A decade-long pricing model shows Ethereum trading at a deep discount to Bitcoin. Is this a rare buying opportunity or the new normal for altcoins?

Bitcoin remains the undisputed heavyweight of crypto — a store of value, an inflation hedge, and now a mainstream financial product thanks to the success of spot Bitcoin ETFs in the United States. Ethereum, meanwhile, has long positioned itself as something different: a platform for decentralized finance (DeFi), non-fungible tokens (NFTs), and smart contracts that run the Web3 ecosystem.

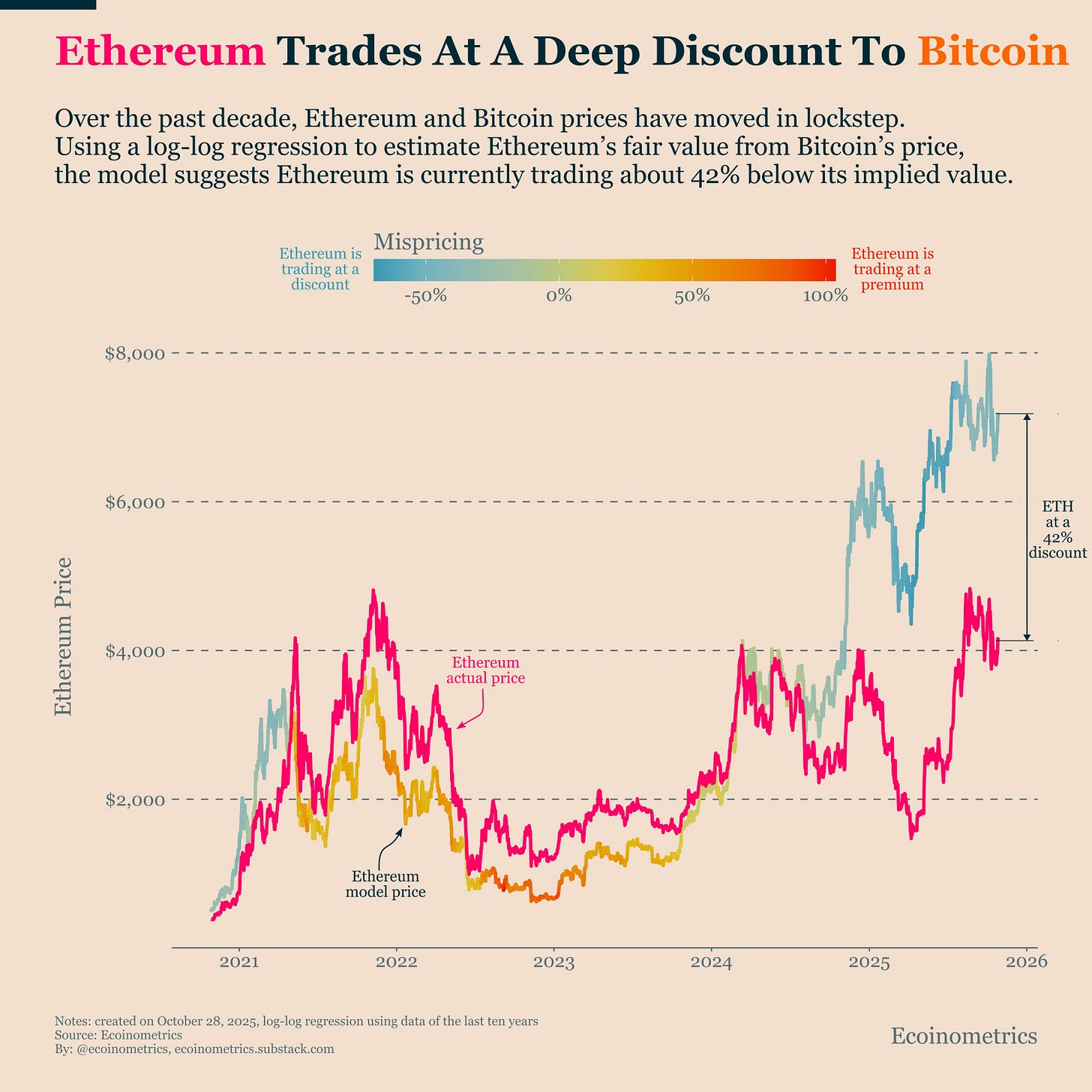

For much of their shared history, Ethereum’s price movements have mirrored Bitcoin’s, albeit with higher volatility. When Bitcoin rallies, Ethereum tends to follow; when Bitcoin corrects, Ethereum often falls harder. This correlation has been so consistent that analysts at Ecoinometrics have used log-log regression models to estimate Ethereum’s “fair value” based on Bitcoin’s price — essentially asking, if the historical relationship holds, where should Ethereum be trading right now?

This model of Ethereum’s and Bitcoin’s price movements suggests that if history holds, Ethereum’s fair value should be significantly higher than where it stands today. The chart paints a clear picture: Ethereum has underperformed its implied valuation by a wide margin, even as Bitcoin’s institutional ascent continues.

Modeling Mispricing: What the Chart Tells Us

The Ecoinometrics model uses data from the last ten years to map Ethereum’s implied price versus its actual price. The resulting chart reveals several key moments where Ethereum traded at a significant discount or premium to Bitcoin.

-

Early 2021–2022: Ethereum reached parity with its model price, even trading at a premium during the height of the NFT and DeFi boom. ETH hit near $4,800 as retail and institutional excitement surged.

