Summary

- Some thoughts on infrastructure: zk-rollups, oracles, and L2 development. How are those things developing, and what does it mean for the industry?

- DeFi — will it rise or lose its ground in 2023? It seems the DeFi field is growing and strengthening by increasing investors' demand.

- Dramatic fall of GameFI, NFT, and SocialFi. NFT hype cooled down, gaming tokens showed poor performance, and decentralized social media doesn’t look like a long-term trend either.

- Strong regulation is coming. Does the market need needs wrangle? If so, what does it mean for investors and those involved?

Intro

The current year, 2023, will likely be challenging for all markets. Although, recent events and current crypto trends show us that the DeFi sector might be a flourishing one. It is also worth noting that DeFi won’t lose its position in the upcoming years as more investors move to decentralized exchanges and other asset management platforms. Moreover, new blockchain technologies are emerging to improve infrastructure’s interoperability.

It has been argued that bear markets are usually used as a respite to build new infrastructure. Still, there is a lack of demand in this cycle, which generally pushes technology development. Let's try to figure out how things are. So 2023 will not be a bull market year but rather a year of institutional experimentation and the introduction of new technologies for infrastructure, including the use of private blockchains, information about the development of which is usually not publicly available.

Infrastructure

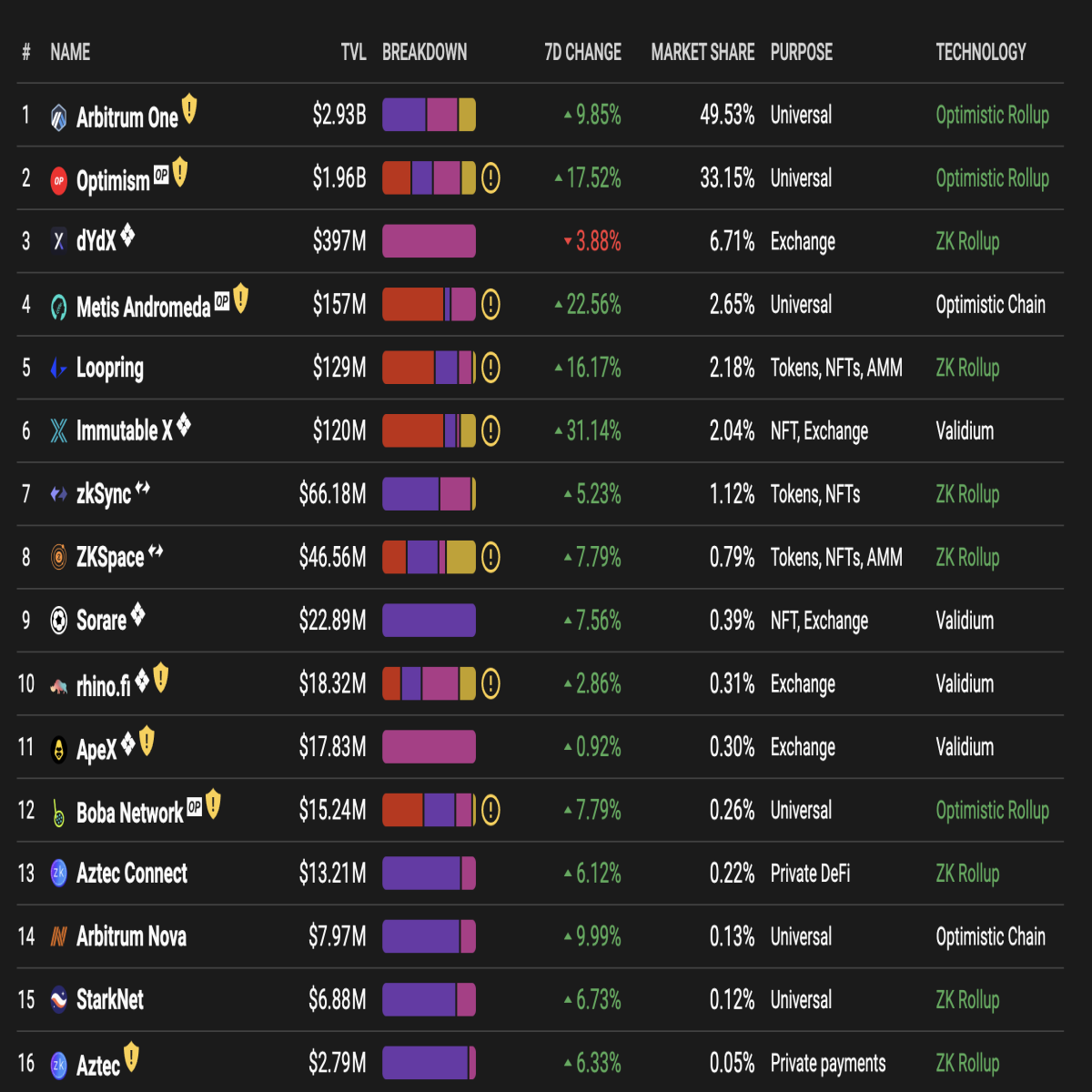

If we focus on recent announcements and investments of funds, we can see that there are more projects related to infrastructure around zk-rollups. New blockchain technologies oriented to support their infrastructure are appearing. These include, for example, projects such as Ulvetanna and Nil, which aim to facilitate the generation of zk-roles and increase EVM interoperability. Hyper Oracle, an oracle indexer that connects zk protocols to Ethereum via cross-chain communication via decentralized RPC. The top blockchains of the past cycle are not left out either. There is a noticeable increase in attention to roll-up technology from current L1 blockchains: Polygon is developing its zkEVM and optimistic rollup solutions to implement and improve scalability; there are developments to launch Solana virtual machine as modular blockchains and rollups; at Avalanche, zk-based solutions to improve speed and scalability are also about to turn up on subnets. In the context of L2 infrastructure development, it is important to develop bridges and conditions for liquidity providers for optimistic rollups, which have a delay of 1 week to transfer to L1 due to the particular logic of working with Fraud Proofs. This requires either protocol that provides liquidity or solutions similar to Aave's GHO that allow access to blocked liquidity through synthetic assets or lending. This is a highly relevant issue, given that zk rollups have difficulties with EVM compatibility and running applications on zkEVM is more difficult than almost natively migrating Dapps from L1 ETH to optimistic L2. And also, the main TVL in DeFi L2 generates optimistic rollups, which outperform even most L1 rollups:

Figure 1: L2 TVL. Source: l2beat.com

Figure 1: L2 TVL. Source: l2beat.com

Figure 2: All chains TVL. Source: DeFiLama

Figure 2: All chains TVL. Source: DeFiLama

According to an analyst Hayden Booms, it is worth considering that in the run-up to the Shanghai update for Ethereum, which will allow users to unlock funds, there could be pressure on the price of ETH. Because of this, some of the liquidity may go to other protocols and ecosystems - such as L2 solutions, which may start launching their tokens in 2023 (Optimism, ZkSync, Starknet). And the leading L2 roll-up protocol, Arbitrum, may strengthen its position after introducing support for non-EVM smart contracts. But it's worth keeping in mind that L2 uses ETH rather than native protocol tokens to settle transactions, which may have a positive impact on ETH due to network effects and the increase in ETH burnt in transactions.

