Bancor v2.1 has been live for about three months. The new version of the protocol offers single-sided exposure and impermanent loss protection to AMM liquidity providers through the use of BNT.

The following report uses on-chain data collected October 24, 2020-January 6, 2021 to analyze the growth and overall health of the protocol. Additional protocol reports, live dashboards and network data will be made available to the community via bancor.network.

Highlights:

- Total network liquidity increased almost 1000%, driving $1.12M USD in cumulative swap fees ($4.48M annualized).

- The value of swap fees earned by the protocol exceeded the total cost of impermanent loss compensation paid to liquidity providers by a margin of more than 5X.

- This indicates protocol revenue is covering the cost of impermanent loss protection, and generating a profit for the protocol and its owners (BNT holders).

- The results lend credence to the sustainability of the v2.1 model and largely support our belief that v2.1 offers a compelling answer to the problems of first-generation AMMs.

Sections:

- Bancor v2.1 Primer

- Liquidity & Fees

- Impermanent Loss Protection

- BNT Supply

- Outlook

- Conclusion

1. Bancor v2.1 Primer

A key feature of Bancor v2.1 is impermanent loss insurance, which provides compensation to liquidity providers for impermanent loss incurred on their staked liquidity.

Impermanent loss in AMM liquidity pools gets its namesake from its variable magnitude over time. The loss at any point in time is hypothetical, and determined by the relative price movements of the tokens inside the pool.

During periods where the relative TKN/BNT prices are diverging (“TKN” is used henceforth to indicate any token other than BNT), the implied impermanent loss is rising, but falls again if prices revert back to their original ratio when the liquidity was first contributed.

As a result, the overall insurance liability to the protocol varies with time, and experiences frequent moves in both directions. What is owed to liquidity providers at any given time will likely differ from the compensation eventually paid out by the protocol.

Therefore, impermanent loss compensation is not a cost paid in real-time, but rather a cost that is only realized by the protocol when protected stakes which incurred IL are withdrawn.

By design, the insurance policies offered by Bancor are earned over time. When a user makes a new deposit, the cover offered by their insurance policy increases at a rate of 1% each day the stake remains live, and matures to full coverage after 100 days.

After this period, any impermanent loss that occurred in the first 100 days or any time thereafter is covered by the protocol at the time of withdrawal. Withdrawals prior to the 100-day maturity are only eligible for partial compensation.

For example, withdrawals after 60 days in the pool receive 60% compensation on any impermanent loss incurred. Also, there is no compensation offered at all for stakes withdrawn within the first 30 days.

2. Liquidity & Fees

Protected Liquidity Deposits

Since Bancor v2.1 launched, total liquidity on the network increased almost 1000%, currently at around $175M USD.

Protected Liquidity Withdrawals

The amount of protected liquidity withdrawn during this time was 13.7M BNT ($21M USD).

Fees

Total fees earned by the protocol and its liquidity providers equaled roughly 700,000 BNT or $1.12M USD ($4.48M annualized).

Currently about half the BNT in the pools has been contributed by the protocol, therefore the protocol is expected to earn 25% of the overall fees earned.

During the study period, protocol-earned fees amounted to 175K BNT or $300K USD — all of which has been or will eventually be burned for BNT, placing deflationary pressure on the token.

Revenue growth per pool coincided with increases to co-investment limits. Co-investment limits, which are governed by the BancorDAO, determine the number of BNT that can be emitted by the protocol into a given pool to support single-sided TKN deposits.

The process is as follows:

- New BNT is co-invested by the protocol into a pool to match user deposits of single-sided TKN (e.g., a $100K deposit of LINK triggers $100K of BNT minted into the LINK pool)

- Protocol-invested BNT is minted into the pools and not onto the external market.

- The BNT remains in the pools and earns fees until the BNT and its accrued fees are eventually burned.

- The burning of protocol-invested BNT and its associated fees happens when the TKN provider withdraws their deposit, or when a BNT holder stakes their BNT in the pool, taking over the protocol’s position.

Emission of new BNT to enable single-sided TKN deposits supported a significant rise in liquidity and fees earned by the protocol. In addition, more users deposited their BNT into pools to take advantage of the rising fee income and earn yield on their BNT.

Currently, about 56% of the total BNT supply is staked within the protocol.

It should be noted that BNT emitted by the protocol doesn’t enter the open market unless prices significantly change.

Instead, this BNT is sent directly into the protocol’s pools, and generally stays within the protocol earning fees until it is burned. Further analysis of these mechanics and the impact on BNT supply can be found in section 4, “BNT Supply”.

3. Impermanent Loss Protection

A key data point is the amount paid to liquidity providers as compensation for impermanent loss. Figure 6 represents the current cost of running Bancor’s insurance offering, measured against revenue from swap fees.

Total impermanent loss associated with withdrawn protected liquidity is roughly 41K BNT or $64,000 USD. Meanwhile, fees earned by the protocol and BNT liquidity providers during the same period are equal to 350K BNT or $560,000 USD ($2.24M annually).

