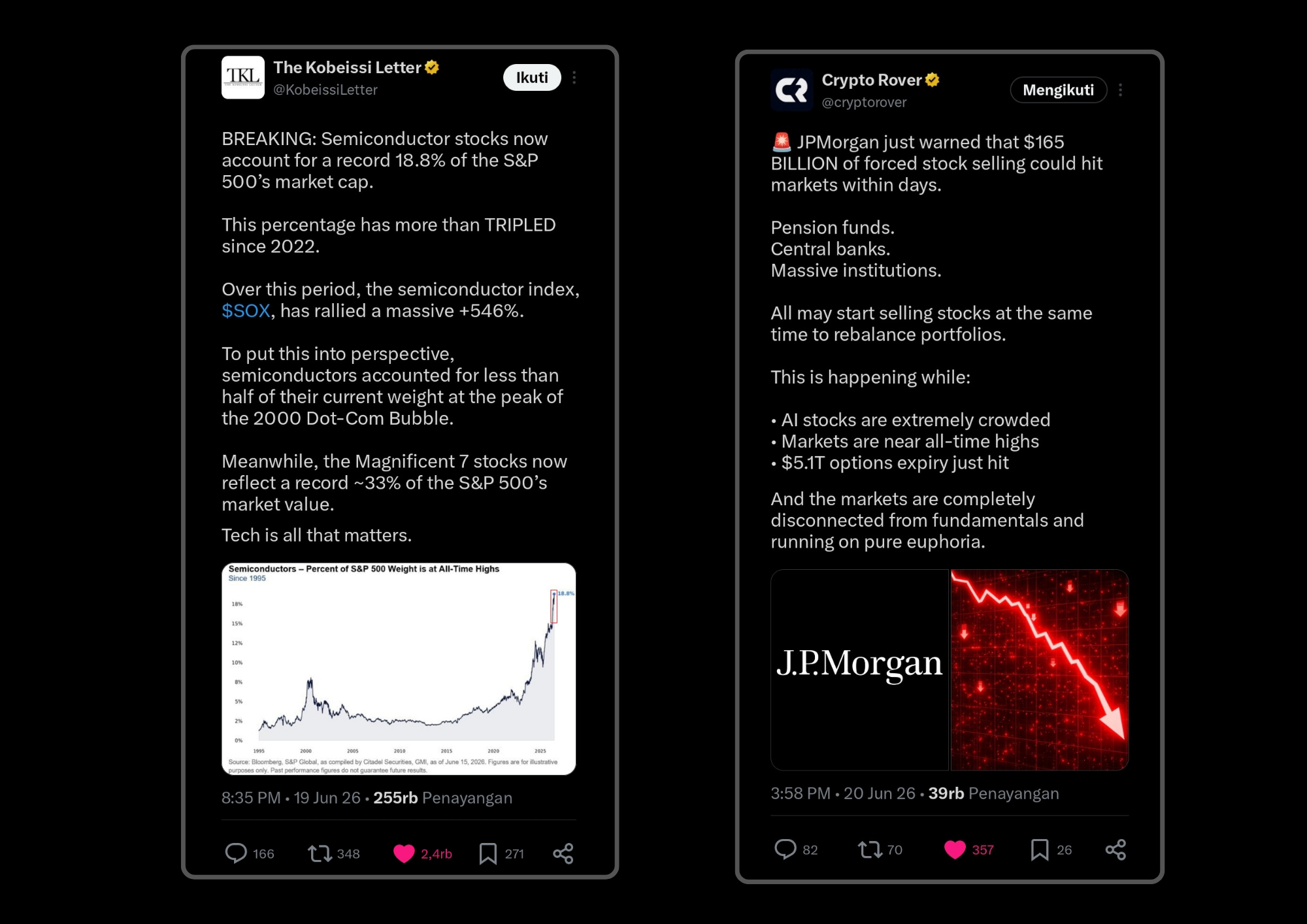

The global financial market is hitting a critical turning point as the S&P 500 index reaches an unprecedented milestone of $7500. This massive rally is completely tied to the historic rise of semiconductor companies, which now represent a record breaking 18.8% of the entire S&P 500 market cap. To put this growth into perspective, this specific sector weight has more than tripled since 2022, fueled by the semiconductor index, SOX, which gained an explosive 546% over the same period. Analysts note that this extreme concentration heavily outpaces the data seen during the absolute peak of the dot com bubble back in 2000.

