The United States, in the same week, is seeking to ban central bank digital currencies (CBDCs) and regulate stablecoins. What a coincidence, isn't it? Politicians rarely make a move without a thimble, but this time the pattern is blatantly obvious.

The vehemence with which the Trump administration has highlighted the benefits of stablecoins has been resounding. Anyone who watched the nationalized Bitcoin 2025 conference in Las Vegas was left with echolalia aftershocks from the repeated use of the word, already a marketing fallacy.

These propaganda efforts find their epitome in the GENIUS Act, passed this Thursday by the House of Representatives and signed today by the president, whose name seems like self-flattery for the genius of this strategy: to win the praise of bitcoiners by banning CBDCs, with the Anti-CBDC Act, while introducing them through the back door of stablecoins.

The Anti-State Surveillance CBDC Bill, which is still under discussion in the House of Representatives, states:

“The Board of Governors of the Federal Reserve System may not test, study, develop, create, or implement a central bank digital currency, or any substantially similar digital asset under any other name or label.”

HR5403 – State CBDC Anti-Surveillance Act

Later, it goes on to define CBDCs as “a form of digital money or monetary value, denominated in the national unit of account, that is a direct liability of the Federal Reserve System.” So far, the only distinction between a CBDC and a US dollar stablecoin is that the asset is a liability issued directly by one of the various Federal Reserve banks.

But the document also clarifies that this ban should not be understood "as prohibiting any dollar-denominated currency that is open, permissionless, and private, and that fully preserves the privacy protections of United States currencies and physical currency," alluding, evidently, to stablecoins.

This is all a game of definitions; the CBDC system already exists in the United States without creating a new instrument. Why do you need a CBDC when 90% of the dollar supply is already entries in a digital database ; when people are arbitrarily excluded from the financial system; and financial surveillance is established under KYC laws ? That is, the Bank Secrecy Act of 1970; the Patriot Act of 2001; the Foreign Account Tax Compliance Act (FATCA) of 2010; the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010; and the Anti-Money Laundering Act of 2020.

In short, an arsenal of laws that forces private financial institutions to become de facto government agencies and report the transactions of their clients and users to the authorities. And guess who's classified as financial institutions under the brilliant GENIUS Act... Bingo!: stablecoin issuers.

This means they must file Cash Transaction Reports (CTRs) and Suspicious Activity Reports (SARs), the same monitoring procedures traditional banks perform. It requires stablecoin issuers to implement Customer Identification Programs (CIPs) and enhanced due diligence (EDD) for high-risk accounts, especially in cross-border transactions. In other words, beyond the transparency and traceability inherent in cryptocurrency network accounting, stablecoin issuers must become direct informants to the State. GENIUS deepens financial surveillance through stablecoins.

And while the GENIUS Act doesn't explicitly mention FATCA, its focus on international interoperability of dollar-backed stablecoins means issuers may have to report information about foreign holders to the IRS, especially if they operate in the 113 jurisdictions subject to FATCA agreements.

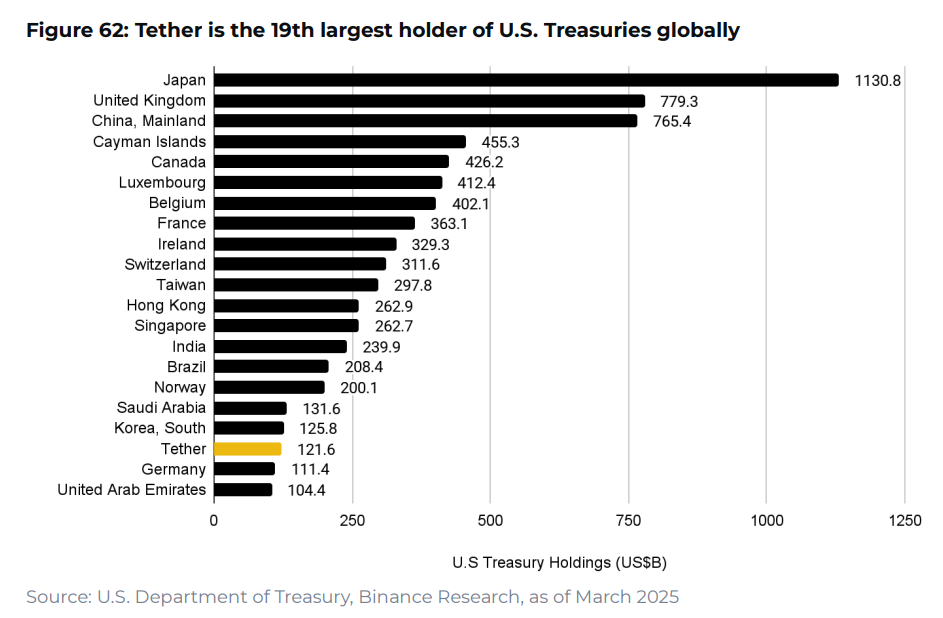

It's said that digital currencies issued by the Fed are prohibited and considered a liability, but by requiring stablecoins to hold their reserves in instruments issued by the Federal Reserve, they not only increase demand for US Treasury assets, but also essentially become a proxy for the institution. Currently, Tether alone is the nineteenth largest holder of US Treasury securities worldwide.

Tether holds more Treasury bills than Germany and the United Arab Emirates. Source: Binance.

Tether holds more Treasury bills than Germany and the United Arab Emirates. Source: Binance.

