Wallet adoption, regulatory clarity, and fintech innovation fuel an unstoppable wave of digital dollarization as PayPal, Western Union, and JPMorgan join the race.

The evolution of money is rarely linear. It is shaped by innovation, regulation, market demand, and increasingly, by the quiet momentum of digital infrastructure. In 2025, the landscape of digital finance is undergoing one of its most critical transformations yet, driven by stablecoins. With the recent passage of the GENIUS Act in the United States, a new chapter has begun—one that promises regulatory clarity, institutional embrace, and mass-market adoption of this once-niche asset class.

The Regulatory Breakthrough

In July 2025, the U.S. government took a decisive step by enacting the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act), providing long-awaited legal clarity around stablecoin issuance and digital asset classification. This landmark legislation marks a turning point in how the financial system interacts with blockchain-based value.

Under the GENIUS Act, stablecoins must meet transparency standards, undergo third-party audits, and maintain full 1:1 fiat reserves. It also defines the boundaries between payment stablecoins, securities-backed tokens, and algorithmic models, giving developers and financial institutions alike a robust framework for compliant innovation.

In response, Bank of America has projected a sharp uptick in stablecoin supply, estimating an increase of $25 billion to $75 billion in the near term. This forecast not only reflects market optimism but also a structural shift in how capital is flowing into blockchain-based ecosystems.