Layer 2

It’s worth mentioning that Layer 2 rollups are still running using centralized sequencers, and this can carry potential risks for exploits. These risks are especially relevant for Optimistic rollups because of their latency period in the face of the emergence of liquidity providers borrowing from L2 to L1 transactions.

Appchain idea

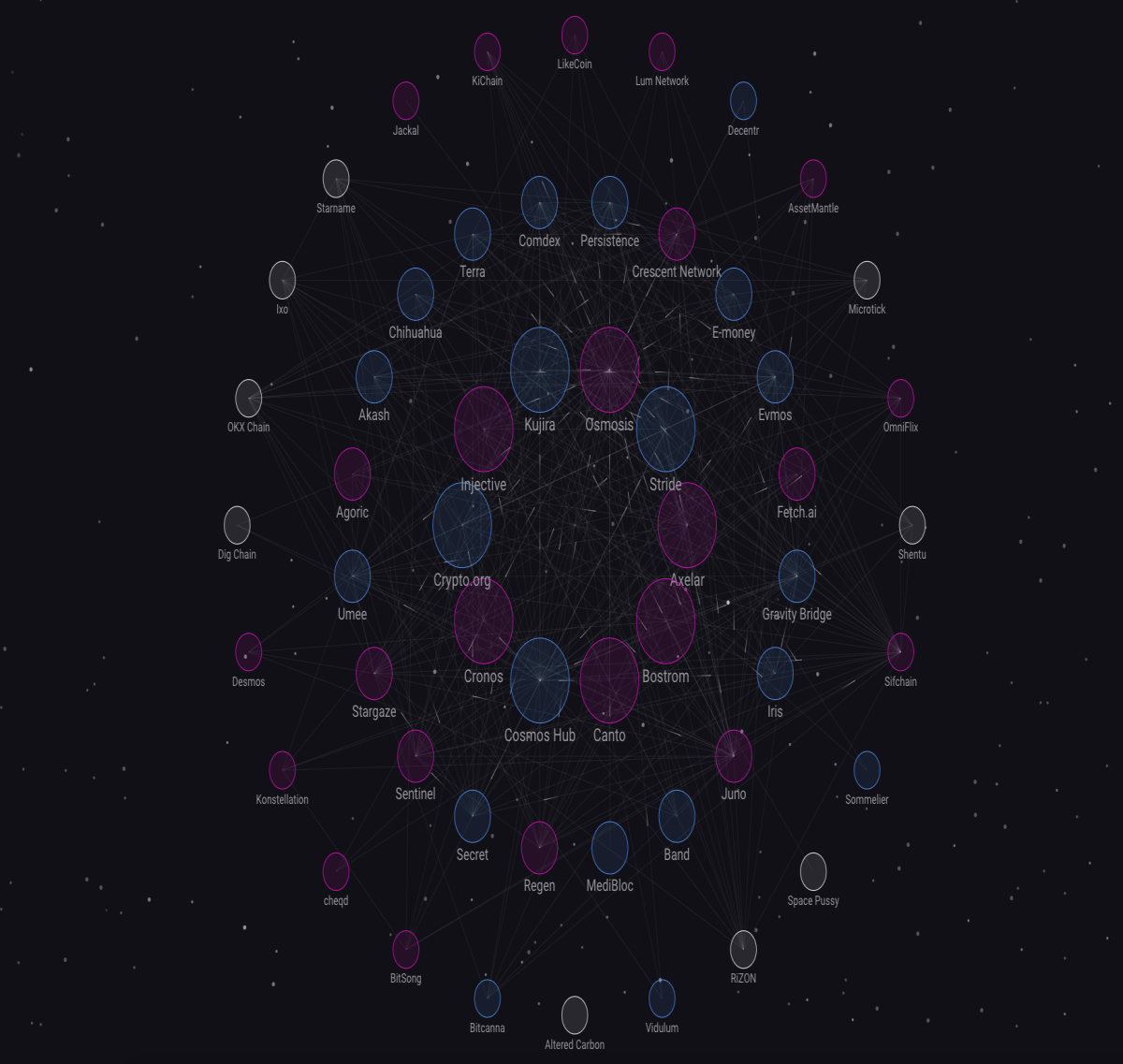

One of the most relevant trends in blockchain technology that we can’t neglect is the development of the Appchain idea, which is implemented in the Cosmos ecosystem, gaining momentum in some L2 solutions for Ethereum. IBC technology based on Cosmos is very actively developing, allowing a connection of Appchains and creating opportunities for cross-chain interoperability, including in the form of bridges.

This can increase the reliability and credibility of bridges, as third-party bridges are always less reliable than native ones and prone to exploits. It would also unify the liquidity of protocols such as Uniswap, Aave, Synthetix, and Compound, where liquidity is currently scattered across networks. Another factor that could contribute to the explosive development of Cosmos is the transition of dYdX from StarkEx to Cosmos, as well as the expected launch of the Circle USDC native stablecoin in Cosmos.

ZK & Cosmos

Moreover, the joint development of ZK and Cosmos technologies leads to the ability to connect IBC to Ethereum via zk-Proofs, which reduces the cost of bridges and allows IBC to connect to any blockchain without built-in IBC support. This could lead to the Cosmos ecosystem becoming a single hub for all networks.

