No surprise to anyone here that things are quite a bit rocky. Well, here's a few charts not intended to brighten the mood at all.

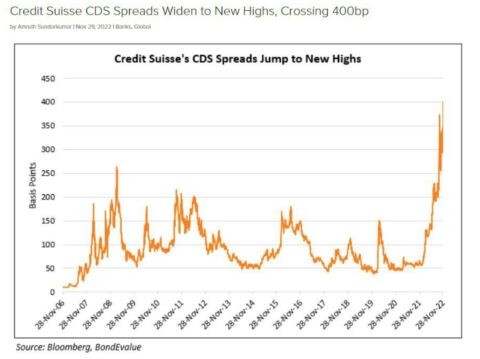

CDS Spreads for Credit Suisse bank just vaulted again in a parabolic fashion to new highs above 400 bps. This is well above the levels seen during the 2007-2010 financial crisis period. This spread represents the rising cost to insure against Credit Suisse defaulting on its bonds. Translation: the market thinks this aging behemoth is going under. Oh yeah - the Fed sent the Swiss National Bank $6.3 Billion via overnight swaps in mid-October.

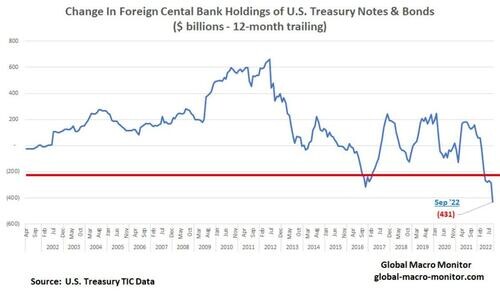

The chart below depicts the change in Foreign Central Bank holdings of UST. In other words, this shows the demand for American debt from foreign countries. Clearly something shifted in the 2011-2012 period, and note the drastic decline since Biden took office. Real estate, equities, crypto and other assets have all been hammered hard in 2022 in America from Chicago to Boston to LA and all over the land, to the point you can't gloss over it like putting on some fake teeth. That means cap gains tax receipts in 2023 are in the tank.

So, in short, the typical buyers of U.S. notes and bonds (UST) are fleeing but the amount of debt that needs to be sold is set to rise very dramatically, particularly in the post-Covid money orgy period. Who will buy the bonds? Here's a few other pieces we published here covering this topic:

Is The Fed Prepping Bitcoin To Serve As Life Preserver?

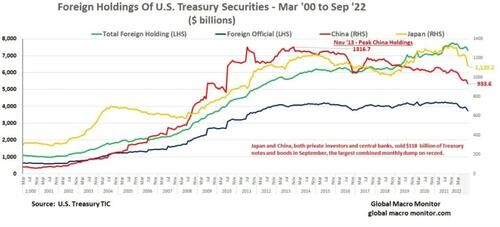

The last chart presented here breaks down the foreign holdings of UST by specifically looking at China and Japan - typically and historically the two largest buyers of UST. Now, call us crazy, but after Biden stole/froze Russia's UST, we find it a tad bit difficult to believe that Russia will be coming back to the feeding trough anytime soon.

As one can see below, China's holdings continue to decline as they have since 2011-2012 and are even accelerating that trend. Japan's holdings are falling off a cliff. As one might recall, we laid out how Japan is tackling YCC which leaves them in a horrific position. The Bank of Japan can print Yen to defend the yield on the ten year JGB, but this crushes the currency. Or, it can defend the Yen and be unable to conduct YCC. Can't have it both ways. Tick tock tick tock.

Conclusion:

- banking crisis in Europe entirely plausible which will spread beyond Europe

- Treasury Department will eventually face a very legitimate crisis where there are not nearly enough external buyers of UST to mop up the ever expanding needs of the DC Swamp to spend more and need to sell more debt

- U.S. Government faces a scenario where the only way to keep spending and remain functional is for the Fed to step in and buy bigger and bigger chunks of newly issued UST

Federal Reserve: Foreign Holdings