However, this aggressive upward move has triggered a major warning from banking giant JPMorgan regarding a potential $165 billion forced stock liquidation. Large institutions, central banks, and major pension funds will likely be forced to sell off equities to rebalance their portfolios after tech gains made their allocations disproportionately large. This warning lands right alongside a massive $5.1 trillion options expiry event, creating a highly volatile backdrop for a market that many believe is running on pure euphoria and disconnected from baseline economic indicators.

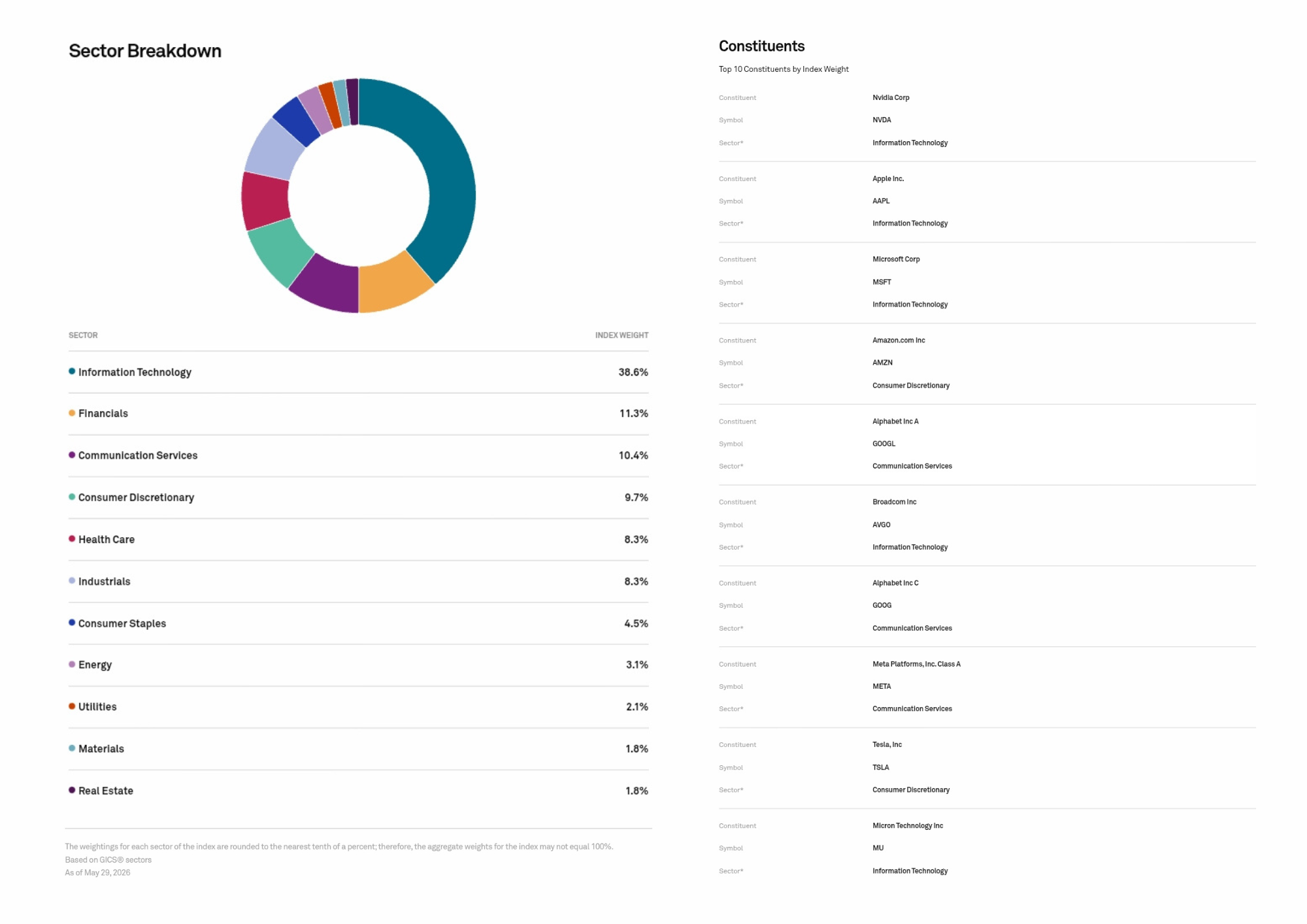

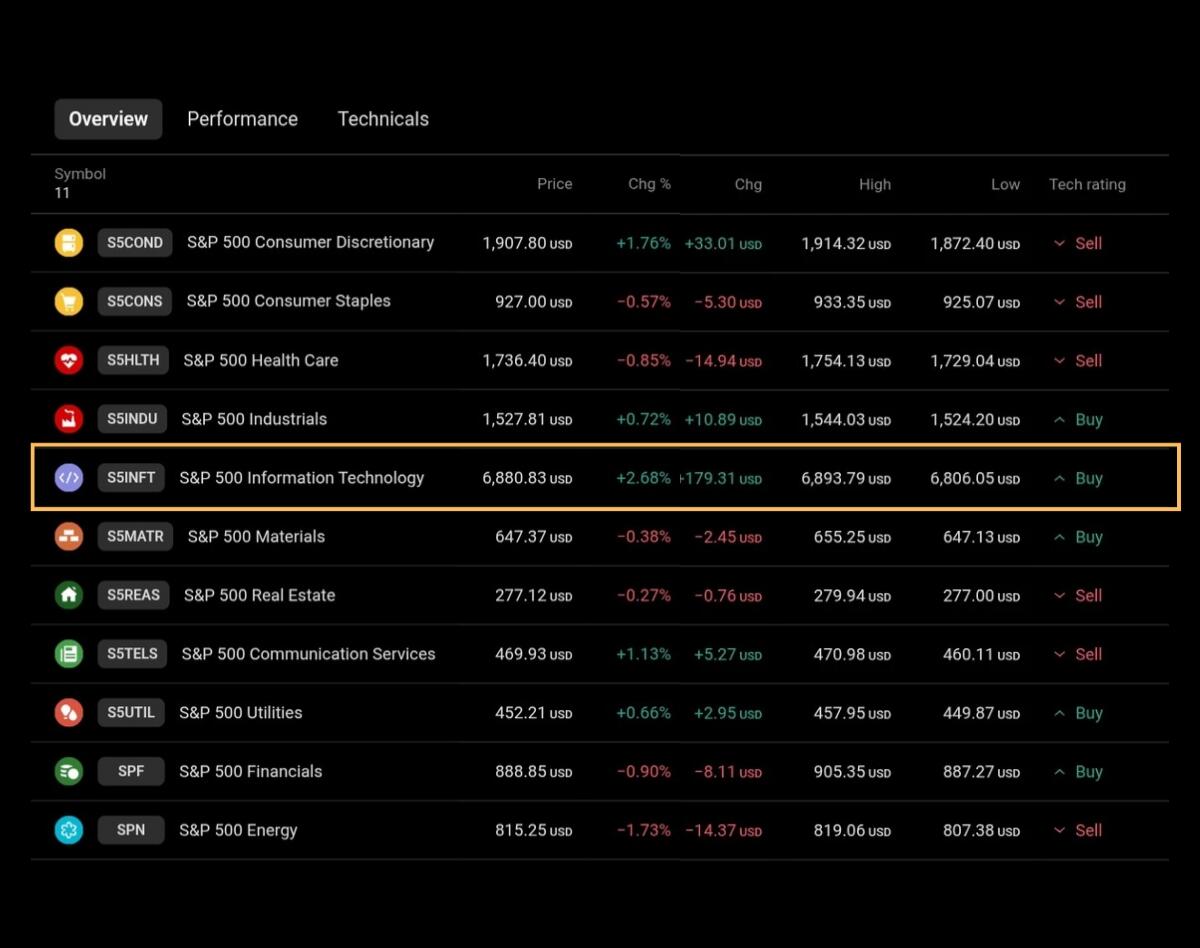

A closer look at current sector weights reveals that Information Technology completely dominates the broader market, locking in a massive 38.6% share of the S&P 500 index. Within this sector, semiconductor powerhouse NVIDIA Corporation commands the highest individual index weight, closely followed by tech heavyweights Apple, Microsoft, and Broadcom. This internal market imbalance is visible in recent daily sessions, where the tech sector alone booked a sharp 2.68% jump while defensive areas like energy and financials lagged behind in the red.

Adding to the tension, recent capital flow reports indicate that institutional money entering artificial intelligence equity products has flattened out over the past two weeks. Worried about an overextended market, institutional desks are quietly shift adjusting capital into less volatile asset classes. This underlying shift shows up on the technical charts, where the semiconductor index, SOX, displays a vertical, highly parabolic curve that leaves it exposed to aggressive profit taking. While the weekly S&P 500 framework remains above $7500, trading this far above historical moving averages without an occasional healthy pullback serves as a clear warning sign for active traders.