Figure 3: Cosmos IBC ecosystem. Source: www.mapofzones.com

Figure 3: Cosmos IBC ecosystem. Source: www.mapofzones.com

Other projects such as Oasys, Starknet, Immutable, Avalanche, and others are also popularizing the idea of separate blockchains for separate applications in the form of L2 or L3. But they don't offer as much native interoperability with other blockchains as IBC does. Even Avalanche, after launching AWM (Avalanche Wrap Messaging) technology, similar to IBC Cosmos, includes interoperability without bridges only between its subnets. With other blockchain networks, the connection is still via a bridge.

Download our all-in-one app to be far ahead in the crypto space. Set it up right from AppStore and Google Play for free.

DeFi

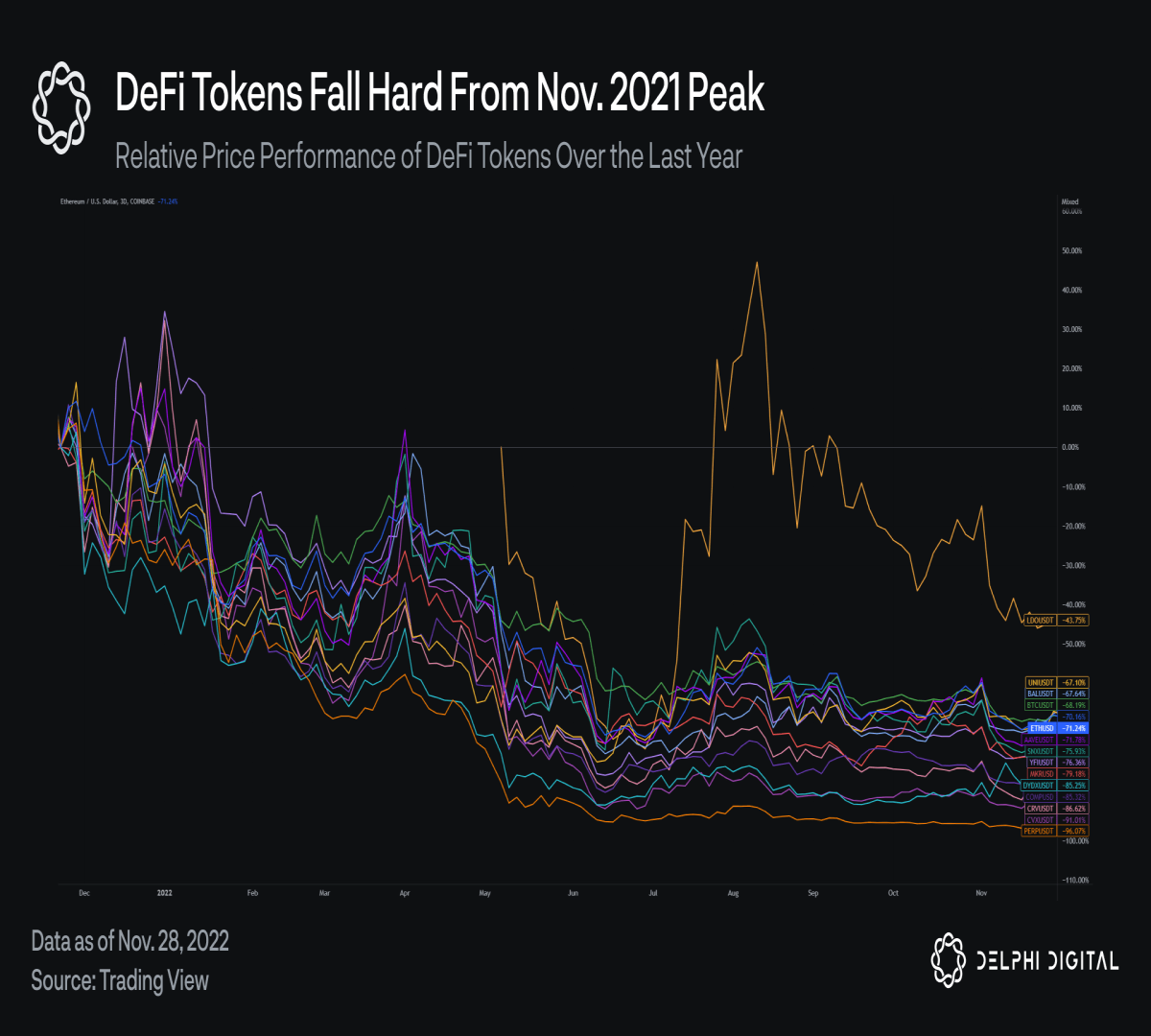

Although the DeFi boom has passed in 2020, after the FTX story and cryptocurrency funds, there has been more interest in the direction of decentralized finance. This is because, in this usage scenario, the user usually retains complete control over their funds. The dynamics of DeFi tokens in Ethereum since November 2021 do not look good:

