Big Tech’s capital spending on AI hits record highs as investors cheer and risks mount.

In a remarkable show of confidence—or perhaps collective urgency—Silicon Valley’s biggest players are pushing AI spending into uncharted territory. Last week’s earnings reports from Meta, Microsoft, Apple, and Amazon made one thing strikingly clear: artificial intelligence is no longer a side bet or an exploratory initiative—it is the strategic battleground.

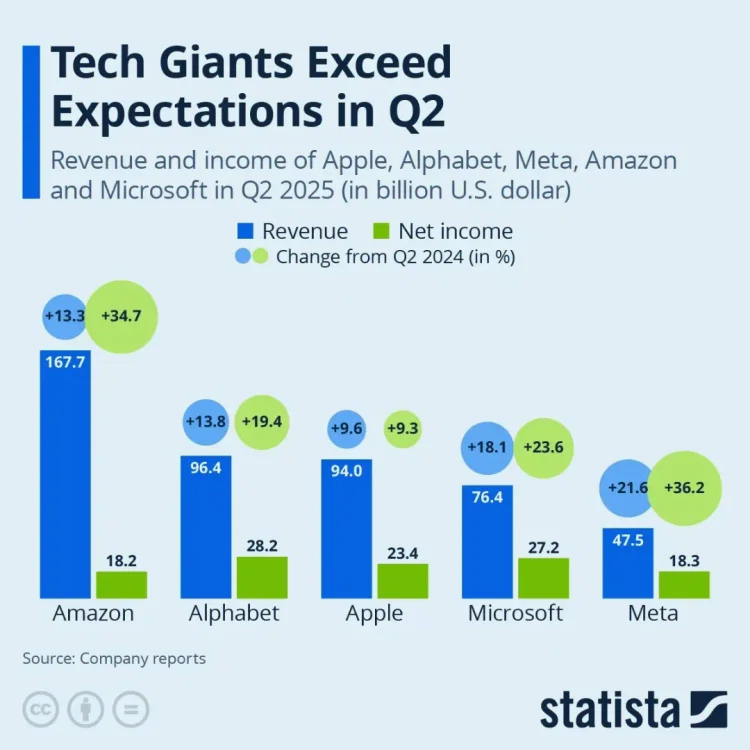

Meta’s and Microsoft’s quarterly disclosures captured headlines, not just for their earnings, but for the sheer scale of their AI-related capital expenditures. Microsoft, in particular, made waves with its declaration that it expects to spend over $100 billion in fiscal year 2025, with $30 billion this quarter alone—a record-setting pace that dwarfs its past capital outlays. And it’s not just infrastructure. Microsoft’s strategic partnership with OpenAI has already become emblematic of the company’s ambition to dominate the enterprise AI space.

Meta, meanwhile, is playing catch-up—but doing so aggressively. Mark Zuckerberg, in a rare moment of admission, acknowledged that Meta had “fallen behind” in AI innovation. Since then, the company has engaged in what could be described as a recruitment blitz, including the poaching of OpenAI engineers with multi-million-dollar packages. The company’s capex (capital expenditures) is projected to reach $35 to $40 billion this year, largely focused on building AI infrastructure and capabilities, particularly around their Llama model and AI agents.

Apple’s approach was less flashy but no less important. Although its better-than-expected quarterly earnings were driven by resilient iPhone sales, CEO Tim Cook made it clear that AI was about to become a larger part of the company’s strategy. Apple has long been more cautious in making bold AI announcements, but during the earnings call, Cook committed to “significantly” expanding AI investment—and left the door open for acquisitions to fill any gaps. And Amazon? While less explicit in its figures, the company continues to ramp up AI infrastructure through AWS, which is becoming the platform-of-choice for many foundational model developers.

Investor Sentiment Defies the Norm

Traditionally, capex that exceeds expectations tends to weigh on investor sentiment. Large spending often triggers concerns about bloated budgets, diminishing margins, and uncertain ROI. But last week flipped that expectation on its head. Instead of punishment, Meta and Microsoft were rewarded by the market, with both companies seeing a pop in their stock prices following the announcements.

This suggests that investor psychology around AI is shifting—rather than fearing overinvestment, markets now appear to view bold AI capex as a proxy for future dominance. This optimism is rooted in the notion that we are still in the early innings of AI adoption. Unlike prior tech trends that often plateaued quickly, AI seems to be evolving into a general-purpose technology, much like electricity or the internet. If that’s true, then the companies laying the deepest foundations today—via data centers, custom chips, and AI talent—will control the infrastructure of tomorrow.

The Strategic Logic—and the Potential Pitfalls

To be clear, there is a strategic logic behind this frenzy.

- Control of compute and model development: The companies investing heavily aren’t just betting on applications—they are investing in the stack: silicon (NVIDIA, custom chips), infrastructure (cloud and data centers), models (Llama, GPT, etc.), and interfaces (Copilot, Reels, Siri).

- Platform control: Just as Apple became a platform for mobile apps and Google for search, the next generation of AI platforms may become gateways to billions in recurring revenue through subscriptions, licensing, and enterprise contracts.

But here lies the paradox. The demand that is expected to justify these outlays is still in its infancy. The generative AI market, while promising, has yet to yield consistent, mass-market monetization. So far, most use cases remain experimental, productivity-enhancing, or niche. If the revenues from AI adoption fail to scale at the same pace as capex, these investments could turn from visionary to burdensome.

Lessons from the Past: The Dot-Com Echo

It’s worth remembering that many of the same dynamics—buzzword-heavy optimism, VC-fueled valuations, and infrastructure-first strategies—were present in the late 1990s during the dot-com boom. Back then, companies spent massively on data centers, fiber optics, and web infrastructure before the consumer and enterprise markets were ready. Eventually, the demand did come, but not before a painful correction wiped out hundreds of over-leveraged firms. Silicon Valley’s AI bet is arguably more grounded today, with clearer use cases across healthcare, finance, logistics, and productivity. But the risk of overpromising and underdelivering remains.

The Open Question: Strategic Spending or Hubris?

So, what does this mean for the broader tech ecosystem? Smaller firms may find themselves squeezed as Big Tech monopolizes talent, infrastructure, and capital. Regulators may become more watchful as these firms consolidate power through AI dominance. Meanwhile, the public, increasingly aware of AI’s implications, is beginning to question how this rapid innovation wave will affect jobs, equity, and truth itself.

As investors and observers, we should be asking: Are these bold AI investments a strategic masterstroke or a signal of corporate overreach?

Originally Published on LinkedIn.