TL;DR:

- A total stock market index fund is a good way to get exposure to US equity markets but probably not the best way.

- Indexing is actually factor investing.

- If you are going to index, maximizing your factor exposure through a small-cap value index fund tracking the S&P 600 value index might be the better way to go long-term.

If you go into any of the larger financial independence (FI) forums and ask the hive how you should invest, I guarantee you’ll get the following answers:

“VTSAX”

“Index funds”

“Read The Simple Path to Wealth”

All of these suggestions are leading you to invest your money in a single product: a total stock market (TSM) index fund. But is that actually a good way to invest? The answer: yes and no.

What is Indexing?

Indexing is probably the most widely lauded, yet misunderstood type of investing you can engage in. The premise is simple. By investing in a fund that tracks an index such as the S&P 500 (passive management), instead of one that hires people to pick individual stocks (active management), you can cut costs tremendously and pass that savings onto the investors. Those savings in turn, can lead to much higher total returns for investors over time. Add in the fact that most actively managed funds fail to beat their benchmark indices over long stretches of time and the case for indexing is hard to beat.

But here’s the rub. Depending on who you ask, indexing might not actually be considered investing.

What? How!?

Take a look at this definition of investing by Benjamin Graham (Warren Buffet’s mentor and widely hailed as the father of value investing). According to Graham in his 1934 text Security Analysis:

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

That one bit, thorough analysis, is where indexing doesn’t really meet the criteria. Unlike an actively managed fund where you (presumably) have fund managers analyzing each and every security going into the fund to make sure it’s a good investment, indexing does none of that.

With an index fund, the only criteria for a security’s inclusion in a fund is its inclusion in the index that the fund tracks. And with most index funds, the proportion or weight given to a particular security in a fund has everything to do with how large the underlying company is (its market capitalization). In other words, if you invest your money into a TSM fund and its top 10 holdings make up 20% of the fund’s assets; is it because those 10 holdings are solid investments? No. It’s because those 10 companies comprise 20% of the market capitalization for the entire stock market (kind of a scary thought honestly).

So what is indexing, really? Is it investing or is it speculating?

Personally, I like to look at it this way. It’s a little bit of both. On one hand, there’s no analysis involved with a straight indexing approach such as with a TSM fund so it’s definitely speculative according to Graham. On the other hand, there’s a good case to be made that with an index fund, you’re actually engaging in another type of investing known as factor investing.

What Is Factor Investing?

Factor investing finds its roots in some of the most widely cited academic research in the field of finance. In a nutshell, research has shown that in a diversified portfolio the majority of an investor’s expected return (and compensated risk) is generated not from the selection of individual securities, but from exposure to what’s become known as “factors.”

So what’s a factor?

Basically, a factor is a simple characteristic of a security that can influence it’s return. Things like does the security have risk? Is the company big or small? Is the company profitable?

Those kinds of things.

But how does that translate into indexing? To explain that, let’s take a look at three of the most widely accepted factors to give you an idea.

Market Factor

Out of all the other factors, when it comes to investing, the market factor is said to drive your overall return the most. To see if your investment has exposure to it, just answer this question: does the investment have risk? That’s it. In the US, that’s basically everything that’s not a t-bill. More specifically, if you bought a stock, you have exposure to the market factor and should get paid a premium for that risk (the equity risk premium).

That said, if you buy an individual stock, there are other risks at play and exposure to the market factor isn’t going to explain all your returns. An individual stock has specific risks that are separate and added onto the systemic risks associated with the market. Just like how the price of Bitcoin tends to affect the prices for most alt-coins, the systemic risks of the stock market as a whole will influence the price of individual stocks as well.

Here’s the thing though, as Harry Markowitz points out in Modern Portfolio Theory, you don’t get compensated for taking on specific company risks. By adding more stocks into your portfolio that aren’t correlated with one another (like mixing an airline company with one that makes shoes), you can eliminate specific risk. Do this enough, and eventually you’ll get to a point where you’re left only with systemic market risk (aka the market factor).

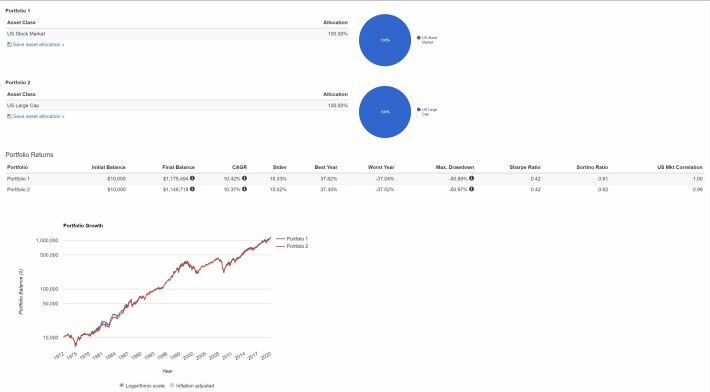

That is exactly what you get with TSM fund. Pure, unbridled exposure to the market factor and it’s volatility expressed by the Greek letter beta (β). It’s known as single-factor investing and it’s really all you’re doing when you invest with a TSM fund or any blended large-cap fund like an S&P 500 index fund.

And, just because the question comes up a lot, to illustrate that there’s no real difference take a look at the return profiles from each.

Source: Portfolio Visualizer

They’re virtually identical, so any debate on whether you should invest in an S&P 500 index or a TSM is a total waste of time IMO.

