Real‑world asset (RWA) tokenization turned from a niche experiment into one of the fastest‑growing segments of on‑chain finance. From only about $5 billion in non‑stablecoin RWAs in 2022, total on‑chain RWAs surged to over $30 billion by September 2025. When stablecoins are included, the tokenized asset market exceeds $300+ billion. The market is dominated by private credit ($16.7 billion) and tokenized U.S. Treasuries (~$7.4 billion AUM), followed by institutional alternative funds ($2.3 billion), commodities (~$2.1 billion) and ect. Because of this, tokenization is no longer just a theory. On-chain funds are being tested by big Wall Street firms like BlackRock, Franklin Templeton, and Apollo. At the same time, governments in the U.S., EU, Asia, and the Middle East are making plans to deal with the change. Analysts now think that by the early 2030s, between 10 and 30 percent of all financial assets in the world might be tokenized. This would open up a market worth tens of trillions of dollars.

Current Market Trends

The market data showed a strong boost in the RWA market. By the end of December 2024, on-chain RWAs had already hit $15.2 billion. That number went over $24 billion just six months later and currently (Sep. 2025) it is over $30 billion. With stablecoins, the market is more than ten times bigger, with more than $280 billion worth of tokens. There has been growth across the board, but some asset classes stand out.

- Private credit is still the most important part of the industry, with $17 billion in loans and trade finance tools tokenized on-chain. Protocols like Maple Finance have led the way in creating institutional-grade loan pools that bring together retail and institutional money and deliver rates in the double digits. Even though credit markets are risky, Maple's completely collateralized business has kept investors' faith and set the stage for expansion.

- Tokenized U.S. Treasuries are the second main pillar. Their rise has been impressive: they went from less than $1 billion in early 2024 to more than $5.5 billion by spring 2025, and currently $7.7 billion with BlackRock's BUIDL fund alone making up almost half of the market. These tools connect traditional money market yields to the DeFi area and are soon becoming the foundation of crypto's "risk-free" yield curve. Franklin Templeton, Ondo Finance, Superstate, Circle, and OpenEden have all released competitive products that usually have yields of 4% to 5% after costs.

- There is also a layer of commodities, with roughly $2.1 billion in assets under management in Tether Gold (XAUT) and Paxos Gold (PAXG). There are new tests with copper and oil that show commodity-backed tokens could become a common way for on-chain investors to protect themselves against inflation.

- Real estate is sometimes called the best example of tokenization, although it is still very new, with a market value of less than $1 billion worldwide. But experimental programs in Dubai and Singapore show how big it may get. The Dubai Land Department has started putting property deeds on the blockchain, and DAMAC and MANTRA have announced a $1 billion effort to do the same for real estate in the area. Companies like Hamilton Lane and KKR are trying out partial tokenization of funds in the U.S. and Europe.

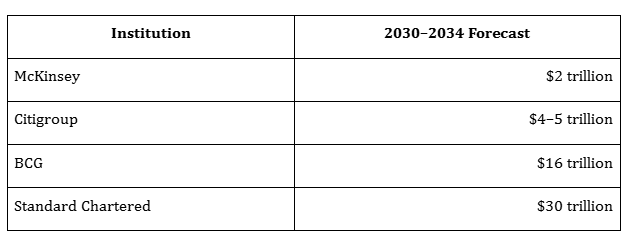

Forecasts illustrate the magnitude of potential expansion. McKinsey projects that tokenized assets could reach $2 trillion by 2030. Citigroup anticipates a market of $4–5 trillion, while BCG estimates $16 trillion, and Standard Chartered envisions $30 trillion by 2034.

What Changed in 2025

The year 2025 has started to feel like the moment when regulation, institutions, and technology finally began pulling in the same direction. What had been fragmented experiments just a few years earlier is now taking shape as a more coordinated global shift.

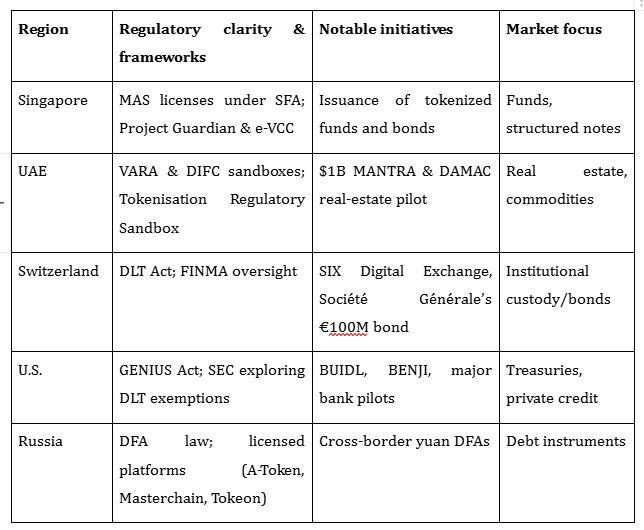

In the United States, July brought the passage of the GENIUS Act — the country’s first federal law focused entirely on stablecoins. It laid out clear rules on reserves, audits, and compliance, and limited issuance to banks and licensed players. A couple of months earlier, the SEC had gathered industry leaders for its first tokenization roundtable, where it floated the idea of exemptions that would allow tokenized securities to trade directly on distributed ledgers. Even the banking regulators, who once sounded alarms about digital assets, softened their stance this year, giving banks the green light to expand into custody and tokenization services.

