Our second article of this series, which explains different types of DeFi investment apps for beginners/non-crypto natives is here!

Decentralized Finance (known as DeFi) is a collection of apps, website, and products that do things similar to what banks and financial institutions do in the regular world, but on a blockchain. In this article, we will walk through what some of these projects are, and how they compare with each other in terms of risk and safety.

If you enjoy our content and want to show you support, please tap on the "tip" button below, to send us a $0.01 tip for FREE!

A quick glossary refresher:

- A stock exchange in DeFi is known as a DEX, or Decentralized Exchange. One example is Uniswap.

- And a savings account, just like in a bank, is known as a savings project in DeFi. One such example is AAVE.

- And companies, that run and direct businesses, are called DAO's in DeFi. One such example is Maker DAO.

- Liquidity, means pretty much the same thing as in traditional finance. Exchanges that have high liquidity make it easier to buy and sell stocks for cash, by having a high number of available buyers and sellers on their platform. More on that in our DeFi Concept explainer (upcoming article).

Today we will be talking about some concepts which only exist uniquely in DeFi such as Liquidity pools and yield farming.

Disclaimer: DeFi Desk is an entertainment platform, and not a source of financial advice. You must remember that you are wholly responsible for any and all investment decisions that you make, whether they lead to life-changing profit or loss. You are the sole driver of your caravan, which may include your family (if you are providing for one), so do consult a professional and make sufficient research before investing in any products mentioned.

3rd layer - Liquidity

Providing liquidity is a profit strategy in DeFi, that works by getting liquidity fees. It is considered medium risk to high due to the possibility of loss. However, it is also a very rewarding strategy that can pay off exponentially well if you make smart choices.

If you'd like to explore lower risk strategies, do check out our first "7 layers" article here: The 7 Levels of Risk — DeFi Investments Explained, Savings & Strategies

This strategy is built on the concept of liquidity—Big platforms have it, small platforms want more of it. This is because, more liquidity is equal to more buyers and sellers, faster trades, and better prices.

In DeFi, liquidity is being supplied by a 'liquidity provider', or someone who deposits tokens into a 'liquidity pool'. We say that they are providing 'liquidity' to the market, because the more they provide, the more 'liquid' a market will be.

There are several sub-concepts that we will explain in this section:

- Liquidity Pools

- Depositing Liquidity

- Trading fees

- Impermanent loss

Liquidity Pools

Liquidity pools are what allows traders to trade in DeFi, or what is known as swapping, which happens in Decentralized Exchanges (DEX's).

The demand for liquidity in DEX's are high because most traders will want to use swaps in order to buy or sell a token instantly, and not all tokens are listed in centralized exchanges like Coinbase, Kraken, or even Binance. There often hefty listing fees or a complicated application processes involved to get your token listed, and so most projects don't bother listing their tokens until they become large enough for that to be a concern.

In this way, there are many small or unknown projects, or even sizeable ones like Balancer (worth $653 million USD) that don't make a huge effort to get listed on centralized exchanges, but always ensure that they have significant liquidity in DEX's like Uniswap or Sushiswap (or on their own platform, where Balancer has their own decentralized exchange).

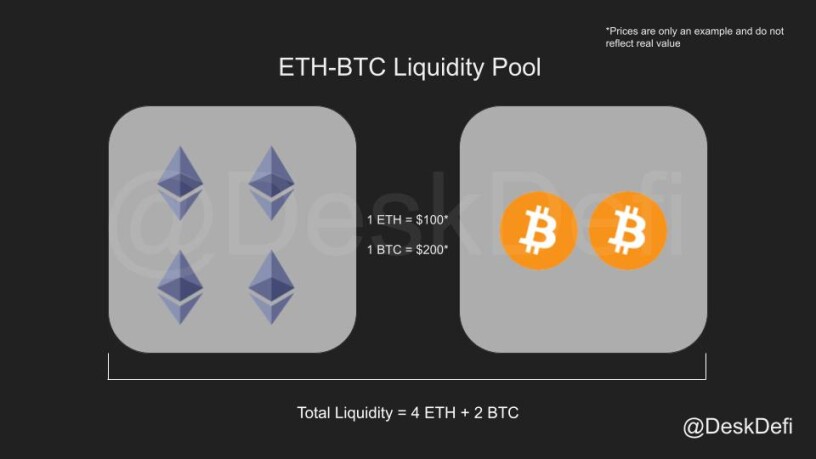

Most liquidity pools are actually made up of pairs of two tokens (or in some cases, three or four tokens) that allow traders to swap one token directly for another. These pairs are arranged to have equal in value on both sides. In this example of an ETH-BTC pool, both sides are worth $400* each:

