Previously on this platform we made the case that the Fed was essentially boxed in. The Fed could pursue/allow hard defaults which result in a literal deflationary collapse of the system and society, or it could opt to inflate its way out of debt. Either way, the choices are not much more fun than getting your teeth yanked out.

Fed Wants And Needs Inflation - Stealth YCC and Debt/GDP Magic Tricks

Yield Curve Control In Japan - Coming Soon To America

Bank for International Settlements Allows Banks To Keep 1% of Reserves In Bitcoin

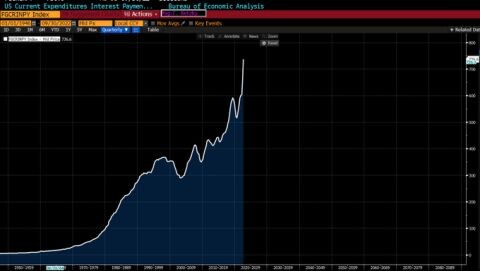

In effect, our stance has been that the Fed will push to a certain point, but the bills still need to be paid and the Treasury will still need to sell more debt to someone. The chart above depicts the run rate for annualized interest payments on outstanding UST. This is going parabolic at this point with an inverted yield curve with rates north of 4.00% across the curve. This may be the most important chart in the markets to observe currently.

Annualized, the projected interest payments on the debt now exceed the projected budget of the Department of Defense. And here are some more nuggets related to this issue:

- In a tough environment for risk assets, cap gains tax receipts moving forward will be much, much lower

- Social Security and Medicare are untouchable

In short, tax receipts are about to plummet, and the Treasury's largest buyers of UST historically are either gone or tapering off their activity. Japan, for example, has huge issues of its own to manage. Who will buy the new UST issued?

It's much easier for Chair Powell to "pull a Volcker" if Debt/GDP was around 40% like it was when Volcker embarked on his mission to hammer down inflation. Debt/GDP is far north of 100% now which severely limits the options for the Fed (if it chooses to avoid full on collapse).

Here's a possible route they take:

- Raise the "target rate" for inflation and gaslight the public with bullshit like "the new normal" and other pontification about how their models said this or that, blah, blah, blah

- Implement YCC and QE

- Obsess over YOY comparisons in 2023 that show "inflation coming down" (entirely plausible with weakening economy)

- Stoke the flames of a move to "risk on" while attempting to nudge the economy forward which results in NOMINAL Debt/GDP lowering so the Fed can gaslight the public about how it "reduced the debt burden" which is another way of saying the problem is still there but they made it look less troublesome relative to GDP (a GDP inflated higher with a higher "inflation target rate")