-

Mid-2022–2023: Following the Terra/Luna collapse and the broader crypto bear market, Ethereum’s actual price fell well below its model value, reflecting shaken confidence and risk aversion.

-

2024–2025: Bitcoin’s resurgence, driven by institutional flows into ETFs and broader macro tailwinds, wasn’t matched proportionally by Ethereum. This divergence widened into a 42% discount, the deepest since the 2022 capitulation.

At face value, the data implies that Ethereum is trading far below its fair historical relationship to Bitcoin. But the more intriguing question is why.

The ETF Effect: Bitcoin’s Institutional Advantage

One major factor explaining the current mispricing is the differential impact of ETF flows. Bitcoin’s spot ETFs, launched in early 2024, transformed institutional access to the crypto market. Bitcoin ETFs have collectively attracted well over $60 billion in assets under management since their launch. These inflows provided persistent buying pressure and effectively legitimized Bitcoin as a mainstream asset.

Unlike Bitcoin, Ethereum has yet to capture the same level of institutional momentum. Despite SEC approval for spot Ethereum ETFs, inflows remain modest, roughly $15 billion to date, falling well short of the capital pouring into BTC ETFs. While ETH products showed signs of catching up earlier this year, the gap persists. For investors anticipating that ETH ETFs will eventually follow Bitcoin’s adoption curve, current prices may represent a textbook mean reversion setup.

Beyond Correlation: Has the Relationship Changed?

Still, a key counterpoint emerges: perhaps Ethereum’s discount isn’t a temporary anomaly, but a reflection of changing fundamentals. Bitcoin’s narrative has crystallized — digital gold, capped supply, macro hedge. Ethereum, however, faces a more complex identity. It’s a platform for innovation, but also one under competitive and regulatory pressure.

While Ethereum’s shift to proof-of-stake significantly reduced its energy footprint and altered token economics, Ethereum’s gas fees and scalability issues continue to challenge mainstream adoption. Layer-2 scaling solutions like Arbitrum, Optimism, and Base have helped, but the ecosystem’s fragmentation makes it harder for investors to value Ethereum as a unified asset.

Moreover, the rise of competing smart contract chains — Solana, Avalanche, and even new modular chains like Celestia — has chipped away at Ethereum’s dominance in DeFi and NFTs. According to DefiLlama data, Ethereum’s share of total value locked (TVL) across DeFi protocols has fallen from over 65% in 2021 to about 48% today. While still dominant, the erosion signals growing competition. So, could the 42% discount represent not mispricing, but repricing — a market re-evaluation of Ethereum’s future growth relative to Bitcoin’s more defined role?

The Case for Mean Reversion

Despite these structural challenges, many long-term investors argue that Ethereum’s network effect and on-chain economic activity remain unmatched. Daily active addresses, developer activity, and on-chain revenue continue to place Ethereum at the heart of Web3 infrastructure. Crucially, if inflows into the spot ETH ETFs pick up pace in the U.S, they could act as a powerful catalyst for revaluation.

If realized, such flows could close the current 42% gap quickly. Moreover, Ethereum’s deflationary tokenomics, where ETH supply can shrink during high network activity due to EIP-1559 burns, present an additional long-term tailwind. Bitcoin’s fixed supply is static; Ethereum’s is dynamic — meaning network growth directly impacts scarcity. From this perspective, the current mispricing looks less like a warning and more like an opportunity for contrarian accumulation.

The Next Possible Catalyst: Real-World Asset Tokenization

If there’s one area that could reignite Ethereum’s momentum, it’s the tokenization of real-world assets (RWAs). This concept — representing traditional assets like bonds, real estate, or equities on blockchain networks — has recently attracted growing interest from major financial institutions.

According to Boston Consulting Group, the market for tokenized assets could reach $16 trillion by 2030, and Ethereum remains the leading platform for such experiments. Companies like BlackRock, Franklin Templeton, and J.P. Morgan have all launched or piloted tokenized funds using Ethereum-compatible networks.

However, while the potential is enormous, the narrative hasn’t caught fire yet. The projects are largely institutional, slow-moving, and regulatory-heavy — far from the retail-driven energy that fueled earlier Ethereum cycles. For tokenization to become Ethereum’s next breakout story, it needs momentum, user adoption, and market excitement — all of which are still in their infancy.

Ethereum’s Position: Between Innovation and Maturity

Ethereum now stands at a crossroads between innovation and maturity. On one hand, it remains the dominant platform for decentralized computation, processing millions of daily transactions and powering the majority of DeFi protocols. On the other hand, its ecosystem is sprawling, complex, and less cohesive than Bitcoin’s narrative-driven resurgence.

Its deflationary supply mechanics (thanks to EIP-1559 and proof-of-stake) offer a solid economic foundation. Yet even deflation cannot offset the sentiment gap if investors don’t see a clear path to growth. The 42% discount, then, is not just a number. It’s a mirror reflecting Ethereum’s identity crisis, a technologically advanced network awaiting its next chapter.

A Trade, Not Yet a Triumph

Ethereum’s current valuation gap tells two stories at once. In the short term, it signals opportunity, a possible mean reversion play if capital inflows normalize and ETF inflows gather pace. But in the longer term, it reveals uncertainty, an ecosystem rich in potential but lacking a unifying catalyst to rival Bitcoin’s dominance.

For traders, ETH at a 42% discount may indeed be a bargain. For investors, it’s a reminder that narratives move markets, and Ethereum’s next one has yet to be written. Until it finds that spark, whether through tokenized assets, next-generation DeFi, or another innovation altogether, Bitcoin will likely remain the market’s gravitational center.

Originally Published on Substack.