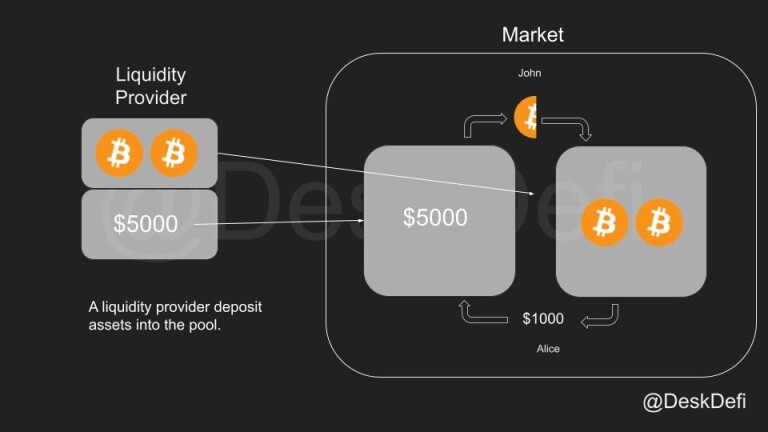

Depositing Liquidity

Here's a simplified diagram of how depositing works:

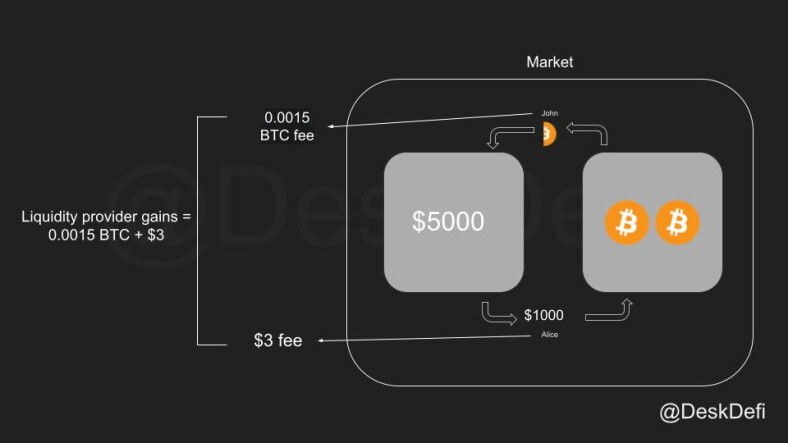

Trading fee

Providing liquidity allows other traders to trade using the assets provided. In return, liquidity providers also gain a 0.3% fee paid by traders, for all the trades that happen in their liquidity pool:

*Prices used are for educational purposes only.

Impermanent loss

Impermanent loss is the concept that, as one token price changes (goes up or down) relative to the other token in a pair, the pair will start to lose some value as a result of rebalancing. A Liquidity pool rebalances itself to maintain equal value on both sides. With trading activity, one side will often become unequal, and the other side will have to be rebalanced to match its value.

Basically, as the price of tokens go up and down, liquidity providers lose a little extra money because of rebalancing. This is known as "impermanent loss" because you can presumably stay in a pool long enough for the trading fees to make up for it.

However, most of the time, this is not desirable. And so liquidity providers should avoid pools with high impermanent loss because they can lose their initial investment very quickly if the token price is volatile (changes a lot in a short period of time).

Low-risk pools

The best liquidity pools are those with high volume and low impermanent loss. Stable pairs such as USDC-DAI have almost 0 impermanent loss, because their price rarely changes. However, the downside is, there are usually not much rewards to be gained from these pairings because there is a much higher amount of deposits (since it is seen as safe) compared to trading volume. These can pay anywhere from 3-10% APR in fees.