Figure 4: DeFi tokens value. Source: Delphi Digital, Trading View

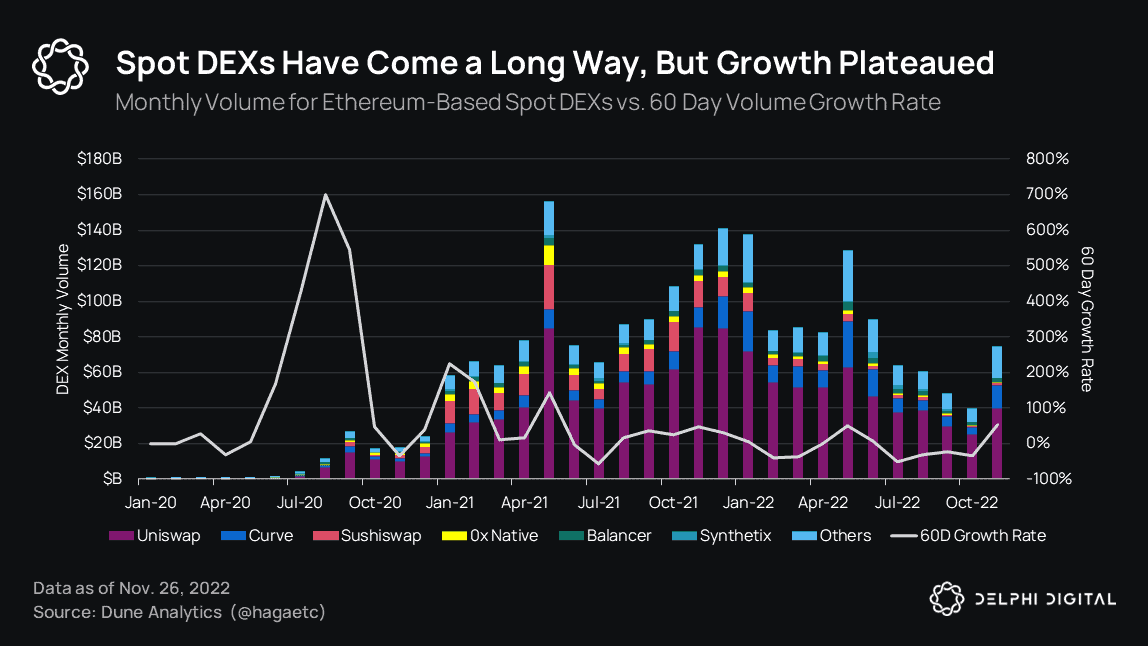

In spite of that, there are full-scale launches of L2 solutions ahead, which may stimulate a new round of DeFi development due to lower commissions, higher speed, and new tools. It is also worth considering that improved user experience and UX will bridge the gap between CEX and DEX operations. The development of new technologies with higher transaction processing speed allows the implementation of more advanced models for dealing with liquidity, which may come to replace AMM. For example, they include centralized order books (CLOBs), which reduce Impermanent Loss risks for liquidity providers in addition to improved UX. There are also combined solutions that combine hybrids of CLOBs and AMMs. Traders can use market or limit orders to access essential shared liquidity between all pools. Such solutions include Duality, which is set to launch in Q1 2023. That’s quite noticeable that despite the TVL’s fall more than 75% from its peak, DeFi still accounts for most of the capital in products on blockchain networks, with DEXs generating the bulk of the volume.

Figure 5: ETH spot DEXes monthly volume. Source: Delphi Digital, Trading View

Figure 5: ETH spot DEXes monthly volume. Source: Delphi Digital, Trading View

While interest in leveraged derivatives in DeFi is waning due to falling markets, the collapse of institutional lenders such as Celsius, BlockFi, Hodlnaut, and Babel Finance is increasing interest in DeFi lending. This could allow for more transparent processes and loan portfolios and give market makers access to leverage credit based on data from on-chain balance sheets without bureaucratic processes (Maple). Another trend to note in DeFi is the development of aggregators. Right now, many protocols in different networks with their sites, disparate liquidity, UX, and UI create a high entry threshold for users. Several layers have already formed in DeFi, which are responsible for aggregating and providing liquidity and building infrastructure. Or for example, Matcha, 1inch, and ParaSwap get quotes from different DEXs to find users the best execution price.

The next trend, which has long been outlined but has only started to develop in the last 1-2 years actively and is setting the direction for 2023 with project launches - cross-chain interoperability. For full interoperability, you need more than just bridges. In addition to solutions to improve UX, aggregators or cross-chain protocols continue with liquidity providers and lending protocols that allow assets in one network to be borrowed against assets in another network, which will also improve capital efficiency. These projects include Mars Protocol, Prime Protocol, Rage Trade, and Composable Finance.

These are all more like backend solutions. However, there are increasing requests for next-level formations - custom formations. These include Odos, Zapper, Zerion, and DeBank. They provide users with a single interface to interact with a large number of protocols and can even roam across multiple liquidity floats to reduce transaction costs.

Separately, there are derivative instruments, of which there is a huge number in 20222. They potentially open up a huge field for experimentation: from hedging call and put options to providing liquidity in narrow cases, such as transferring funds from optimistic rollups to L1. This could include synthetic assets, which allow for infinite liquidity based on token burning/minting.

There are also new ways of using liquidity that is still in development and are aimed at using DeFi as a base level. For example, Berachain (which also belongs to the Cosmos ecosystem) plans to launch a PoL-based consensus, Proof of Liquidity, in which a share of validators are simultaneously used to provide liquidity in the DEX and lending markets, as well as to maintain their stablecoin peg. This design makes DeFi an integral part of the base layer, which is not the case in the existing L1 paradigm.

These are all more like backend solutions. However, when there are increasing requests for next-level formations - custom formations. These include Odos, Zapper, Zerion, and DeBank. They provide users with a single interface to interact with many protocols and can even roam across multiple liquidity floats to reduce transaction costs. Separately, there are derivative instruments, of which there is a vast number in 2022. They open up a field for experimentation: from hedging calls and put options to providing liquidity in narrow cases, such as transferring funds from optimistic rollups to L1. This could include synthetic assets, which allow infinite liquidity based on token burning/minting.

There are also new ways of using liquidity that are still in development and are aimed at using DeFi as a base level. For example, Berachain (which also belongs to the Cosmos ecosystem) plans to launch a PoL-based consensus, Proof of Liquidity, in which a share of validators are simultaneously used to provide liquidity in the DEX and lending markets, as well as to maintain their stablecoin peg. This design makes DeFi an integral part of the base layer, which is not the case in the existing L1 paradigm.

