What happens when the foundations of our financial system are disrupted?

“The Times 03/Jan/2009 Chancellor on brink of second bailout for banks”

That’s the message digitally etched into the first block in a chain that would eventually bring about the age of the Blockchain. Bitcoin.

That was in 2009. Since then, thousands of other Blockchain solutions have popped up, all staking their claim as the “future of x”. In 2018, the total market cap of all cryptocurrencies reached an all-time high of roughly $835 billion. This is a drop in the bucket compared with traditional markets, but for a market never before seen on the face of the earth, reaching that figure in 10 years is not to be sniffed at.

How Did We Get Here?

Since the dawn of humanity, we have needed to transact information and value. In early civilizations, this was easy, since tribes and villages were small. A small number of products and/or services produced by a small number of people. For the most part, transactions were between people who know each other.

As populations grew, so did the complexities of the economy. The number of products and services grew, and people unknown to each other began transacting more often.

To address this, we needed to facilitate new types of exchange: currencies, loans, stocks, etc. These exchanges needed to occur between people, companies, and governments who did not necessarily know or trust each other.

The seeds were planted for the tree that would eventually become our current financial system.

Layers Upon Layers Upon Layers

The system we built is layered. The base layer is where the most fundamental problems need to be solved. How do we design a system which has few limits to exchange but also limits the possibility of fraud? This is the basic principle underpinning our entire financial system. The way this problem is solved influences every layer above it.

The one we have now was created decades ago and rarely ever changes.

Our solution was to create trusted 3rd parties. For example, Governments guarantee the value of our currencies, Banks custody our money, and facilitate exchange. We are trusting these 3rd parties to always act on behalf of us.

Trust

Governments regulate the financial industry to ensure they can trust it. Customers need to trust that banks follow the law and keep their money safe, and banks need to trust each other to develop common protocols and relationships.

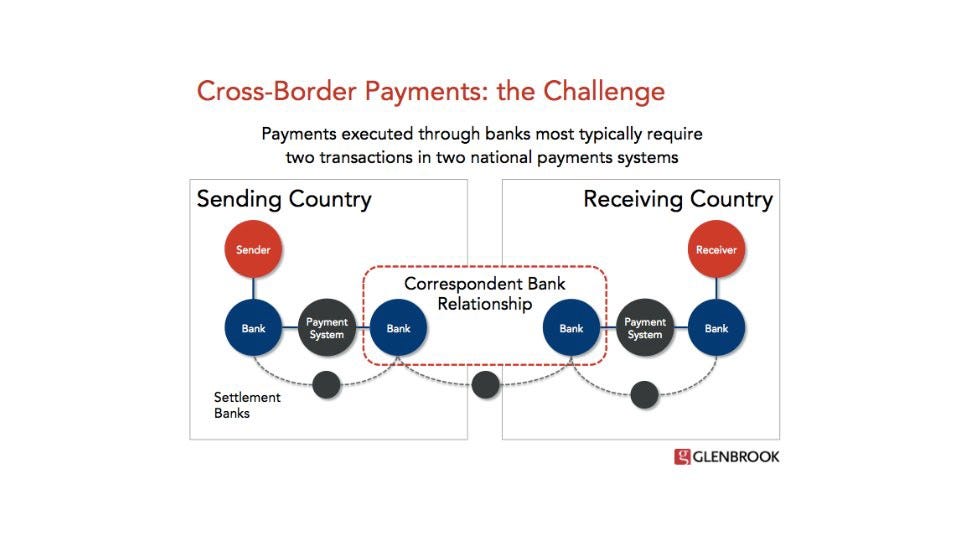

Trust creates restrictions. It introduces extra steps into simple transactions. Consider cross-border payments.

Sending money overseas takes a long time, as you may have experienced. But the reason is the inefficiencies that are introduced by needing trust. The banks need to use a trusted intermediary to get the job done.

So long as the system is built on trust, this is the way it has to be. And it means that the system is slow, lacking freedom and innovation.

