A few weeks ago, I was writing an educational article for a DeFi client. Topic? Crypto lending vs Staking.

Simple, right? So I did what most writers do: I opened Investopedia to double-check a few facts.

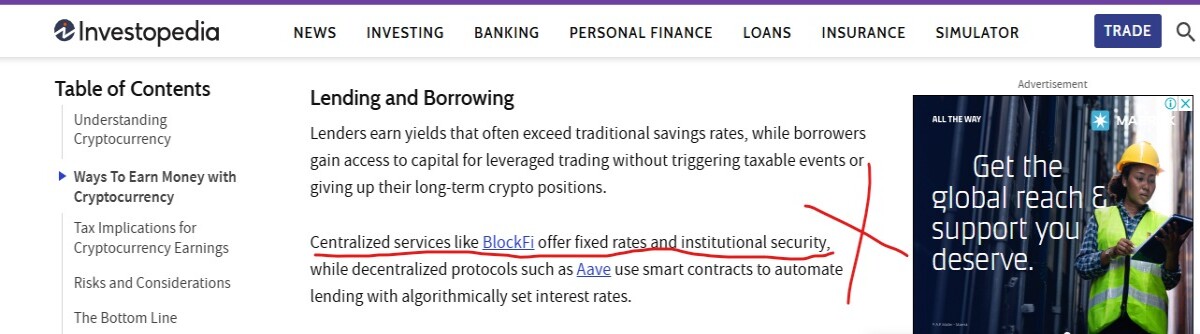

I mean, it's Investopedia. The holy bible of financial education online. They have credibility, traffic, authority... and then I saw this line:

"Centralized services like BlockFi offer fixed rates and institutional security."

Excuse me, what?

I had to blink twice. I checked the date. Refreshed the page. Nope—this wasn’t 2021. It was 2025. And yes, they still had BlockFi listed as a valid crypto lending platform.

Let me break down why that made me cringe with secondhand embarrassment.

BlockFi Wasn’t Just a Bad Pick—It Was a Cautionary Tale

What BlockFi Promised vs What Actually Happened

BlockFi was once a major player in the crypto lending game.

Retail investors could deposit BTC or USDC and earn interest.

It looked safe. Almost boring. Like the crypto version of a savings account.

But under the hood?

-

Exposure to Three Arrows Capital and FTX

-

Zero transparency in fund management

-

Big centralized decisions with client funds

And of course… everything came crashing down.

SEC Said: Enough. Here’s $100 Million in Fines

In 2022, the U.S. Securities and Exchange Commission came knocking. Turns out BlockFi had been operating without registering as an investment company under the Investment Company Act of 1940.

They had to:

- Pay $100 million in penalties

- Register their crypto lending product

- Shut down retail access in the U.S.

That was the beginning of the end. Eventually, BlockFi filed for bankruptcy. Users were left hanging. Some are still fighting to get their funds back. So no—BlockFi does not “offer fixed rates and institutional security.” What it offered was a shiny UX and a false sense of safety.

The Real Danger? Misinformation From Trusted Sources

When a platform like Investopedia makes a mistake like this, it’s not just embarrassing—it’s dangerous.

Many retail investors still don’t fully understand how crypto lending works. They trust names like Investopedia to guide them. So when that source casually recommends a company that literally imploded and got sued by the SEC, that’s more than a typo. That’s negligence.

Why Brands Can’t Afford to Wing It With Crypto Content

This isn’t just a hit piece on Investopedia. It’s a wake-up call to every brand trying to talk about crypto, DeFi or blockchain:

If your content isn’t written or verified by someone who actually knows the space, you’re playing with fire.

You might:

- Recommend outdated or dead protocols

- Misunderstand how DeFi platforms work

- Use jargon that confuses your audience

- Destroy trust with one careless line

That’s why DeFi brands need specialized crypto copywriters. Not just marketers. Not generalists. People who understand smart contracts, risk models, and how regulations are evolving.

Because in crypto, things move fast. And if you’re publishing content based on last year’s facts—you’re already irrelevant. Or worse, you're misleading.

Final Tips For Avoiding a BlockFi-Level Mistake in Your Content:

Vet Your Sources – Just because it ranks on Google doesn’t mean it’s right.

Add a Crypto-Savvy Reviewer – At least one person on your content team should be neck-deep in DeFi.

Avoid Recommending Specific Platforms unless you’ve double-checked their current status.

Use Examples, Not Endorsements – “Here’s how a lending platform could work” > “Use BlockFi.”

Hire writers who live and breathe Web3. Like, say… CopyBiker. 😉

If this made you rethink your crypto content strategy—good. That was the point.

Now go audit your last blog post and make sure you're not sending your readers straight into a regulatory disaster. 😬