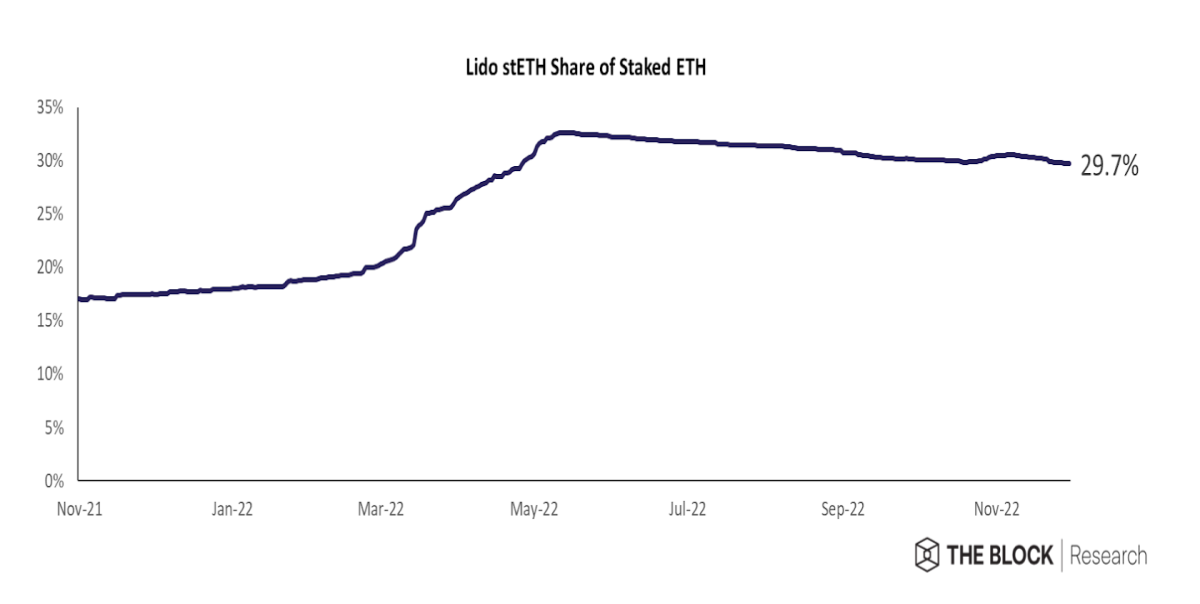

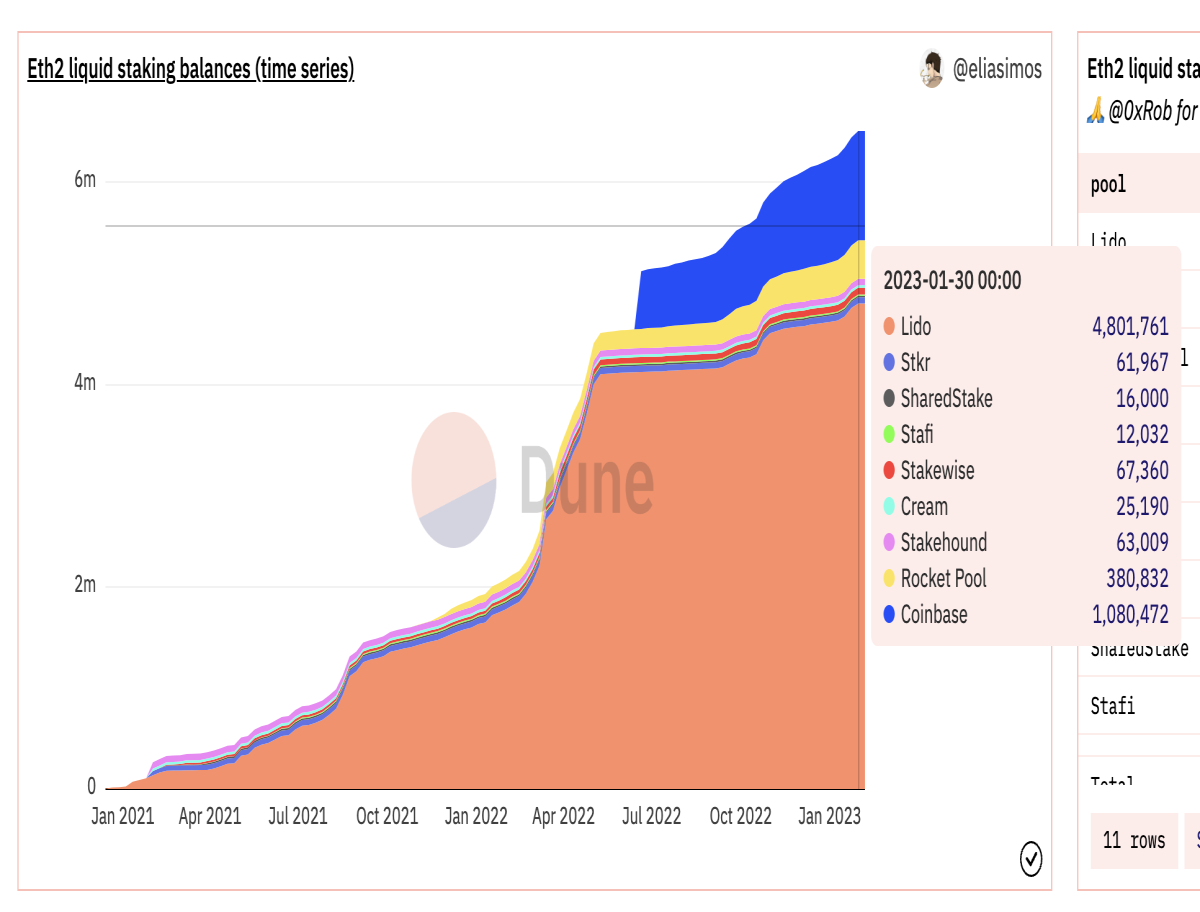

In the context of increased activity in Ethereum's L2 and Shanghai update, it is also worth considering that most of ETH are liquidated directly, without the involvement of synthetic liquidity. In particular, despite the large percentage of staked ETH in Lido (29.7%), there are prerequisites for further growth in liquidity staking. According to Dune Analytics, 42.97% of ETH was deposited through liquidity pools. The diagram from Dune shows an upward trend in the volume of stacking.

It is more profitable for stackers to get synthetic liquidity and use it in DeFi, rather than just staking ETH, thus reducing capital efficiency. A fight could unfold between liquidity-staking protocols such as Lido, corporative Liquid Collective protocol, Coinbase cbETH, Rocket pool, and others.

Figure 6: Lido stETH share of staked ETH. Source: The Block Research

Figure 6: Lido stETH share of staked ETH. Source: The Block Research

Figure 7: ETH2 Liquid Staking Balances. Source: Dune Analytics

Figure 7: ETH2 Liquid Staking Balances. Source: Dune Analytics

We can also observe a high interest in DeFi from institutional players. Some of the examples:

- Wintermute is launching a derivatives exchange that outsources the storage of customer funds to trusted custodians.

- Ondo has launched a tokenized fund that allows Stablecoin holders to invest in U.S. bonds and treasuries and receive tokenized interest from the funds, which can be transferred online, including through approved smart contracts.

- BlockTower has partnered with MakerDAO to create an institutional loan fund that works with real assets (RWAs). Maker will deploy four vaults to fund real asset investments (RWAs) created by BlockTower and released online through Centrifuge.

