You need dollars today. Do you sell some BTC (likely pay tax and lose future upside) or borrow against it (keep upside and pay interest costs)? This guide gives you a practical way to choose, plus a calculator to run your numbers in minutes.

1. Decision at a Glance

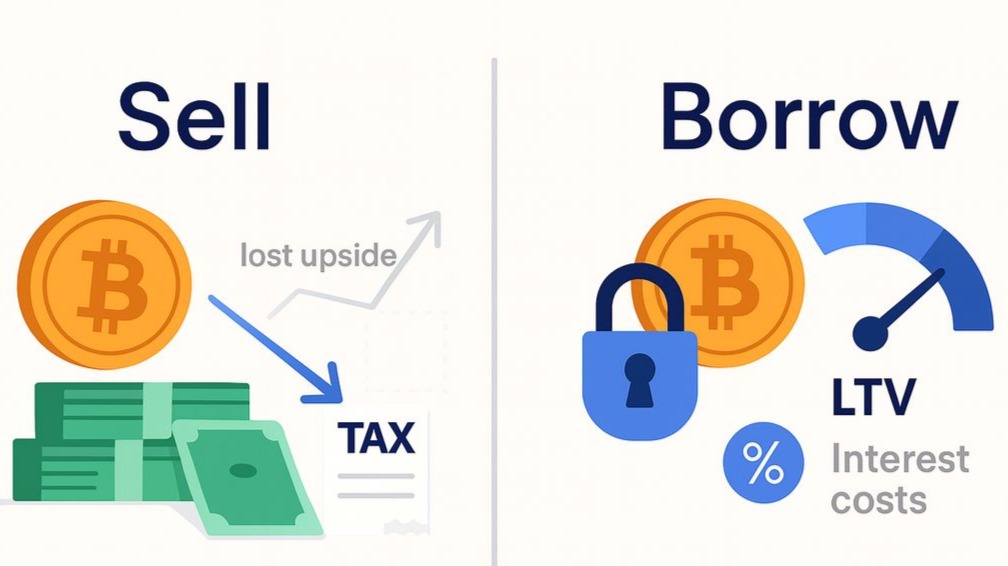

Two paths to raising cash from your Bitcoin:

- Sell BTC: instant liquidity, likely a taxable capital gain, and you give up future upside on the coins you sell.

- Borrow against BTC: pledge BTC as collateral, receive a cash loan, pay interest, and watch your loan‑to‑value (LTV). If price falls past a threshold, you may need to add collateral or risk liquidation.

Use Wallet Pilot's Sell vs Borrow calculator to see both outcomes side by side with your numbers: interest costs, taxes, and liquidation buffers.

2. Real Life Example

Meet Carla, a long-term HODLer who needs $50,000 for a home renovation. She owns 2 BTC, purchased in 2019. Bitcoin trades at $100,000 today. Should Carla sell a quarter of her stack (0.5 BTC) or borrow against it?

Keep Carla in mind as we explore the two options.

2.1 Selling: Quick Look

Capital-Gains Tax

Carla's cost base for her BTC is roughly $5,000 per coin. Selling 0.5 BTC today nets $50,000 and triggers a long-term capital-gain of $47,500. At a combined federal + state rate of 20%, she'll owe $9,500 in tax. Thus her net proceeds are $40,500.

Lost Upside

If Bitcoin doubles to $200,000 next cycle, Carla's 0.5 BTC would be worth $100,000, a $50,000 opportunity cost on top of the $9,500 tax bill.

2.2 Borrowing: The Tradeoffs

If Carla borrows $50,000 at 50% LTV

- Required collateral: ≈ 1.0 BTC (because $50,000 / 0.50 = $100,000 collateral value).

- Liquidation LTV (illustrative): 80%.

Liquidation price = Debt ÷ (BTC pledged × 0.80)

= $50,000 ÷ (1.0 × 0.80)

= $62,500

Takeaway: If Bitcoin drops 37.5% from $100k to about $62.5k, Carla will need to post additional collateral or her loan will be closed. To reset the loan to 50% LTV, Carla will need to post an additional 0.6 BTC.

3. Taxes in Plain English

In most jurisdictions:

- Selling BTC is a taxable event. You realize a capital gain or loss based on sale price minus cost basis. Short‑term gains (12 months or less) are usually taxed higher than long‑term gains (more than 12 months).

- Borrowing is not a sale. Receiving loan proceeds does not by itself trigger capital gains tax. Your tax basis and holding period continue.

- Interest deductibility depends on use of proceeds. In many jurisdictions, interest may be deductible only if the loan funds are used for investments or certain income‑producing activities. Personal use typically is not deductible. Keep clear records.

- Liquidation is a sale. If collateral is sold to cover the debt, that generally counts as a taxable disposition and can realize capital gains.

4. Risk Management Essentials

- LTV buffer: Start lower to survive drawdowns. Many borrowers consider it prudent to not exceed 50% initial LTV.

- Know the thresholds: Identify maintenance and liquidation LTVs, the pricing source, and how alerts are sent.

- Top‑up plan: Keep some BTC or cash unpledged so you can add collateral quickly.

- Rate, term, and fees: APR, origination fees, prepayment terms, and compounding determine true cost.

- Custody and rehypothecation: Who holds keys, and can collateral be lent out? Segregated, auditable custody reduces operational risk.

- Recourse: Understand whether the lender can pursue you beyond the collateral.

5. Who Should Borrow vs Sell

Borrow when you:

- Expect BTC appreciation and want to keep exposure.

- Can comfortably service interest and maintain a collateral buffer.

Sell when you:

- Need certainty and simplicity with zero margin‑call risk.

- Current rates and fees make borrowing uneconomic.

- Do not have sufficient collateral to survive a significant price fall (e.g. 50%)

6. Bottom Line

Borrowing against BTC can raise cash without losing future upside and creating a tax event. When borrowing, it is key to understand all the costs, maintain healthy collateral buffers, and pick the right lender. Selling may be the simpler path for many. The right choice depends on your goals, timeframe, and risk tolerance.

Wallet Pilot has a Free Calculator which you can use to run the numbers and compare lenders.

Friendly Disclaimer

This is general information, not financial or tax advice. Tax rules vary by jurisdiction and your circumstances. Consider speaking with a qualified professional before acting.