My Opinion

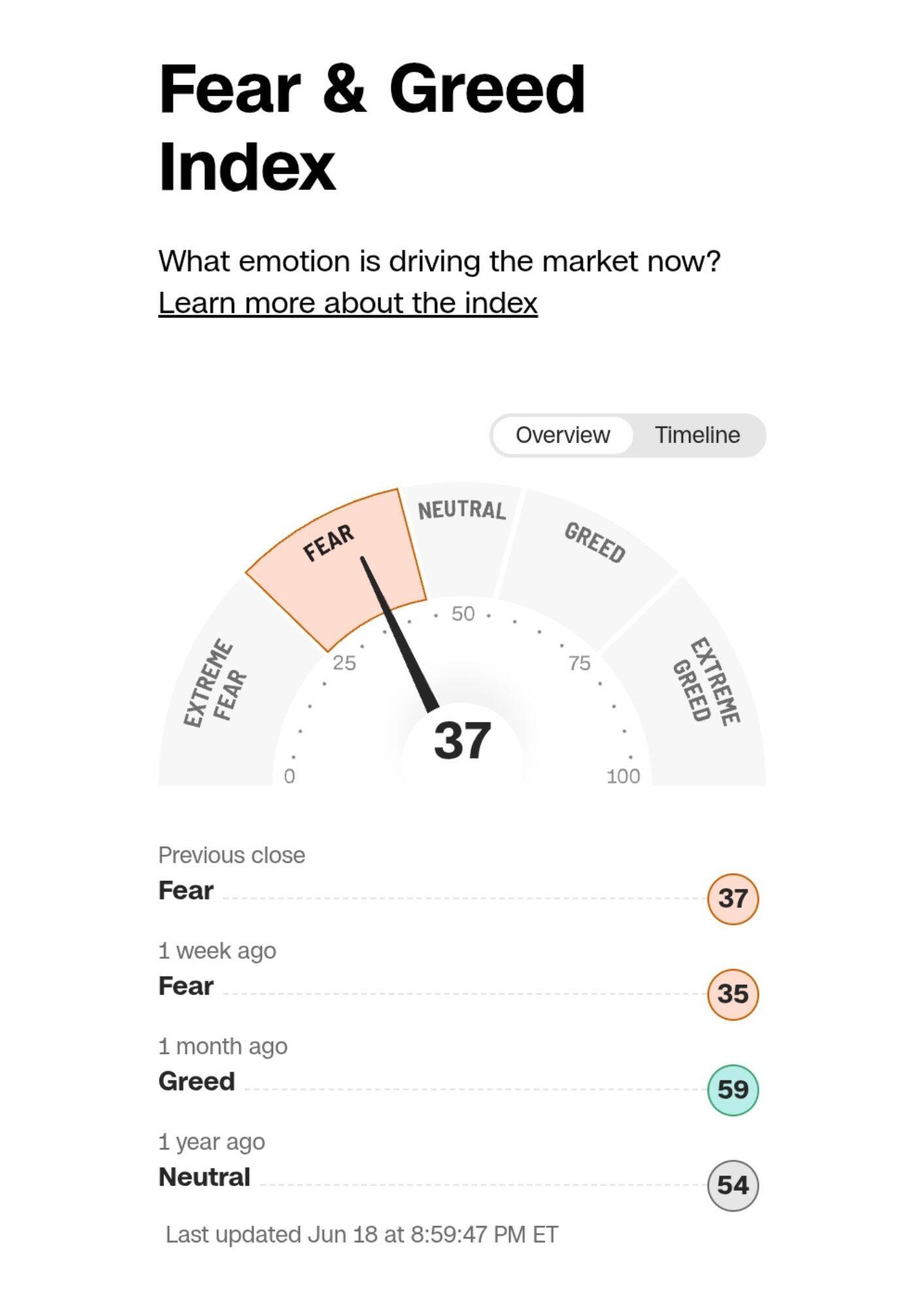

Looking at the positive factors, this climb to $7500 demonstrates that the ongoing AI expansion is generating actual corporate earnings, separating it from the purely speculative tech bubble of 2000. Furthermore, the fear and Greed index is currently sitting at 37, indicating a state of fear among market participants. This general sense of caution among retail traders is actually a good sign, as it acts as a stabilizing force that prevents the market from entering a state of total, uncontrolled irrational exuberance.

On the negative side, having 38.6% of the entire index tied directly to a single sector introduces severe systemic vulnerability. The S&P 500 has effectively stopped reflecting the broader global economy, acting instead as a proxy for just a handful of megacap tech firms. If JPMorgan’s projected $165 billion rebalancing materialized, any downside movement in top holdings like NVIDIA, Apple, or Microsoft would instantly pull the rest of the market down with them. Combining that structural weight with the trillons in options expiry could easily trigger panic selling, bringing prices down to align with historical fundamentals.

Click here to read my authentic and original analysis

Source