NFT, GameFi, SocialFi

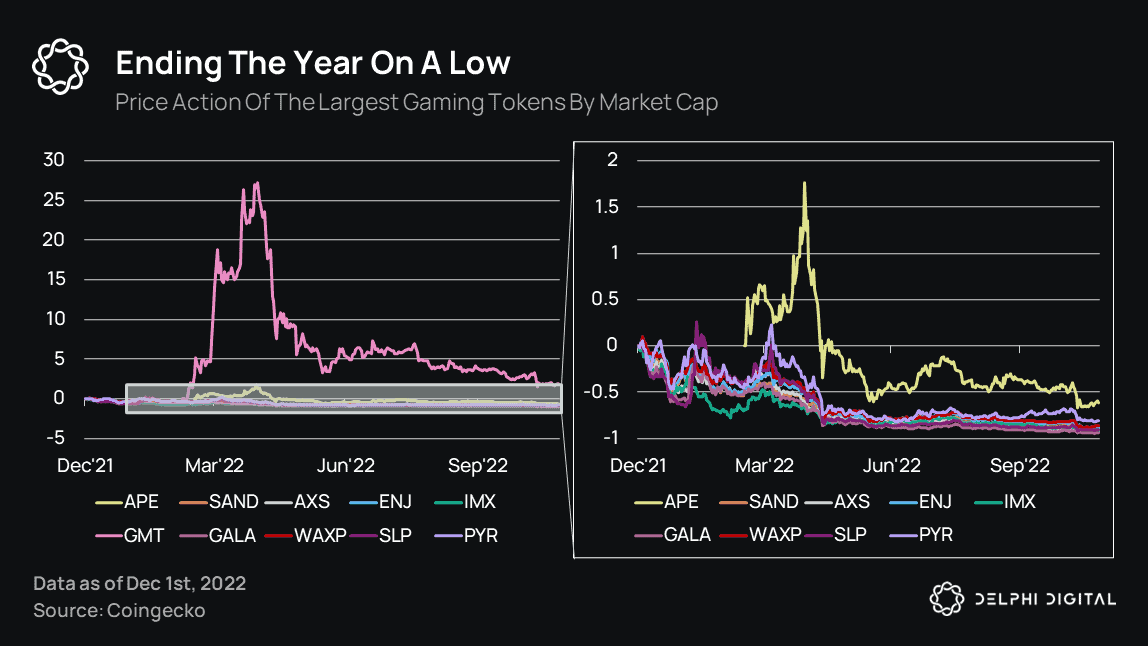

As for the NFT industry, judging by recent trends, it is losing ground. But nevertheless, many new projects related to GameFi and SocialFi are emerging. These include projects like Lens, Bluesky Social, and Farcaster. Game projects are coming to the point where gameplay, lore, and gameplay are more important than the blockchain component, despite the fact that in 2022 more than 50% of the deals attracting investment were related to games. At this point, these investments are at a disadvantage, as game project tokens tend to have poor performance due to the weak applicability of in-game tokens and poor economic incentives, which put more pressure on the price.

Another thing to consider is the fact that the Web3 gaming industry has been hit hard since the collapse of Terra and FTX. Since early 2022, the top 10 blockchain gaming projects by market capitalization have fallen to 95%.

Figure 8: Largest gaming tokens value. Source: Delphi Digital, Trading View

Figure 8: Largest gaming tokens value. Source: Delphi Digital, Trading View

In addition, there are no cases for easy work with NFT for users accustomed to Web2. Therefore, in 2023, tools and products will be actively developed to facilitate the adoption, a trend set back in 2022. Therefore, it is unlikely to expect significant breakthroughs at the intersection of the crypto- and game industries soon. Especially since, at the moment, there are still many limitations in user experience, UX, and UI for web2 users. And for a breakthrough for games in Web3, first, you need to build a convenient infrastructure, not only for the Web3 component but also the hardware, which will not only ensure the reliability and responsiveness of the system but can offer good capacity for data streaming in the case of VR and AR content. And so far, the current stage of development deals with the development of blockchain infrastructure and Web3 rather than on the user experience side, which will have to launch a mass adoption.