This indicates that at this stage, protocol revenue is dominating the realized costs of impermanent loss protection, and generating profits for the protocol and BNT holders.

The 41K BNT worth of impermanent loss was not an expense paid in net new BNT, since swap fees earned from protocol-invested BNT were used to cover the cost.

In addition, some liquidity providers withdrew their deposits prior to achieving 100% insurance. Liquidity providers who withdrew their deposits accrued partial protection from impermanent loss, and were paid out according to their level of cover.

As the proportion of insurance policies with 100% protection increases over time, it stands to reason that the associated cost to the protocol will rise. However, various factors suggest the protocol is able to handle this insurance burden.

Differences in deposit dates between liquidity providers is an important consideration. The time-staggering creates a situation where the insurance liability is spread unevenly across the pool.

This has been partially influenced by co-investment limit updates governed by the BancorDAO, allowing for more single-sided, protected liquidity to enter the system in waves, as opposed to all-at-once.

This healthy distribution of relative liability in the protected stakes on most pools reduces the frequency and magnitude of insurance-related BNT pay-outs. This will be an important metric to continue monitoring and discuss further in future protocol health reports.

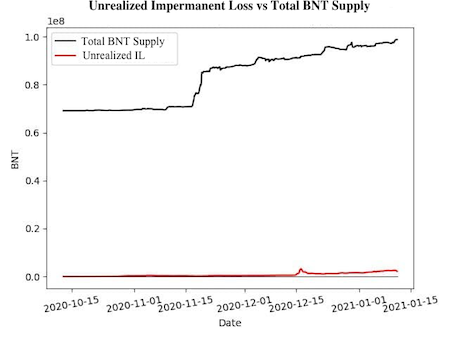

The unrealized costs of impermanent loss should not escape scrutiny. To estimate the total impermanent loss of the system requires a hypothetical ‘black swan’ scenario in which all liquidity providers withdraw from the protocol in the same instant, leaving the exchange completely empty.

For this exercise, it is assumed that all liquidity providers have attained 100% impermanent loss coverage, resulting in a conservative over-estimate.

In figure 7, this unrealized inflation is compared with the total BNT supply over time. It is plainly apparent that even under the catastrophic conditions of this hypothetical, the total dilutive influence of impermanent loss insurance across the protocol is minor.

Overall, the data above suggests that protocol fees are covering the realized insurance costs (i.e., the cost of doing business), while unrealized insurance costs would incur minimal dilution to BNT holders.

These results lend credence to the sustainability of the v2.1 model, as outlined in our technical documents, and largely support our belief that v2.1 offers a compelling answer to the problems of first-generation AMMs.

4. BNT Supply

Impermanent loss protection so far has resulted in minimal BNT emissions. Low emissions are supported by the protocol’s ability to co-invest BNT and use fees from co-invested BNT to compensate LPs for impermanent loss.

Therefore, it is clear all new BNT tokens added to supply since the v2.1 launch are currently being used to support single-sided liquidity entering the system. The increased token supply can be viewed as a type of bootstrapping overhead, that is slowly paid back to the protocol via a token burning process.

The elastic use of BNT to support single-sided deposits is distinct from other emissions-based rewards programs which send tokens to users to be claimed immediately, or after some lock-up period.

Rather than being distributed to users, the protocol supplies BNT to its pools as needed, and under the guidance of the DAO, to support new single-sided deposits.

The protocol therefore has a significant yield-earning share of the pools, and its earnings are used to fund the BNT token burning mechanism.

