Probably you've already used one without knowing it. Let's take a look at what they actually are, how they work, and why the world's leading payment companies are getting on board and looking to build on top of them.

Visa handles approximately $15 trillion worth of transactions per year. In 2025, $46 trillion were processed through stablecoins. PayPal's volume is exceeded by more than 20 times. Three times Visa's. That number is a real number, and most people wouldn't know it.

Stablecoins are no longer the stuff of cryptocurrency lore. They're financial infrastructure, and that change from experimentation to the mainstream occurred quicker than many expected. Stripe, Mastercard, Visa, PayPal, BlackRock – this is where they are now. The time to catch up with this is quickly running out.

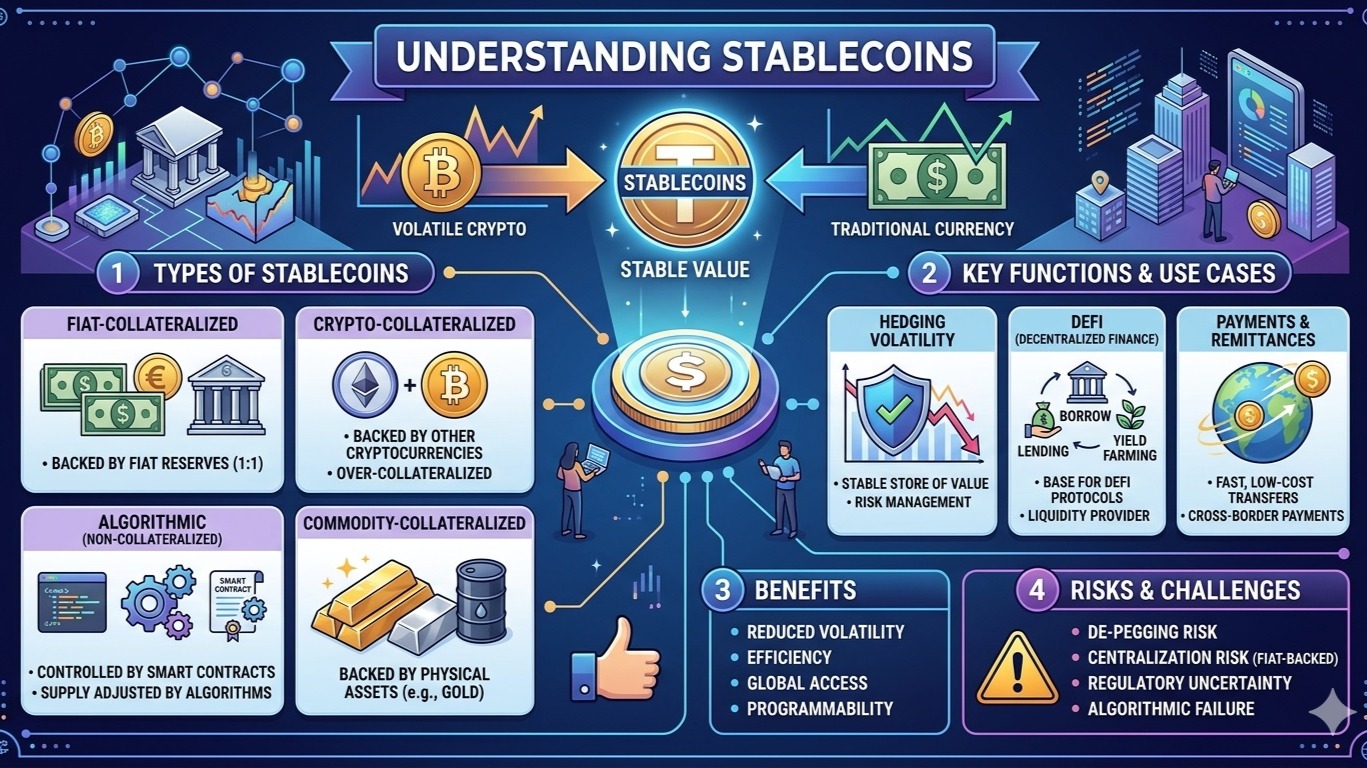

A stablecoin is just what it sounds like.

A stablecoin is a cryptocurrency that has been “backed” by a stable asset, typically the USD. It takes 1 token to equal 1 dollar. It can be sent worldwide in seconds, 24 hours a day, seven days a week for fractions of a cent. No bank required, No correspondent banking delays, No 3-5 business day settlement windows.