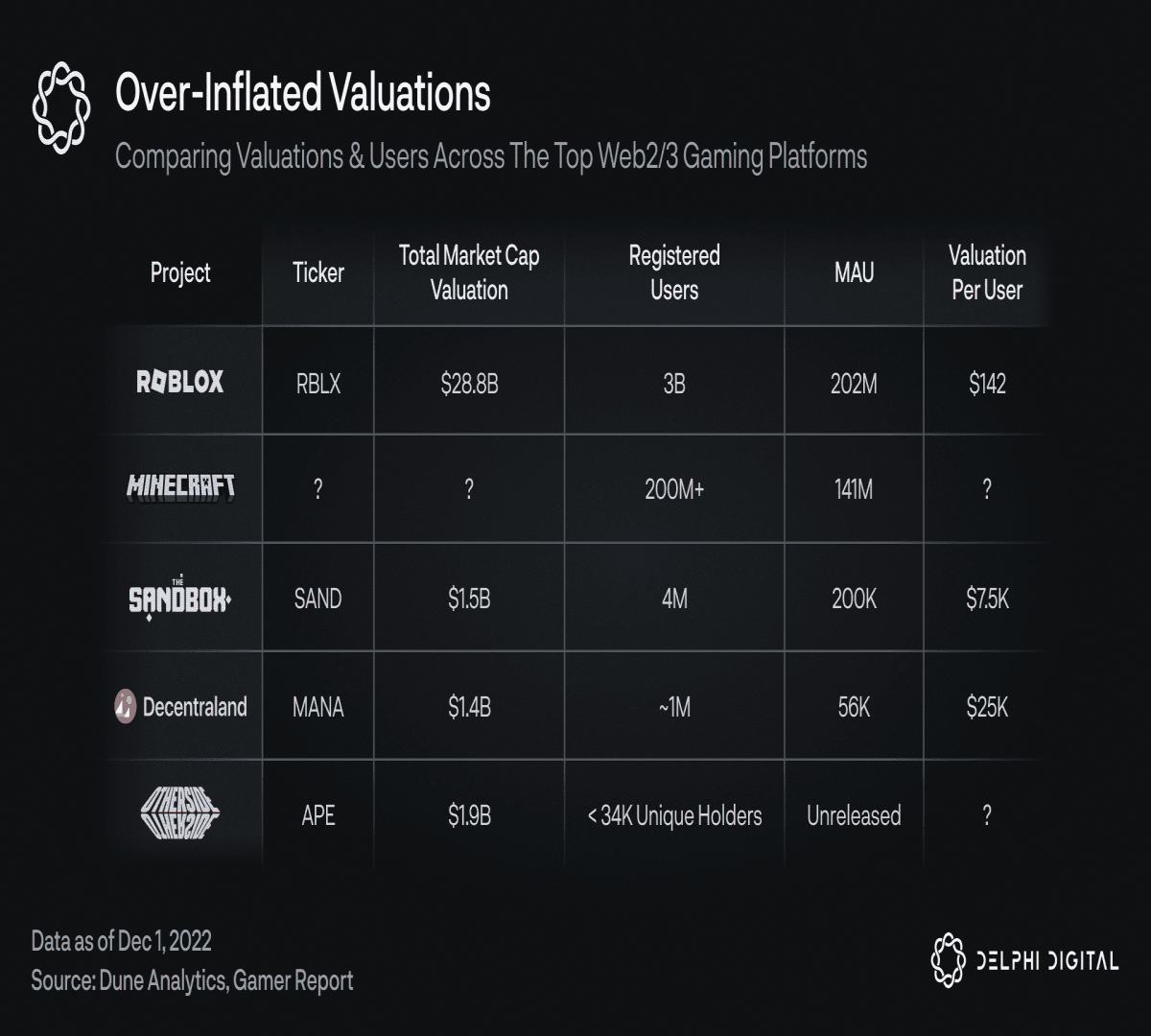

If we look at the side of meta-universes, such as Decentraland, Sandbox, and Otherside, we can assume that significant growth in 2023 in this direction is not expected. In this sector, development occurs only when there is a lot of flashy money, attracting the attention of celebrities, and experiments are started. For example, as it was with land, around which in 2021 and 2022, there was a considerable stir and even began to emerge a full-fledged client infrastructure: studios that create custom objects, buildings, spaces, and quests (Polygonal Mind, Voxel Architect, Ogar, Allota Money and many others), consulting agencies (Metaverse Advisors), real estate agencies that invest in virtual land (Metaverse Group, 13th Floor Ventures). At this point, activity has been severely deflated due to a drop in velocity and investor interest. But even in this case, judging by the evaluation of such projects relative to the number of users compared to Web2 (Roblox, Minecraft), users are very overvalued, so we should only expect breakthroughs in this direction in 2023.

Figure 9: Valuations and users of the top Web2/3 gaming platforms. Source: Delphi Digital, Dune Analytics

Figure 9: Valuations and users of the top Web2/3 gaming platforms. Source: Delphi Digital, Dune Analytics

It can be noted that the trend of user identification, including with Souldbound tokens, is now more active. Hidden here is another point that is not very obvious for users with wallets, which can allow users to work with Dapps through smart contracts, reducing the number of actions in the applications. This is possible through account abstraction and would bring the user experience closer to Web2. Currently, account abstractions support protocols that have wallet addresses as smart contracts: zkSync, Starkware, and modular Fuel.

Another recent trend that began in late 2022 is AI-themed, on which the tokens of blockchain projects related to AI have grown strongly in one way or another. This happened on the backdrop of the rapid development and impressive growth of AI neural network users, such as ChatGPT, Midjourney, Jasper, and a host of others.

But this should hardly be considered a long-term trend applicable to the crypto industry. This is because cryptocurrency and blockchain technologies are not used in the solutions mentioned above, and they are Web2 products with payment methods used for Web2. Blockchain technologies are still too slow for a huge user base of 500mln users with a huge number of requests. AI technologies in blockchain so far are used as a rule for analyzing on-chain data, improving the work with data in blockchains, and improving the networks themselves. And cryptocurrency for payment is also so far weakly applicable because for Web2 users, it is easier to pay directly from a plastic card than to increase the number of payment steps through a payment gateway and one of the many blockchain wallets in many different networks.

External Incentives and Regulation

If you pay attention to what's happening in the world around us, you'll notice some interesting facts and trends.

For example, oil and gas companies like Exxon Mobile are converting natural gas, which would otherwise be burned, into electricity to run bitcoin mining right on-site. This further reinforces the idea that bitcoin is backed by energy itself, giving it more perceived value and creating a long-term trend for the crypto industry.

