlook for late 2025‑2026

Industry body NASSCOM projects India’s tech‑services revenue to top $300 billion in FY 2026, up from $282 billion in FY 2025, as enterprises accelerate AI‑led spending and expand global‑capacity centres.

Parallel to that, blockchain and DeFi markets are forecast to grow at compound rates above 40 %, with stable‑coin transaction volumes already overtaking Visa in 2024, signalling a long‑run tail‑wind for firms building and securing digital infrastructure.

This backdrop supports a fresh leg of IT demand that should benefit leaders like Infosys, while increased digital‑payments penetration strengthens the retail‑banking franchise of HDFC Bank.

Tips for retail investors

- Start small, scale in: use staggered purchases to average entry price.

- Reinvest dividends: compound growth by automatically reinvesting payouts.

- Review quarterly results: track loan‑growth trends for HDFC Bank and large‑deal wins for Infosys.

- Diversify beyond two names: add ETFs or bonds to cushion unforeseen shocks.

Risks and cautions

- Global slowdown could curb tech spending and loan growth.

- Currency fluctuations affect Infosys’s dollar revenue and HDFC Bank’s foreign borrowings.

- Regulatory shifts (RBI policy, data‑privacy rules, crypto taxation) may alter sector dynamics.

Miss the train, and you might be chasing higher prices later

The time to act is now.

✍️ Written by El Salvador CopyBiker — Crypto Content Specialist.

Helping your audience actually understand your Web3 product (no PhD required).