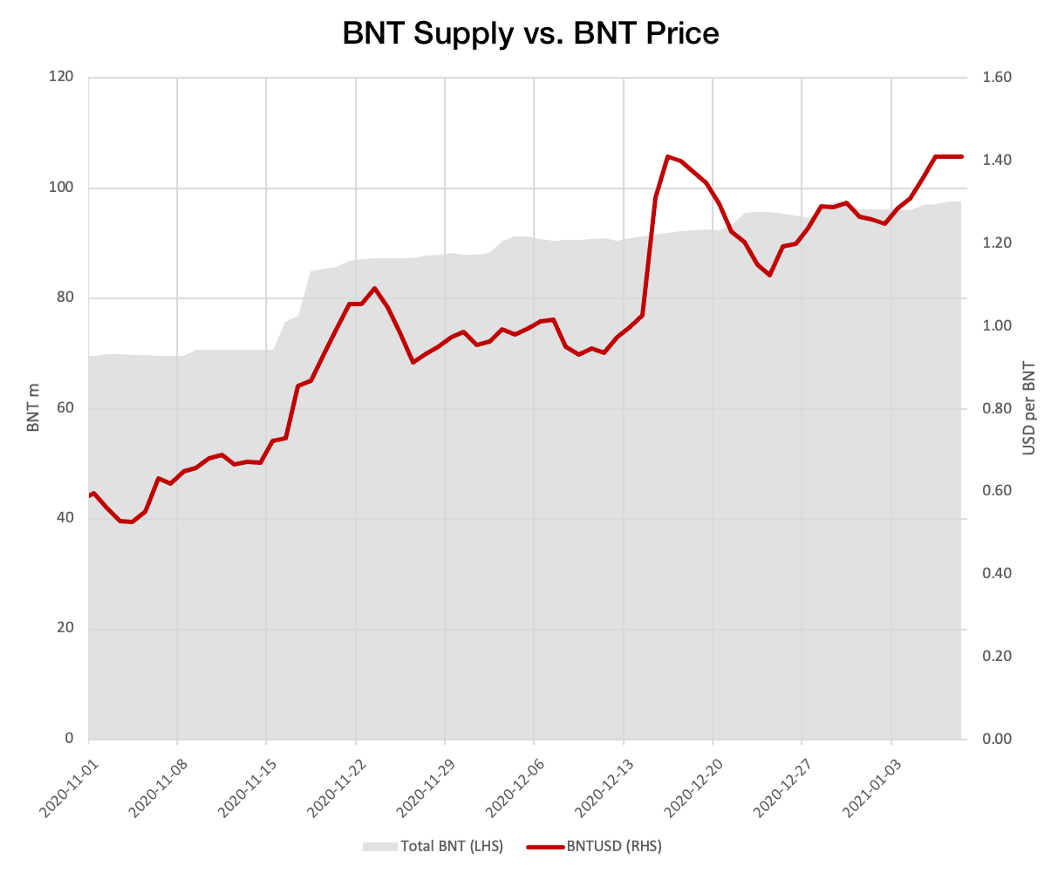

Since v2.1 went live, the BNT supply has increased by almost 45%, climbing from roughly 69M to roughly 98M. All minted BNT was minted into the pools and not onto the external market.

Depending on market moves, the pools may leak this BNT onto the external markets, or they may absorb BNT from the external markets. As long as markets stay within the same range, protocol-emitted BNT remains in the pools.

The supply increase coincided with a 210% increase in the BNT price against USD. In our case, creating new BNT and providing it to pools resulted in a disproportionate increase in demand for the token, and the demand has largely been supported by its increased supply.

As can be seen above, the value of BNT appreciated as supply expanded. This is not a novel phenomenon, and can be interpreted by considering the origin of BNT value.

The vast majority of new supply is used exclusively to support single-sided deposits in the protocol until it is eventually burned. This creates new market opportunities and increases the total locked value of the system. Overall, the case for staking BNT is only made more attractive.

The lack of selling pressure is also worth noting. Since minted BNT inherits the current market price at the time it is created, and is only available for purchase via the pools, there is no associated ‘dump’ that usually follows the minting of tokens, as is observed in other projects.

The above points notwithstanding, it is important to remember that there is a persistent deflationary pressure on BNT that is dependent on the protocol’s co-investment and earnings.

When swap revenue is high, BNT holders can have their cake and eat it too — the inflation associated with minting new tokens supports the ecosystem, and then pays for itself through token burning.

This is akin to the protocol investing money on marketing to drive usage, then allowing the investment to pay itself off over time.

Increases to co-investment are correlated not only with increased liquidity and fees, but also rising annual percentage yield (APY) for liquidity providers.

This suggests that in certain areas of the network, fees are growing faster than liquidity as specific pools become more competitive in the market and capture a growing share of total volume for a given token, via DEX aggregators or direct traffic.

5. Outlook

New proposals currently in the late-stages of development by the BancorDAO are worthy of attention. An admin fee, which charges TKN liquidity providers for impermanent loss protection, via a small fee on swap revenue, could significantly support the capacity of the protocol to cover its liability, and maintain a stable insurance model.

Known as the Bancor Vortex, the current proposal is open for discussion on Bancor’s Discourse forum and focuses on a new utility for vBNT that creates additional revenue streams for BNT holders while supporting market demand for BNT staking in the protocol’s pools.

Additionally, a new merit-based whitelisting schedule offers the means to establish insurance status on new tokens without sacrificing caution or diligence.

To token communities, this represents an opportunity to establish a market on Bancor where holders can benefit from its unique features; to the BNT community, it represents a tenable means to grow the total value of the system in a responsible, business-first approach.

6. Conclusion

By most indications, the network is healthy, and functioning as intended. The total locked value in TKN and BNT has exploded, and swap fee revenue with it.

The ability of the protocol to support single-sided deposits with no IL is actively supporting market demand for BNT, through the creation of a compelling, high-yielding platform for swappers and LPs.

Our mission to provide a sustainable AMM model that allows its liquidity providers to stay long on their tokens, free from the threat of impermanent loss, is coming to light.

This preliminary health status update indicates that the system is profitable, and scalable, for both TKN providers and protocol owners (BNT holders) who act as underwriters of impermanent loss risk.

Additional protocol reports, live dashboards and network data will be made available to the community via bancor.network.

Co-Authors: Nate Hindman, Mark Richardson, Stefan K. Loesch (topaze.blue), Michal Herzyk