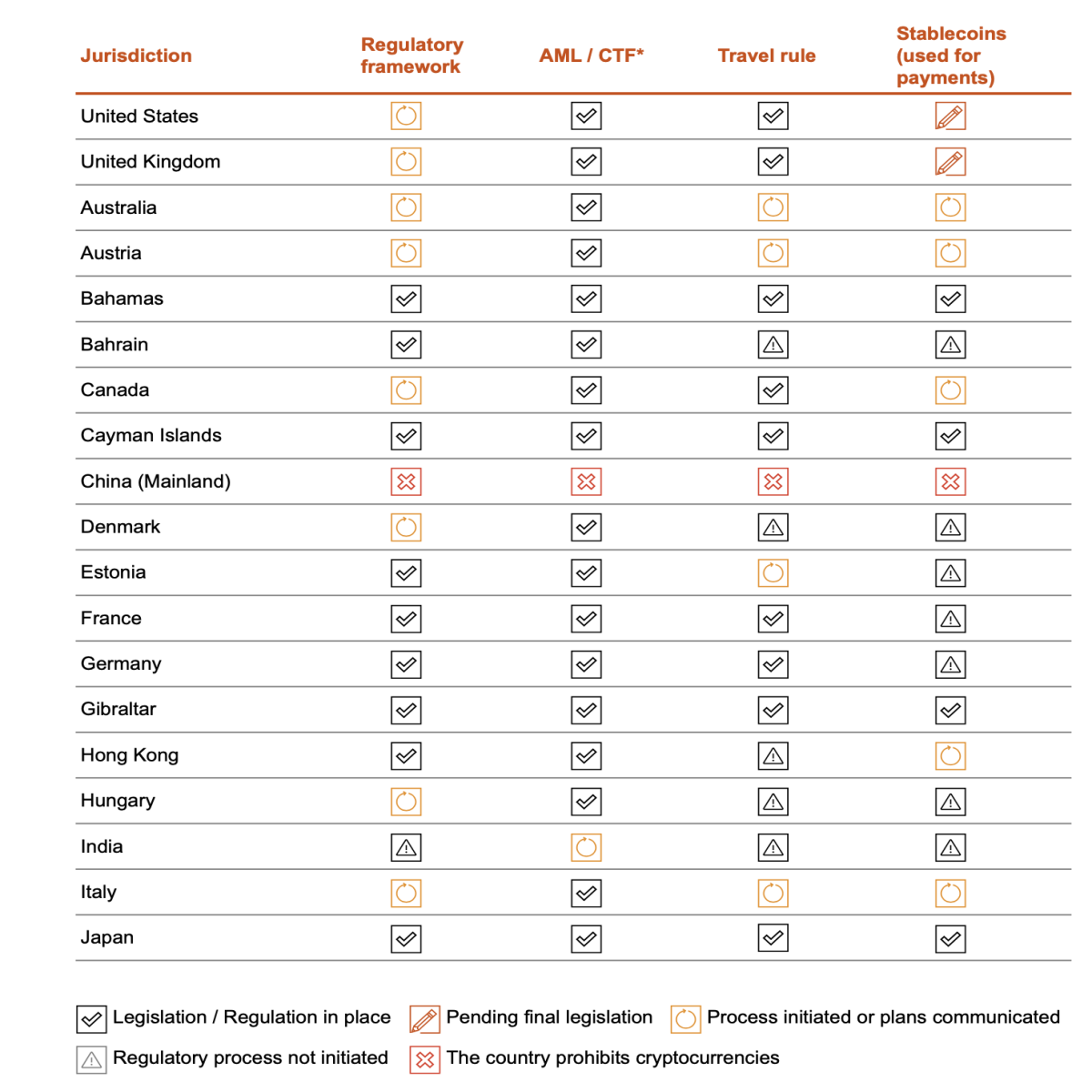

New hubs for cryptocurrencies are forming. For example, UAE is seeking to maximize the ease of doing crypto business in its jurisdiction by issuing clear and transparent laws and acts for regulation, as well as supporting the development of the crypto industry from its development funds and creating separate zones and companies. Examples include Dubai Blockchain Center (DBCC), Mubadala Investment Company, Crypto Oasis, Coinmena, and Venom Foundation. Also, many startups that want a comfortable environment for their development have already moved to Dubai, including Singularity DAO, Crypto.com, Bybit, Biconomy, and Elrond Incubator, and this trend is growing. According to the PwC Global Crypto Regulation Report 2023, AUE is one of the friendliest jurisdictions.

Figure 10. Source: PwC Global Crypto Regulation Report 2023

Figure 11. Source: PwC Global Crypto Regulation Report 2023

Figure 11. Source: PwC Global Crypto Regulation Report 2023

Following Dubai, after largely cautious and strict regulation in 17-18, Asian countries are beginning to soften the regulatory environment. Hong Kong has recently moved to liberalize conditions for crypto investors in its jurisdiction, with plans to lower the entry threshold from $1 million to CEX for investors. In December 2022, the Hong Kong Legislative Council passed an amendment to its Anti-Money Laundering and Counter-Terrorist Financing regulations that would apply the same rules to cryptocurrency as traditional financial instruments. The new licensing regime for virtual asset service providers is due to take effect on June 1, 2023.

Conclusion

There are prerequisites for L2 solutions to take a larger market share, as they already generate more TVL than most L1 solutions. Therefore, there is also a trend for infrastructure development around L2. This coule be a good catalyst for token prices of L2 projects, given the decline in L1 blockchain activity. These same narratives also make Ethereum a major blockchain as it is used as a settlement and execution layer. Another player that could take an important place in 2023 in the crypto industry is Cosmos due to its focus on interoperability and cross-chain support.

As transaction speeds increase, new opportunities and models for dealing with liquidity emerge. This trend is also reinforced by the declining confidence in centralized financial structures coming from TradFi and CEX and the increased interest of institutional players in DeFi, including in the context of RWA.

In the context of L2, another likely trend worth mentioning: is an airdrop season, which could be launched by L2s who have been waiting for their token launch for a long time. Such projects could include Arbitrum, Celestia, LayerZero, StarkNet, and zkSync.

Increased activity on the Ethereum network could offset the adverse network effects of unlocking large amounts of staked ETH after the Shanghai update. This could come at the expense of ETH burning with increased transactional activity as DeFi L2 develops and ETH returns to staking on liquidity-staking platforms. This could also give a further uptrend for tokens from platforms like Lido, Rocket Pool, cbETH Coinbase, and others.

In parallel, there is the development of user-oriented infrastructure: aggregators of DeFi applications, wallets and so on.

Also visible is the ongoing trend since 2022 to actively build regulation, and the forward in this direction is undoubtedly the UAE with their clear, transparent and easily accessible acts and regulations.

If 2021 was the year of flashy money and projects driven by short-term demand, and 2022 was the year of considering and accumulating, then 2023 is the time to roll back to the roots, structuring and improving the infrastructure for further development of the industry as a whole.

Disclamer

We are not financial advisors. The content on this website is for educational purposes only. In order to make the best financial decision that suits your own needs, you must conduct your own research and seek the advice of a licensed financial advisor if necessary.

Know that all investments involve some form of risk and there is no guarantee that you will be successful in making, saving, or investing money; nor is there any guarantee that you won't experience any loss when investing. Always remember to make smart decisions and do your own research!

References

- l2beat.com

- DefiLlama

- Cosmos Developer Portal

- William Doom “Optimistic Rollups”

- Vitalik Buterin “An Incomplete Guide to Rollups”

- msfew.eth “zk, zkVM, zkEVM and their Future”

- Garvit Goel “Bringing IBC to Ethereum using ZK-Snarks”

- Polymer Labs “Developing the Most Truly Decentralized Interoperability Solution | Polymer ZK-IBC”

- The Block “Research 2023 Digital Asset Outlook”

- Dev Berachain “Introducing Berachain”

- Naga Avan-Nomayo “Crypto Market Maker Wintermute Mulls Launching Derivatives Exchange After FTX Collapse”

- Prnewswire “Ondo Launches Tokenized US Treasuries and Bonds, Targeting $100 Billion Stablecoin Market”

- Suzuki Shillsalot “MakerDAO enters this new partnership: How will MKR react to it?”

- Steven Zheng “The Block Research’s Analysts: 2023 Predictions”

- PwC “Global Crypto Regulation Report 2023”

- Delphi Digital “The Year Ahead for Infrastructure” ********

- Delphi Digital “The Year Ahead for DeFi” ********

- Delphi Digital “The Year Ahead for Gaming”