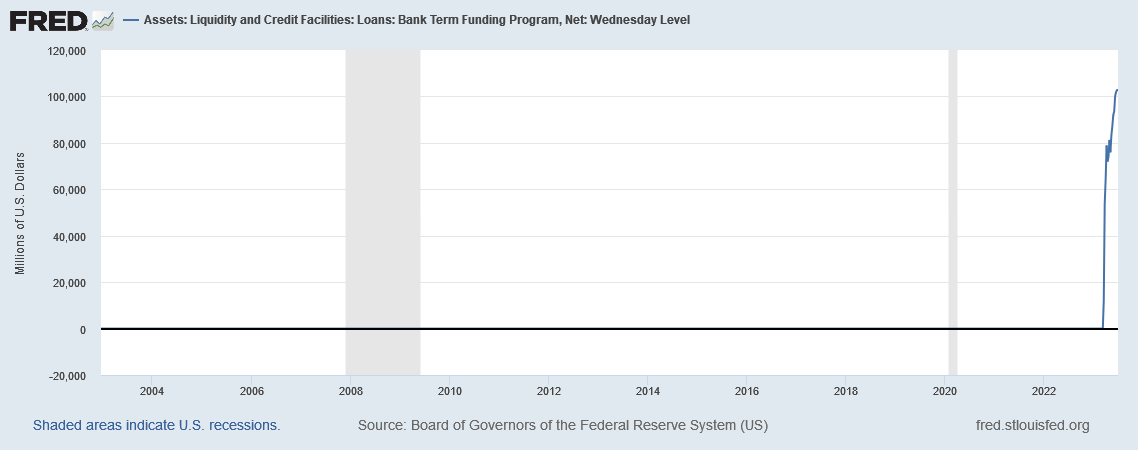

So what do we have here? Let's take a look at the Fed's new bailout program (Bank Term Funding Program - BTFP) and the Federal Home Loan Bank (FHLB).

IMF Preps Central Banks for Raising Inflation Target Above 2%

Also, here are some other recent articles related to the subject matter of this post:

What Would Constitute Checkmate?

Did The Bitcoin Price/Volume Trend Change Yet?

Credit Default Swaps And Bitcoin

YCC and QE - Fed WANTS Inflation

Bitcoin Hitting All Time Highs

Consider this list and in this specific order.

