With Bitcoin’s 30-day volatility at its lowest in years—even amid record highs—Wall Street may finally be ready to make it a core allocation.

Earlier today (June 11, 2025) – Bitcoin briefly touched $110,237 - propelled by a cooler-than-expected U.S. inflation print. The Consumer Price Index (CPI) rose just 0.1% month-over-month and 2.4% year-over-year, beating expectations of 2.5%. Core inflation also clocked in at 0.1%, raising the chance of a September rate cut. But beneath the surface of Bitcoin’s bullish breakout lies a far more consequential development than today’s price spike: a structural transformation in its volatility profile.

A Game-Changer for Bitcoin’s Risk Profile

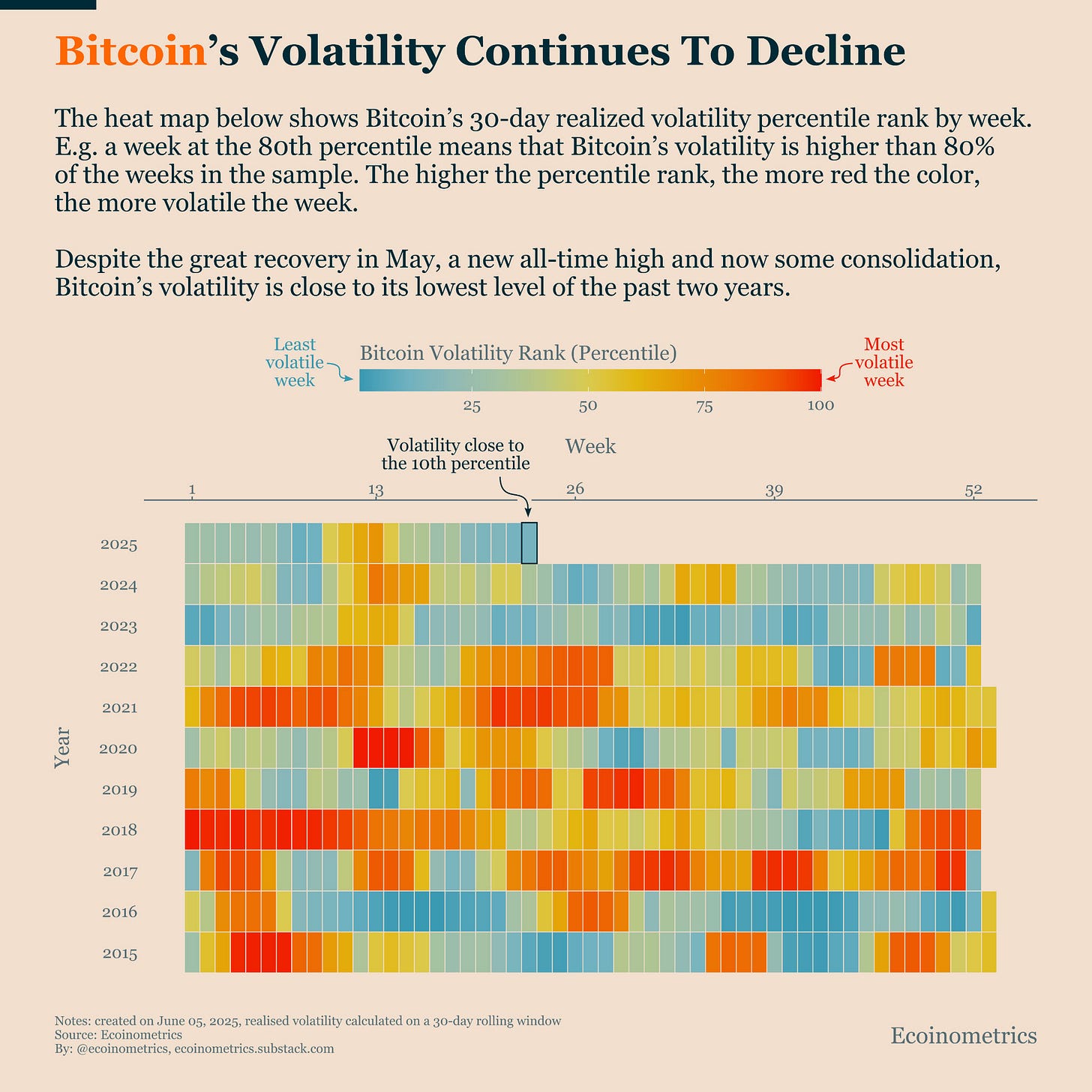

According to data compiled by Ecoinometrics (chart below), Bitcoin’s 30-day realized volatility has now dropped to the 10th percentile, meaning it is less volatile than 90% of all weeks over the last decade. This is not merely a quiet period—it’s a statistically rare calm.