There are some pools which are considered "lower risk", such as USDT-ETH which experience a high volume but with less depositors, and so pay out a higher fee reward for depositors. This can average anywhere from 30%-70% APR.

If your aim is to have steady gains, you would be able to achieve that with one of these pools. You can also research pools on your own with websites that provide DeFi pool analytics such as apy.vision.

However, note that even "lower risk" pools have significant risk involved due to the volatile nature of crypto in general, so I would recommend doing your due diligence and testing before attempting to invest a large amount.

Everything else—Medium to Extremely High risk

Pretty much everything other than stable pools are considered fair game for risky players. You can do your research to find liquidity pools that you would like to invest in.

The best pools would be those with low impermanent loss (or lower compared to fees earned), high volume (lots of daily transactions), and low reserve (less other people to share the fees with).

If you want to gain the most fees, providing on Uniswap (for Ethereum) or Quickswap (for Polygon) would be the smartest move since they have the most volume on their respective platforms! However, do your own research first as there can be some pairs that do better on certain exchanges (e.g. Sushiswap may have better volume for certain pairs). You can do this with aforementioned tools like apy.vision.

In conjunction with the gains from trading fees, some liquidity providers can enjoy an additional benefit, known as yield rewards.

Let's explore this in the following section :

- Yield Rewards

- Yield Depreciation

- Governance and Fee-sharing

- Compounding Vaults

4th Layer - Yield Farming

Yield farming is the strategy of accumulating yield rewards. Yield rewards are a kind of 'bonus' for providing liquidity to a market, and these rewards are paid out by the platform that benefits from it. They are often paid using a token unique to the platform. For example, Sushiswap pays liquidity rewards in the SUSHI token. Balancer pays rewards in the Balancer token (BAL). Pickle finance pays rewards in the PICKLE token, and so on, and so forth.

SUSHI is the most well known token for this because they used this tactic to attract liquidity providers from Uniswap, back in September of 2020. By providing rewards, they were offering an additional income source for liquidity providers who couldn't earn as much on Sushiswap through fees (because most traders were using Uniswap, the first and largest DEX).

These rewards are paid on an ongoing basis, until the liquidity reward program is over. The calculation of profit from these rewards is generally shown as 'APR' (annual percentage rate), which is the % of returns per day multiplied by the number of days in a year (365).

APR = daily rewards * 365

Reward Depreciation

Today, this same model is used all across DeFi by various projects, as a way of attracting new investors and liquidity providers to their project, and also for rewarding long term holders who continue to provide liquidity.

However, one problem faced by all platforms who give liquidity rewards is that, inevitably, the reward token's price will depreciate over time as users sell it (usually to ETH or to USDC/DAI) to realize their profit. This reduces rewards for holders and can also make a reward program grow less attractive over time. If left unchecked, the inflationary effects of minting reward tokens can even cause a token's price to plummet to 0, which would lead to a near 100% loss for reward token liquidity providers.

The worst culprits of reward depreciation are projects (often called 'farms') that offer ludicrous rates of return ("~50,000% APR") which were both unrealistic and unsustainable. Paying these rewards doesn't cost anything to the platform, but they would need to give people a reason not to sell those tokens, or it will quickly become worthless.

Can I really get returns of 50,000% a year?

Unfortunately, no.

These reward tokens might experience a short period of pumping, maybe in the first day, as new investors pour in. But as soon as the time is ripe, the creators of the platform can start selling their stake, and cash out before the crash. This means that usually, if the returns sound too good, then token it's being paid in is probably on its way to becoming worthless.

This is usually the case on Binance Smart Chain (BSC) platforms, but also seen on Polygon. This loss is absorbed by liquidity providers who provide the tokens for a reward pool because people who sell are using their pool to do so, which depreciates their holdings' overall value.

But there are ways for platforms to extend the lifespan of their reward tokens, perhaps even indefinitely, by giving it a purpose in their ecosystem:

Governance and Fee-sharing

To combat this, many projects offer a share of the platform fees, voting power, or some other incentive from staking these reward tokens. PICKLE holders can stake their PICKLE to gain DILL, which is a governance and fee-sharing token. Sushiswap has a similar program for SUSHI holders to stake SUSHI and receive xSUSHI, which also has governance and fee-sharing built in.