A Decade of Progress

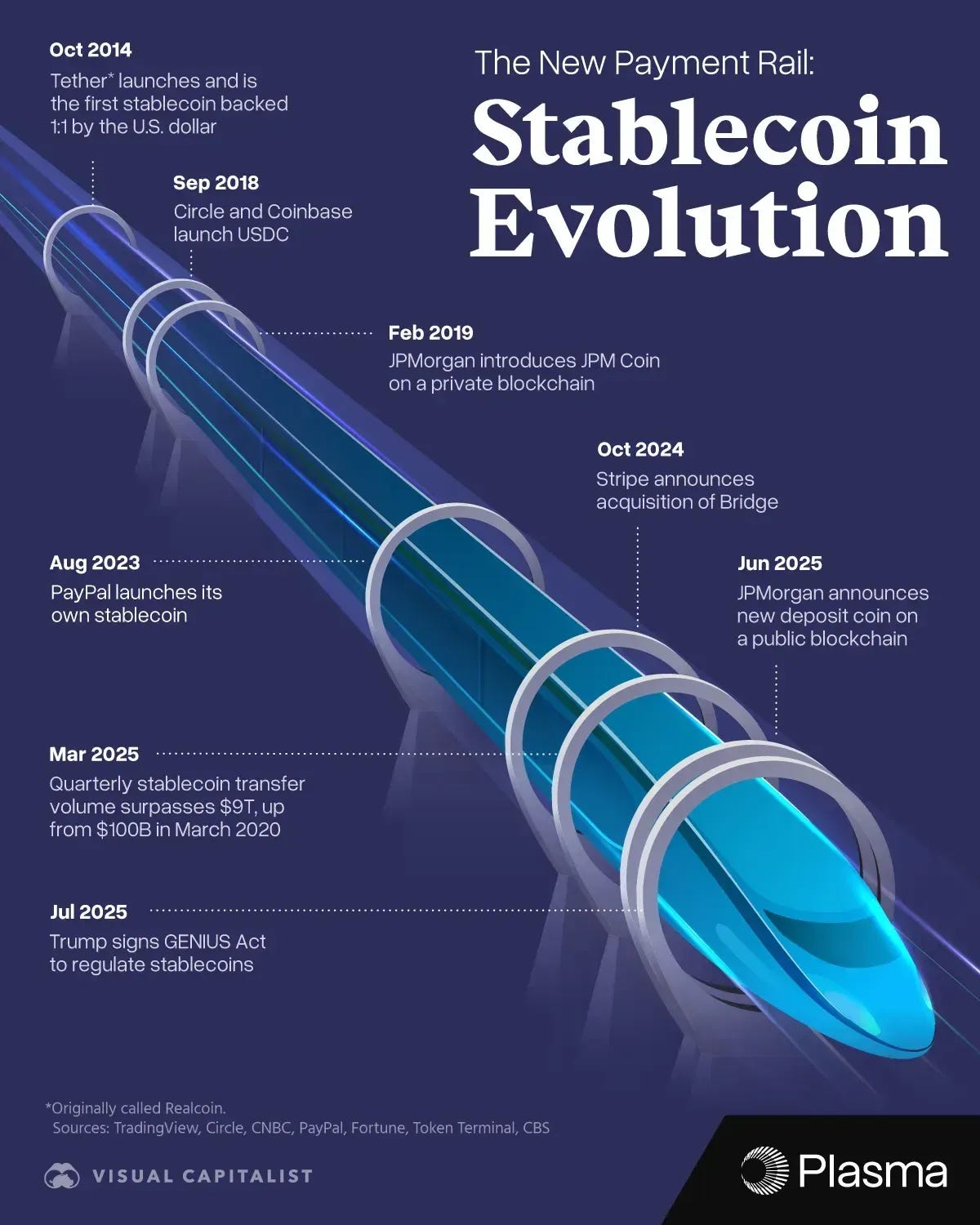

As illustrated in the infographic below, the stablecoin story began in October 2014, when Tether launched the first dollar-backed stablecoin (originally known as Realcoin). Since then, key milestones have marked the asset’s journey into mainstream finance:

-

September 2018: Circle and Coinbase introduced USDC, a fully reserved dollar-backed stablecoin that became the gold standard for transparency, now the second-largest stablecoin.

-

February 2019: JPMorgan launched JPM Coin for internal settlements on a private blockchain, heralding the corporate entry into digital cash equivalents.

-

August 2023: PayPal launched its own stablecoin (PYUSD), a clear indication of fintech’s growing role in reshaping digital value exchange.

-

March 2025: Quarterly stablecoin transfer volumes exceeded $9 trillion, up from just $100 billion in March 2020.

-

June 2025: JPMorgan expanded further, announcing a deposit coin on a public blockchain, breaking with their previously private-led strategy.

-

July 2025: The GENIUS Act became law, setting the stage for an explosion of new stablecoin products and infrastructure.

The Rise of Utility and Wallet-Level Adoption

Beyond policy and regulation, user behavior is telling its own story. According to recent blockchain analytics, 38% of all crypto wallets now hold stablecoins, outpacing even Solana in wallet penetration. This signals a clear preference for low-volatility, utility-driven assets, especially in regions dealing with currency instability or limited banking access.

Ethereum still dominates in terms of transaction volume, but escalating gas fees are driving users to faster and cheaper alternatives. Solana and Tron have emerged as stablecoin powerhouses due to their low transaction costs, high throughput, and expanding DeFi integrations. For the average user, the choice is becoming less ideological and more functional: which network gets the job done faster and cheaper?

PayPal World: Competition or Validation?

In a surprising pivot, PayPal unveiled PayPal World—a non-blockchain payments platform that mimics stablecoin functionality using fiat rails. It offers real-time settlement, cross-border payments, and digital wallet integration—without the overhead of public blockchain infrastructure.

While some in the crypto community see PayPal World as a threat to permissionless finance, others argue it validates the core use case of stablecoins: fast, borderless, and user-centric transactions. More importantly, it signals to legacy players that the next phase of payments will not wait for decades of traditional banking evolution.

PayPal World’s architecture mirrors that of centralized stablecoins like USDC—but without the decentralization, auditability, or composability that make public blockchain assets so powerful. If anything, its entry may push users who prioritize transparency and interoperability toward blockchain-based alternatives.

Legacy Giant Western Union Enters the Arena

One of the most unexpected entrants into the stablecoin race is Western Union, the 175-year-old remittance giant. CEO Devin McGranahan recently confirmed that the firm is running stablecoin pilots in Latin America and Africa, to integrate them into:

-

Cross-border remittances

-

Local currency conversion

-

Digital wallet infrastructure

This development is significant. Western Union operates in over 200 countries and processes hundreds of millions of remittances annually. If stablecoins can reduce fees, improve settlement speed, and offer local currency flexibility, it could reshape the company’s role from legacy remittance provider to a global fiat-crypto on/off-ramp.

In regions plagued by inflation, currency devaluation, or banking exclusion, stablecoins offer not just innovation but financial liberation.

Where Do We Go From Here?

Stablecoins are no longer a speculative corner of crypto—they are rapidly becoming the backbone of digital commerce. With major regulatory clarity now in place via the GENIUS Act, institutional entry is accelerating, wallet adoption is spiking, and traditional payment firms are rushing to modernize.

Yet questions remain. Will regulators globally adopt similar clarity? Will CBDCs compete or complement stablecoins? How will decentralized stablecoins like DAI or algorithmic models adapt under this new scrutiny?

What’s clear is that stablecoins are not a passing phase. They represent a new payment rail—a programmable, borderless, and efficient form of value that transcends old systems. And with the infrastructure, legal frameworks, and user demand now aligned, the next decade will likely see stablecoins evolve from digital dollar proxies into core components of the global financial system.

Originally Published on Substack.