What makes this moment so remarkable is that it coincides with a major bullish move, including the setting of a new all-time high (ATH) just weeks ago. Historically, Bitcoin’s price explosions came with a chaotic surge in volatility. But now, the asset is rallying while volatility compresses—a dramatic break from its past behavior. The heat map provided by Ecoinometrics visualizes this.

From 2015 through 2021, volatility spikes (in red and orange) often accompanied bull runs. These hot zones litter the years of BTC's adolescence—2017’s mania, 2020’s pandemic-fueled breakout, and even 2021’s institution-led rally. But the 2024–2025 period tells a different story: more weeks are shaded blue or green, signaling calm, even as Bitcoin breached new highs.

Why This Matters for Institutional Allocators?

For professional asset allocators, volatility isn’t just noise—it’s the language of risk. Every fund, from pension giants to endowments, operates within a framework that quantifies how much volatility a portfolio can tolerate. Assets that routinely blow through risk models—like Bitcoin did in the past—are often relegated to small satellite positions or left out entirely. But this recent shift makes Bitcoin a very different beast.

If an asset offers high returns without high volatility, it becomes easier to fit into traditional portfolio optimization models like the Sharpe ratio, value-at-risk (VaR), and volatility targeting strategies. This makes it appealing to institutions that may have previously sat on the sidelines due to Bitcoin’s erratic behavior. In short, Bitcoin is evolving from a speculative rocket ship into a macro-correlated asset with an asymmetric upside. For allocators managing volatility budgets, this is a breakthrough.

What’s Driving the Drop in Volatility?

Several structural changes may be contributing to this newfound calm:

-

ETF Flows: The approval and adoption of Bitcoin ETFs in major markets have provided a smoother, more regulated entry point for investors. Daily volumes are increasingly dominated by professional trading desks rather than retail-driven swings.

-

Maturing Market Infrastructure: The presence of robust futures markets, options, custodial services, and cross-exchange liquidity has reduced dislocations and price shocks.

-

Global Macro Narrative: Bitcoin is increasingly seen not as a tech curiosity but as a macro hedge. As traditional assets become more volatile in a tightening or stagflationary regime, Bitcoin is starting to behave like digital gold—reacting more predictably to macroeconomic data.

-

Longer Holding Periods: On-chain data shows that more Bitcoin is held in cold storage by long-term holders (whales). This limits panic selling and short-term noise, resulting in more stable price behavior.

Volatility Compression During a Bull Market?

Even during prior bull markets—such as those in 2017 and 2020—Bitcoin’s gains came amid extreme swings. At those times, it wasn’t uncommon for the asset to rise 10–20% in a day, only to crash just as quickly. That made gains emotionally and strategically harder to hold.

But today, despite rising more than 40% since January and hitting a fresh ATH, volatility remains compressed. As the heat map shows, recent weeks fall into the green-to-blue spectrum—ranked below the 25th percentile for volatility. For comparison, the 2021 bull run shows a sea of orange and red, with many weeks above the 75th percentile in realized volatility. This is not just a statistical fluke—it’s a regime shift.

What Comes Next?

If Bitcoin can maintain this balance—strong returns with tempered volatility—it could catalyze the next wave of institutional adoption. Large-scale investors who previously viewed Bitcoin as too volatile now have fewer excuses. Moreover, as Bitcoin begins to behave more like a macro asset class, it could earn a role not just as an alternative, but as a core portfolio component, akin to gold or even equities.

There are, of course, caveats. Bitcoin’s low volatility may not last forever. Shocks—whether regulatory, technological, or geopolitical—could bring back the chaos. But even a moderate increase in volatility from here would still place it within a more palatable range for many institutional models.

A Structural Maturity Moment

Today’s CPI data may have fueled the immediate price surge, but the real story is deeper: Bitcoin has changed. No longer the volatile outsider, it is transforming into a mature asset capable of earning a seat at the institutional table. That shift—visible now in the data—is not only a milestone for crypto but a warning shot to traditional investors who continue to underestimate Bitcoin’s staying power. As Bitcoin continues to climb with muted volatility, it doesn’t just make headlines—it makes history.

Originally Published on Substack.