1. BTFP

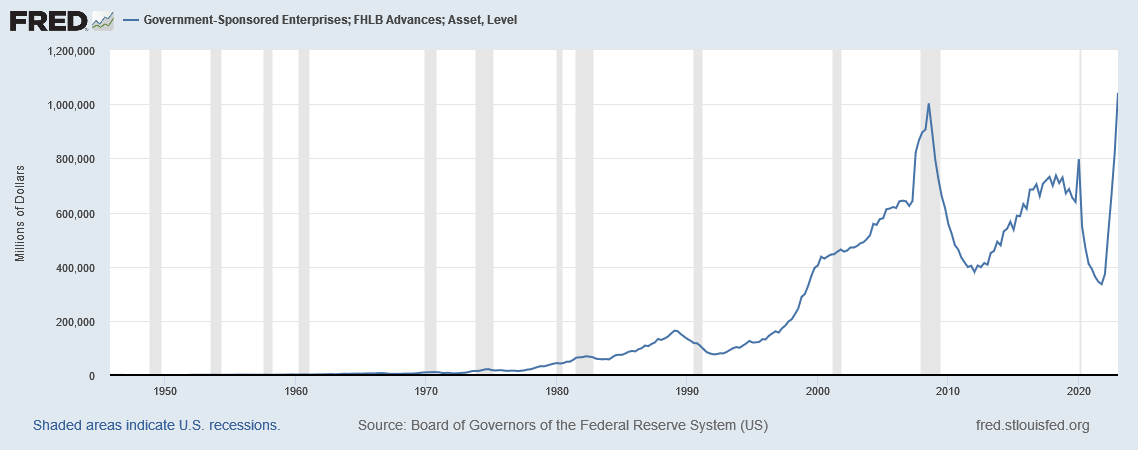

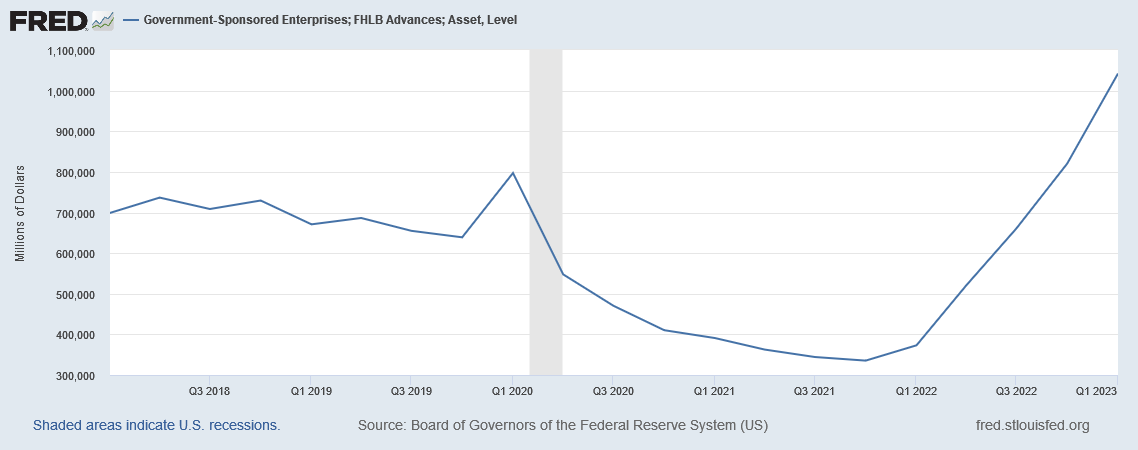

2. FHLB

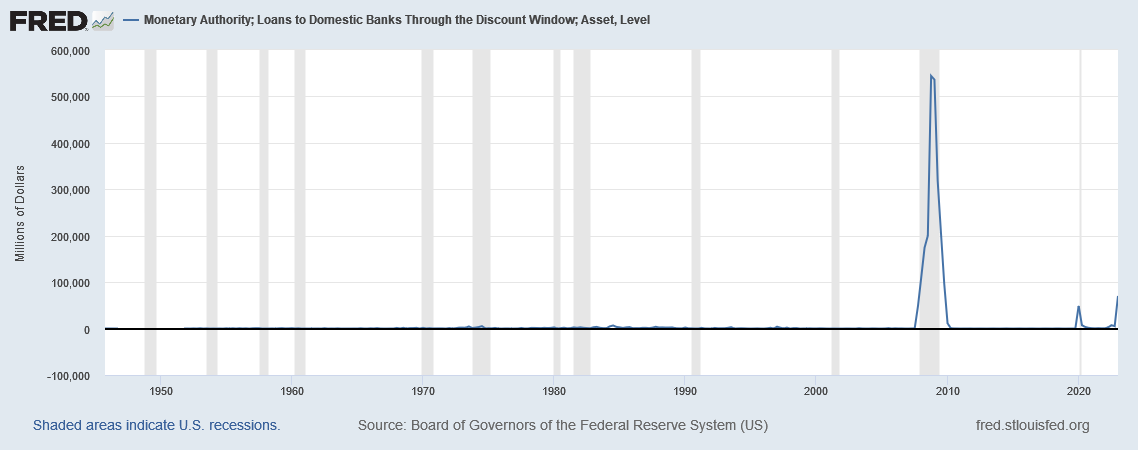

3. Discount Window

In order the least to most "tail between legs" use of a facility by a bank. Below is an image of the Fed's Bank Term Funding Program:

Sure, one can contend that "hey it spikes up because it was just created". True. But, has it come down or is it still at the same levels of usage or a bit higher from launch?

Here is a graph from the Fed depicting the assets (loans to other banks) of the Federal Home Loan Bank. If everything was safe and sound, as proclaimed by the Fed and Treasury Secretary, then why are these loans outstanding spiking above the levels seen in the GFC years ago?

Let's look at this through the lens of both Game Theory and human nature. The Fed opened up a new credit card for banks (BTFP). Think of it like a household rather than a bank. The first thing a household under stress does is grab what is available "for free" as provided by the central authority.

Then, a household under duress financially (like a bank), would pursue the next option if needed that is the least painful or embarrassing or indicative of the true financial level of health of the household. Enter the FHLB. The FHLB is pitched as a place where banks can tap liquidity needed to smoothly provide mortgages to the marketplace and support the economy, housing, construction, blah, blah, blah. The truth is banks can tap this without any formal explanation of why they are tapping it. It's available, and as seen above, is being used very aggressively.

Our contention is that we are nearing the end of the "kick the can" and "extend and pretend" phase. The use of the FHLB is very telling in our view - very telling. Why has it skyrocketed since early 2022? Were banks starting to tap this well before the failures of SVB and other banks earlier in 2023?

What's next?

Well, if a bank has tapped out on the BTFP and the FHLB, then next in line is the Discount Window (a true knockout blow to equity holders in all likelihood). Why would you want equity in a bank that is begging the Fed and market for mercy at the Discount Window?

Equity markets and the economic data have been telling you all is well and AI will save the world and create a supercharged economic growth engine. Debt markets have not been aligned with this. What has been fixed to make one feel like the "banking crisis" earlier in the year has been resolved?

We shall see.