Europe is also moving quickly. MiCA, which originally dealt mostly with stablecoins and utility tokens, is now being extended through a broader “Savings and Investment Union” package to cover tokenized equities, bonds, and derivatives. The EU’s DLT Pilot Regime — in place since 2023 — allowed selected institutions to experiment with trading and settlement under lighter rules. By mid-2025, the results were strong enough that regulators recommended scaling it up across the bloc.

In Asia, pragmatism is paying off. Singapore continues to require token providers to be licensed under the Payment Services Act, while its Project Guardian has graduated from pilot phase to real commercial use. The city-state also introduced Project e-VCC, a blockchain-native fund structure. Hong Kong has leaned heavily into tokenized green bonds, issuing HK$6 billion worth in 2024 alone, and Japan now counts about ¥140 billion (roughly US$1 billion) in outstanding digital securities.

The Middle East is carving out its own role. The UAE has reinforced its position as a regional hub through VARA and DIFC sandboxes and, in 2025, a dedicated Tokenisation Regulatory Sandbox. The Dubai Land Department even launched a real-estate tokenization pilot early this year. Altogether, the UAE’s tokenized asset market is now estimated at around $17 billion.

And then there is Russia, where growth has been dramatic. Under the Digital Financial Assets law, volumes surged seven-fold in 2024 to reach 684 billion rubles and by mid 2025 bypassed 1 trillion rubles. Alfa-Bank’s A-Token platform holds about 60% of the market, Masterchain another 20%, and Tokeon around 5%.

Institutional and Platform Developments

By 2025, institutional adoption of tokenization had clearly shifted into higher gear.

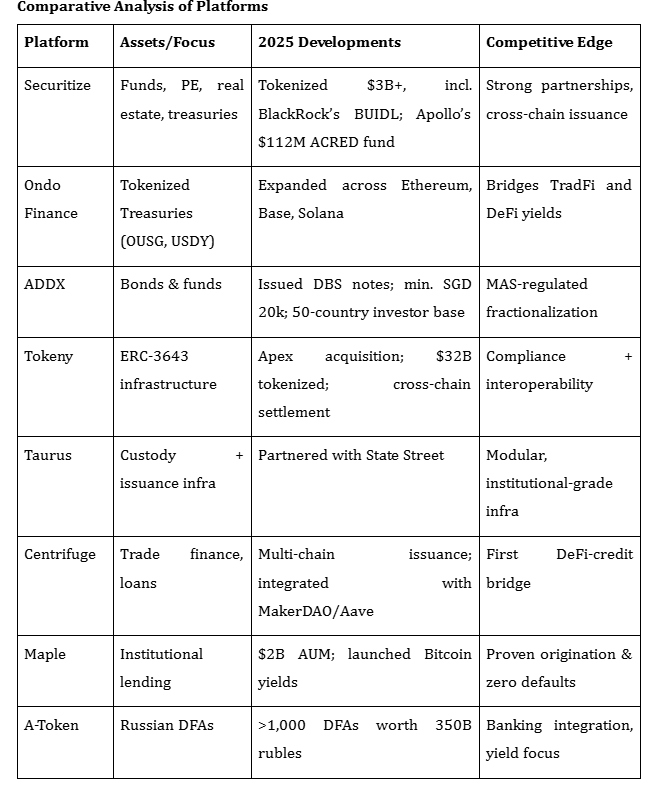

Securitize took a major step forward by tokenizing more than $3 billion in assets, among them Apollo’s $112 million Diversified Credit Fund. It also secured its role as tokenization partner for BlackRock’s BUIDL fund, cementing its place at the center of institutional activity.

Tokeny had a pivotal year as well. After being acquired by Apex Group in May, it teamed up with SkyBridge Capital to tokenize $300 million worth of hedge funds and showcased a delivery-versus-payment model that worked seamlessly across chains in collaboration with ABN AMRO and Fasanara.

Traditional finance is also laying down deeper infrastructure. State Street partnered with Taurus to develop modular tokenization and custody systems built on Hyperledger Besu, positioning itself for a market where regulatory barriers are softening — especially as the SEC revisits earlier restrictions.

In Singapore, ADDX continued to make private markets more accessible by issuing tokenized structured notes with DBS. This move cut minimum investment requirements to just SGD 20,000, compared with the traditional $100,000, broadening the pool of eligible investors.