This slows down the selling of SUSHI and PICKLE, since now people have a second use for it. Instead of selling it now and realizing profits, they can stake it and earn passive income from the platform over time.

The 'fee' that is being shared is usually predefined. On Sushiswap, the fees earned by xSUSHI holders come from 0.005% of every trade. This is because liquidity providers only receive 0.025% fees on each trade, which is less than the usual 0.03% earned on most exchanges. Pickle finance gets fees from every depositor by charging a 'performance fee' on the profit that they make from using the platform's vaults. This fee is then distributed to DILL stakers.

In this way, it turns the reward tokens into 'shares' of the underlying project much like company stocks, receive constant dividends from the profits earned, and incentivizes people to hold on to these tokens as 'shareholders', people who can both vote on and discuss the company's overall direction.

In DeFi, many projects who follow this method of 'shareholding' are effectively 'owned' by their 'shareholders', who all have a say and an interest in the project's long-term success. This is also what is known as a 'DAO' (decentralized autonomous organization).

Next, we'll explain the type of business model run by Pickle Finance, which is known as a 'yield aggregator' or 'vault'.

Compounding Vaults

'Compounding vaults', 'auto-compounder', and 'yield aggregator' are used interchangeably, and generally refer to the related, but slightly different things:

A yield aggregator is a platform (like Pickle Finance) that provides 'vaults' as well as an 'auto-compounding' service. This helps liquidity providers sell their yield rewards (mentioned in above section), and compound (selling and depositing) it into their liquidity pool, to generate a bigger share of fees and rewards over time.

In other words, a vault turns your liquidity pool investment into a compound-interest machine. The return generated (in fees and rewards), will be used to purchase more shares of the liquidity pool automatically over time.

How often is compounding done?

On Ethereum this is usually done once a day by the compounding vault, and on Polygon and BSC this is done multiple times a day, or even multiple times a minute. The second type can lead to network clogging which is an issue facing low-fee, high transaction volume networks that host DeFi projects.

What does compounding do?

In short, it increases your profit exponentially. For those who don't understand exponentially, just imagine you are drinking a glass of water. Now imagine that as you drink, the glass slowly doubles in size. It keeps doing this every half-second, until it soon becomes the same volume as an Olympic swimming pool.

Now you can't realistically keep drinking that way. And that's a quick visual explanation of how exponential gains work.

Alright getting back to compounding, the best way is for you to see for yourself. Try this compounding interest calculator. Let's try $10,000 as the principal, and 10% as the interest rate, and the period as 2 years. Try to set the compounding frequency from yearly, to monthly, to weekly, and then to daily to see the difference in result. You'll see that daily compounding greatly increases the final return on investment.

Yup, that's how it goes. With compounding, your investments grow a lot faster in the same timeframe.

Why does a yield aggregator do this?

Yield aggregators charge a performance fee on profits of deposited assets. On Ethereum, this is commonly 15-30%, while on Polygon this can be lower at 5-15%.

Which yield aggregator should I choose? There are so many!

Different yield aggregators can have unique functions and mechanics to reward its long-term supporters. This can include: unique reward accumulation mechanics (Dracula), their own yield reward programs (Beefy), and fee-sharing (Adamant).

Dracula Protocol is a yield aggregator which has a special function of turning yields into ETH upon collection. Many people like holding ETH and not reward tokens because ETH has much wider acceptance as a cryptocurrency and, in some people's eyes, may have better price growth potential over time. To be able to automate this selling of rewards to ETH saves a lot of hassle and even gas costs for individual investors.

Adamant finance charges a hefty performance fee (30%) but pays all of it to those who stake its reward token, creating a positive feedback loop between depositors and stakers, protecting its own self-interest and those of its investors and depositors in the long term.

Alright, that's part 3 and 4 of our introduction series on DeFi protocols. Follow us on publish0x, or on Twitter @DeskDeFi for updates for the rest of the series!

Also, if you'd like to contribute to our treasury (to fund more articles and cool collaborations), kindly send your donation to this ETH address: 0x97948926f530f189110362C866Bc73812357de1f

We accept all contributions! But we'd prefer ETH, USDC, or DAI if you have it. Thank you for reading, and see you again Crypto-cowboys!