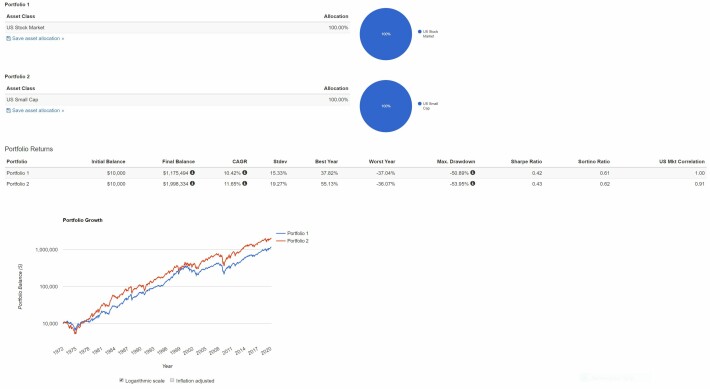

Size Factor

Next up, is what’s known as the size factor and all it really is a function of how large the company or companies you’re investing in are. If you invest in small companies, they’re said to carry more risk than large companies, and therefore, should give you a premium on your return. Makes sense right?

The size factor was popularized through the work of two professors from the University of Chicago, Kenneth French and Eugene Fama when they published their three-factor model. When you compare the overall returns on small-cap stocks to the TSM, you can see this pretty easily.

Source: Portfolio Visualizer

Over time, the smaller stocks provide a larger return over the broader index. Does that mean you’ll always get a better return with small stocks over large ones?

No.

There have been quite a few times over the past 50 years where larger companies have outperformed. Just look at the 1990s! Point is, if you want to take advantage of the size factor (or any factor really), you’ve got to be in it for the long haul.

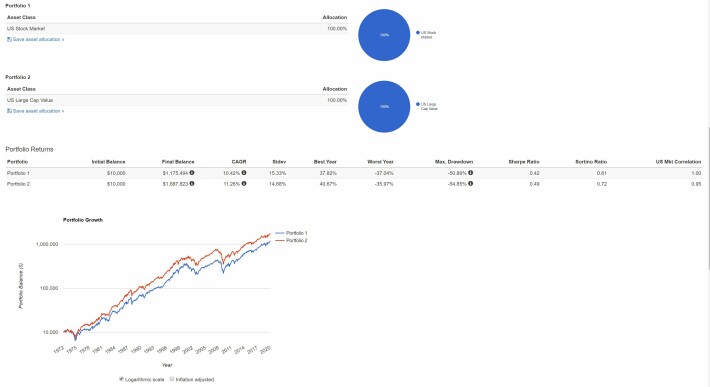

Value Factor

This last one is a little controversial. Traditionally, the difference between a “growth” stock and a “value” stock has a lot to do with the relation of the stock’s price to it’s earnings (P/E ratio) and it’s price to tangible assets (price to book ratio). The lower these ratios are, the better from a value factor exposure standpoint.

For example: take 2 stocks, one that trades at 50 times earnings and another that trades at 10 times earnings. If you’re looking to get exposure to the value factor, you’re going to go with the one trading at 10 times earnings.

However, this is where value investors can get into trouble. What if that company trading at a lower P/E multiple is trading that way for a good reason? Maybe the company’s about to get sued into oblivion? This sort of thing, known as a “value trap,” gives investing on the basis of value metrics its increased risk.

As you might guess, it’s this increased risk that can drive better returns with the value factor; and as you can see, exposure to the value factor has in fact done just that.

Source: Portfolio Visualizer

But just like the size factor, you don’t always get out performance in the short term. In fact, the past 10 years has been a pretty terrible time to be a value investor. That said, the next 10 years could be very different. Just like the size factor, the relative out performance of the value factor is somewhat cyclical.

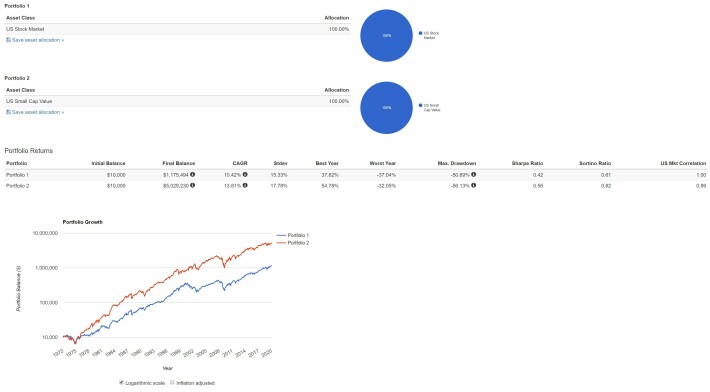

So Should You Just VTSAX and Chill?

Only time will tell for sure. But since index investing is really just factor investing, I’m going to put my money on the additional factors. Personally, I like combining all three factors in a small-cap value (SCV) index fund since I plan on holding it for the long run. In terms of the last 50 years, the total return on SCV compared to TSM is ridiculous. It's no accident that financial expert Paul Merriman is all about this approach to investing.

Source: Portfolio Visualizer

Specifically, I like funds that track the S&P 600 value index (SLYV, IJS, and VIOV) since you get exposure to smaller companies compared to other small cap indices like the Russell 2000. In addition, the S&P index methodology filters some of the less profitable companies which is a plus in my book. Taken together, it is a very tough index to beat long term. In conclusion, if you are going to index, feel free to chill; just consider doing it with something other than VTSAX. Thanks for taking the time to read!

Investment disclosures: I am long VIOV, IJS, and VTSAX and have no business relationship with any of their issuing companies.

Additional disclosures: I am not a financial professional and none of the content presented should be taken as financial advice as it is not intended as such. They are my opinions and that’s all. You should always direct questions about specific investments and your financial situation to a qualified professional.