Furthermore, although it does not explicitly prohibit them, by excluding reserves with other cryptocurrencies, stablecoins such as USDS, formerly Dai, USDe, from Ethena, or GHO, from Aave, and, obviously, algorithmic stablecoins, would in practice be excluded from the game.

This entire scenario undermines the lack of decentralization present in stablecoins and turns them into a machine that leverages the dollar and the Federal Reserve. Stablecoin issuers in the United States will have characteristics similar to any bank. Furthermore, it has already been said that this law favors stablecoin issuers from established banks in the traditional system.

With this law, the United States decentralizes the dissemination of its currency, but now controls it. Before, it was only the Federal Reserve and its branches; now, it's any private US institution that plays by its rules. But with stablecoins, this positioning extends beyond its borders.

Stablecoins have proven that a CBDC would be redundant for the domestic market, given that most payments are already digital. Currently, 98% of the multi-billion-dollar stablecoin market is pegged to the US dollar, and 80% of transactions take place outside the United States. And that's precisely the geopolitical opportunity.

The cryptocurrency market is psychologically and practically dollarized. Not only is the dollar the unit of account against which price fluctuations of all currencies are measured, but traders also turn to dollar-pegged stablecoins for profit-taking and downside protection.

Many people in inflationary economies, with exchange controls, or with limited access to the international market, have turned to dollar stablecoins to save, receive remittances, pay suppliers, and receive other advantages this digital system provides compared to the fiat banking system.

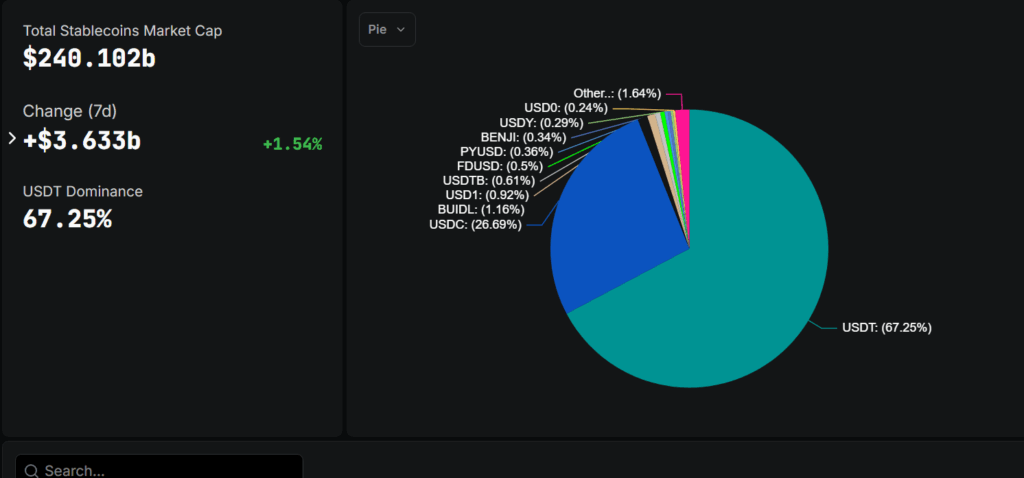

There are currently over 167 stablecoins pegged to the dollar, while there are only 21 for the euro, the second largest fiat currency. However, while there are many stablecoins that could seek licensing under this new regulation, such as Coinbase, Ripple, Binance, the reality at the moment is that the market is controlled by a duopoly between USDT and USDC:

Tether controls 67% of the stablecoin market. Source: DeFiLlama.

Tether controls 67% of the stablecoin market. Source: DeFiLlama.

It is this scenario that the Trump administration has identified and is leveraging to reverse the de-dollarization process that deepened during Joe Biden's presidency, as expressed by Tether's CEO, Paolo Ardoino. While stablecoins bring benefits to life at the individual level, this law will increase the risks of surveillance and account freezing. And, at the state level, they threaten the monetary sovereignty of other countries.

That's why it's more convenient to promote stablecoins rather than CBDCs, as they promote the global hegemony of the dollar without the government being directly accused of interference, since private companies are the ones issuing the instrument instead of the FED.

They will do so candidly, as GENIUS establishes, with the Secretary of the Treasury, former auditor of Tether's reserves, seeking reciprocal agreements with other countries to facilitate the use of dollar-denominated stablecoins issued abroad, probably with negotiations similar to those of the Petrodollar.

At the same time, the dominance of dollar-backed stablecoins around the world, and the importance of the United States as a hub for stablecoin issuing companies, will lead to standards established in the regulatory framework, such as financial oversight measures, eventually being exported and influencing global digital finance practices, ensuring that dollar-backed stablecoins become the global benchmark.

Finally, stablecoins offer the opportunity to remotely freeze funds. It's already common practice for stablecoin issuers to freeze accounts associated with hacks. But since GENIUS, the number of enemies has multiplied, along with the blocking capacity. Until now, the main targets have been individuals classified as criminals (which may include dissidents and political opponents) and sanctioned nations. Now, agencies like the IRS, NSA, and FinCEN will have access to cryptocurrency user data, which their artificial intelligence will analyze, as it has already been revealed they do with banking transactions. This can be leveraged to censor and exclude enemy actors from the financial system, as happened with Russia's exclusion in 2021.

The United States is creating a silent Bretton Woods with stablecoins, seeking to reestablish the international dominance of the dollar, no longer in countries' reserves, but directly in the savings and payments of individuals and businesses. The United States didn't ban CBDCs; it rebranded them.