The Innovation Problem

Possibly the most tragic consequence of this system is the fact that we can only innovate at the top layer.

For example, Monzo bank has won numerous awards since coming into existence because of its mobile-first approach. They’ve innovated on the top layer so that everything can be done from their mobile app, they don’t even have physical bank branches. Their user base has soared in recent years, but they haven’t innovated at a deep level, they’ve simply maximized the potential of the current system (I’m not bashing Monzo here, I’m a customer myself and find Monzo far easier to work with than traditional big hitters). They invested in technology at the top level before the traditional banks did. They hid the plumbing.

Ask yourself how many other industries have companies as old as the ones in the banking industry. Barclays was founded in 1690. Lloyds, in 1765. Citibank, 1812.

The industry is essentially vaccinated against disruption because of the rigid solutions at the lowest level and the restrictions needed to keep it in place. This begets the “too big to fail” banks that we saw during the housing market crash. If an industry is so immune to disruption, it’s natural to expect cronyism to seep in.

Why Bitcoin Changes The Game

Bitcoin is a huge deal because it seems to solve the problems at the foundation layer in a drastically different way. We can build a financial system from the ground up without trust and third parties.

It is a peer to peer system. That means no third-party guarantees its value, facilitates transactions between parties, or even custody money for other people.

Think about that.

That means we don’t need to trust a government not to print trillions of dollars, reducing value.

We don’t need to trust banks to hold on to it for us, lending our money out without telling us what’s going on.

And we don’t need to pay a trusted middle man x% for transferring money overseas.

Software brings things to life. If it can be thought, software can make it real. Bitcoin is money becoming software. With Bitcoin the foundation layer, the opportunities for innovation in the layers above are boundless.

Just like information and the internet, Bitcoin knows no borders. Sending Bitcoin from the UK to your friend in Australia is the same as sending a URL for a Wikipedia page. Trivial. It has been this way with information for years, and now it’s time for money.

But I Don’t Understand How Bitcoin Works

A common commentary on Bitcoin and Blockchain is that it’s too difficult to understand to become mainstream. The cryptographic protocols involved are simply too complex for the common population to grasp on a large scale, so it will never work.

This is a fundamentally flawed opinion.

The underlying protocol of a disruptive technology doesn’t need to be understood by the masses to be used by the masses. Guess how many of the estimated 4.57 billion internet users can explain HTTP, the base protocol used to serve, and access websites? My generous guess is less than 10% (which would still be 457,000,000 people… bit of a stretch).

Understanding it is not how Bitcoin becomes the default. The moment that an alternative system becomes easier and less painful than the current system, is the moment it becomes mainstream. Monzo best hides the plumbing of the current financial system. As soon as the same thing happens for Bitcoin, that’s when it becomes mainstream.

Where We Go From Here

Bitcoin is the foundation for a brand new financial system. Products and services that build themselves on this foundation will look alien compared to the traditional financial system. For users, this means better service, more flexibility, and the removal of the need to trust any third-party entities with our money.

Any businesses built on this system will be far better suited to meet our monetary and digital needs. Our expectations will change, we’ll look back on the archaic system we have now in bewilderment at how expensive and cumbersome it is. Our economies will become even more complex and multifaceted, fulfilling the needs of everyone.

Bitcoin is not just internet money, or nerd currency, or a hobby. It will, and is already, the foundation for a completely new financial system.

And it will change the world as we know it.

Further Reading

If you’re interested in Blockchain Development, I write tutorials, walkthroughs, hints, and tips on how to get started and build a portfolio.Check out this evolving list of Blockchain Development Resources.

If you enjoyed this post and want to learn more about Blockchain Development or the Blockchain Space in general, I highly recommend signing up to the Blockgeeks platform. They have courses on a wide range of topics in the industry, from Coding to Marketing to Trading. It has proven to be an invaluable tool for my development in the Blockchain space.