What type of stablecoin you're dealing with is determined by the mechanism that is used to keep the peg in place. Most, about 84% of the $319 billion market, are fiat-backed, meaning that an issuer has real dollars in a bank or Treasury bills, and issues tokens against those dollars. The USDT and USDC operate in exactly the same fashion. The second type involves crypto collateral that is locked into smart contracts, and overcollateralized to offset price fluctuations. This is primarily due to DAI. The third type — algorithmic stablecoins — attempted to keep the peg by coding and making adjustments to their supply of the coin instead of real reserves. One of the biggest was Terra UST. It has been down since May 2022 and has lost $40 billion of value in 72 hours. Algorithmic stablecoins, which lack real support, have not bounced back as a category.

In 2026, the share of the fiat-backed model is completely dominated in the market. That was the only model that was touched after Terra.

USDT vs USDC — they are no longer one and the same.

Until recently, USDT and USDC for all intents and purposes were the same. Both dollar-indexed and both liquid and widely accepted. In 2026, that's changed. They are in different markets and have different, meaningful, risk profiles.

As of April 2026, USDT (issued by Tether) has a circulating supply of $189.6 billion. That represents 61% of the total stablecoin market. It's the normal liquidity spine of the cryptocurrency trading market globally. More than 60% of USDT's total supply is on the TRON chain, where transfers cost mere fractions of a cent and where hundreds of millions of people in Africa, South East Asia, and Latin America have a convenient dollar saving account. The wallet is integrated into natively in the Telegram wallet, which currently has more than 150 million registered users. In some countries with developing economies, USDT is the most easily available source of dollars available.

The issue is that the Tether is not compliant with the GENIUS Act. It doesn't meet the new US federal requirements for stablecoin issuers. It's further limited under European MiCA regulations. Tether hasn't received the authorization from MiCa to be able to access exchanges and institutions in Europe. In the case of trading in offshore markets and emerging markets, none of that is deemed significant. It is a very important consideration for all of those that affect financial infrastructure in regulated markets in the United States and Europe.

USDC, which is created by Circle, has $77.6 billion in circulation, up 72% year over year. Compliance driven option, fully attested by Deloitte, licensed across 20+ chains, GENIUS Act compliant in USA, MiCA compliant in Europe. USDC is used or integrated by Visa, Mastercard, BlackRock, PayPal, Stripe and Coinbase as a settlement and treasury currency. Circle's revenues rose to $770 million for Q4 2025, while EBITDA jumped by 412%. Circle is also developing Arc, a Layer 1 blockchain on which the gas token is USDC, which has already completed more than 150 million transactions in its first 90 days on testnet.

To appease the regulatory scrutiny, Tether started issuing a new stablecoin, USA₮, in January 2026, but through a nationally chartered US bank, with Tether serving as a technology partner. It's still in its early stages, but it's apparent that, even for the US regulated market, it is a different product.

In March 2023, USDC briefly dipped to $0.88 when Silicon Valley Bank collapsed and Circle reported it had $3.3 billion of its reserves impounded at Silicon Valley Bank. It bounced back in days following Fed's deposit insurance of SVB. It's a helpful reminder that fully backed doesn't imply no risk — it's the issuer's bank that remains fully backed, not the crypto market. Choose your issuer accordingly.

The GENIUS Act – what really happened

On July 18, 2025, the Guiding and Establishing National Innovation for US Stablecoins Act was signed into law. It's the first ever comprehensive federal regulation of stablecoins in the history of the United States and it continues to be implemented, with full compliance rules due no later than July 18, 2026.

It demands that the stablecoin issuers maintain 100% reserves of U.S. dollars or short-term Treasuries, be audited monthly by registered accounting firms, follow anti-money laundering regulations, and be regulated either federally or at the state level. It also found that if the issuer becomes insolvent, the stablecoin holders' claims are prioritized over the reserves, which implies that if the issuer goes broke, you'll be paid first, and not last.

The result: it separated stablecoins into two groups — compliant and non-compliant. Those institutions that will be required to engage with US regulators, banks or payment networks now have a clear answer concerning which tokens they can use. That transparency, above all else is what is driving the corporate and institutional adoption that is in progress.