DeFi as the Distribution Layer

By 2025, DeFi wasn’t just an alternative — it had become the engine room where tokenized assets are issued, managed, and put to work.

Take Maple Finance. Once seen as an experimental credit protocol, it has now transformed into a fully over-collateralized lending platform built for institutions. With more than $2 billion under management, Maple rolled out new products — including a Bitcoin yield instrument paying 5.28% APY — that made it hard for traditional players to ignore.

Morpho v2 pushed efficiency even further. Its new model introduced intent-based, fixed-rate lending and added KYC-enabled whitelists for compliance. Just as important, it slashed gas fees by 70%, making it far cheaper to use. The results spoke for themselves: by June 2025, investors had locked in $4.2 billion.

On the allocator side, MakerDAO’s Spark Protocol emerged as one of the biggest players, deploying over $3.5 billion across treasuries and DeFi. Its portfolio read like a who’s who of tokenized finance: $800 million into BlackRock’s BUIDL, $400 million into Janus Henderson’s Anemoy Treasury Fund, and $300 million each into Superstate, Maple’s syrupUSDC, and Ethena’s sUSDe.

And to tie it all together, Chainlink rolled out its Automated Compliance Engine (ACE) in June 2025. By embedding KYC and AML rules directly into tokens themselves, ACE could finally bridge the gap between DeFi and the world of large-scale institutions — potentially unlocking access to the $100 trillion in capital they control.

Geographic Landscape and Leading Hubs

The global tokenization landscape is now anchored in several hubs with distinct regulatory and market strengths.

Comparative Analysis of Platforms

Future Outlook

Looking ahead, private credit is likely to remain the strongest near-term segment. Double-digit yields and the persistent demand for SME financing make it an attractive play for both institutions and investors. Tokenized treasuries, which ballooned from $858 million in early 2024 to more than $5 billion by mid-2025, are set to keep their lead in retail and DeFi portfolios thanks to their simplicity and daily liquidity. Commodities, while offering inflation protection, still occupy a relatively small niche. Real estate, however, remains the “sleeping giant” — and large-scale pilots like the UAE’s $1 billion program may finally unlock momentum once regulatory clarity catches up.

Over the longer term, the pace of growth will hinge on a few critical enablers. First, regulatory harmonization: initiatives like the EU’s Savings and Investment Union and possible U.S. exemptions for DLT-based trading are early but important moves in that direction. Second, technology standards: interoperable frameworks such as ERC-3643 and cross-chain networks like LayerZero and CCIP will make it possible to achieve true atomic settlement across platforms. Third, settlement assets: the market needs reliable, regulated vehicles — whether stablecoins or wholesale CBDCs — to support large-scale delivery-versus-payment transactions.

Beyond that, the infrastructure for harder-to-trade assets has to mature. Stronger oracles for illiquid instruments, deeper secondary markets, and liquidity aggregation mechanisms will be essential to bring scale. And finally, the human factor: investor trust. Clear legal structures, custody guarantees, and insurance protection will be the ultimate test of whether tokenization moves from early adoption to mainstream finance.

Conclusion

By 2025, real-world asset tokenization isn’t a side story anymore — it has become one of the defining features of digital finance. Non-stablecoin RWAs have grown past $24 billion, while stablecoins bring the overall tokenized asset market above $240 billion. Private credit and tokenized treasuries are leading the way, commodities are carving out a role as a hedge, and real estate — long seen as the “sleeping giant” — is finally beginning to stir. Big names like BlackRock, Apollo, and Franklin Templeton are fully engaged, while DeFi platforms such as Spark and Pendle are weaving RWAs directly into yield strategies. Regulators from Washington to Brussels to Singapore, Dubai, and Moscow are no longer watching from the sidelines — they are actively shaping the rules of the game.

Of course, the road ahead isn’t without hurdles. Rules remain fragmented, liquidity pools are still siloed, and questions about legal enforceability haven’t fully been put to rest. But the bigger picture is clear: tokenization has moved from being an experiment to becoming central to how modern finance works.

The real unknown is what the next decade will look like. Will the world move toward shared standards, global liquidity, and seamless cross-border settlement? Or will we end up with strong but separate regional hubs? Either way, the trajectory is set. RWAs are reshaping how capital is created, traded, and held — building a bridge between traditional finance and the programmable digital infrastructure that is starting to define the future.

Questions Ahead:

By 2025, tokenization is no longer theory — it’s happening. But the next phase will be defined by a few big questions.

- Will tokenization run on harmonized global rules that unlock seamless cross-border liquidity, or will hubs like Singapore, the UAE, and Switzerland build their own standards and compete with fragmented markets?

- DeFi platforms like Spark, Maple, and Pendle already channel billions into RWAs. Can they become the main distribution layer, or will big investors still prefer regulated, centralized venues for large allocations?

- As settlement assets, will wholesale CBDCs emerge as the universal “cash leg,” or will stablecoins like USDC — already liquid and widely used — remain the backbone of tokenized markets?