The value of the stablecoin market increased by 49% between January 2025 and early 2026, expanding from $205 billion to $319 billion. A big booster was the GENIUS Act. Not because it rendered stablecoins safer overnight, but because it created a stablecoins regulatory environment that was predictable enough for large institutions to commit to.

Why major payment companies like Stripe, Visa and Mastercard are now in the game.

This is the aspect of the stablecoin saga that most people don't pay enough attention to. Over the past 18 months, the world's largest payments infrastructure firms have been making the settlement of stablecoins into their product a seamless process.

In late 2024, Stripe purchased Bridge, a stablecoin infrastructure company for $1.1 billion. This is the biggest acquisition of Stripe's history. Earlier this year, Mastercard took a stake in a stablecoin payments firm, BVNK. Visa increased the number of blockchains in its stablecoin settlement pilot to nine in April 2026, alongside the addition of Base, Polygon, Canton Network, Arc, and Tempo to the support for Ethereum, Solana, Avalanche, and Stellar. In the 90 days ending in October, Visa's on-chain stablecoin settlement reached annualized run rate of $3.5 billion by the end of last year. PayPal's PYUSD is now in circulation, with $3.4 billion worth of it available for use, directly within the PayPal and Venmo app.

Stripe, Visa and Mastercard are now reportedly nearing the launch of a stablecoin offering together, and Coinbase is reportedly considering joining. The specifics are not yet available, but the message is loud and clear: The card networks aren't sitting on the sidelines while stablecoins are in development. They are constructing the railway.

The actual infrastructure implementation: This would not be visible to most users. You will pay with a card or PayPal anyway. A larger percentage of those flows will be deposited in USDC or PYUSD, instead of passing through traditional correspondent banking systems, underneath. User experience remains unchanged. The back-end becomes much more cost-effective and efficient.

The dangers that do not dissipate

There's a $319 billion market that's based on a level of trust in issuers and banks and code, and that deserves the disclosure of risk. Some clarifications.

Concentration risk: USDT and USDC make up the vast majority of the market. The repercussions of either having a major issue — a bank failure, regulatory action, reserve deficiency — would be huge. What went down with the USDC is a preview of what will occur with the SVB episode in the near future. It resolved quickly. Not necessarily all of the time.

Not FDIC insured: Stablecoin assets are not covered by any deposit insurance scheme. Reserves can be deposited in insured bank accounts, but the token has issuers' risk. That distinction matters.

Failure of algorithms is still fresh in everyone's memory: Terra UST collapsed less than 4 years ago. The lesson – be warned that a stablecoin with no underlying assets can collapse – is not to be forgotten. However, new algorithmic or semi-algorithmic projects keep emerging. The marketing is not the most important factor, it's the mechanism.

Outside the US: The GENIUS Act brought clarity to the US. It was developed in Europe by MiCA. The regulatory landscape is also not uniform and stable in those areas. Markets can become stablecoin-restricted in a matter of moments.

In practice, this translates to the following:

Even in the case of trading or the short-term parking of capital, the liquidity of USDT on major exchanges is still unbeatable. USDC's compliance profile can eliminate the friction that USDT cannot, a friction that is particularly noticeable when keeping for any purpose that involves regulated financial infrastructure, such as DeFi protocols, institutional products, corporate treasury, etc.

Avoid keeping a significant amount of stablecoins on exchanges. This is the same rule as for all cryptos – not your keys, not your coins. A claim on Circle's reserves that is recorded in your wallet is a USDC. A USDC on an exchange is a statement of an exchange's commitment to provide you that USDC on request. These are two separate things.

The larger scale: stablecoins have already subtly emerged as the most popular financial product in crypto by volume of transactions (TVT). Most financial news did not include the $46 trillion in flows that will occur in 2025. The Visa partnership failed to go trendy on Twitter. But the build out of said infrastructure is occurring at a scale and rate that certainly doesn't imply a trend, but rather a transition.

It's not USDC vs USDT that's the most interesting thing going on with stablecoins today. It's yield-bearing stablecoins: such as BlackRock's BUIDL ($2.8B), Circle's USYC ($2.9B), and Ondo's USDY ($2.1B) which keep TBills on-chain and share the yield with its holders. These are in a grey zone between GENIUS, so they are securities, not payment stablecoins, but they vie for the same balance sheets. As the months pass, the distinction between a stablecoin and a tokenized money market fund is becoming increasingly blurred.