RWA sector exploding: TVL ~$16.8-17B early 2026 (DefiLlama). But how do yields stack up against traditional banking (TradFi) and centralized finance (CeFi like BlockFi/Aave Pro)? Stable income without crypto volatility — let's break it down.

Yields Comparison Early 2026 (Approx., Fluctuate!):

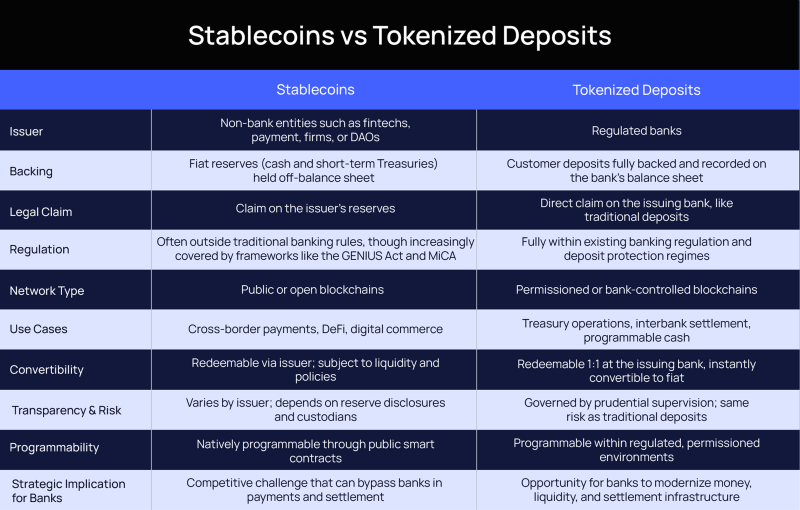

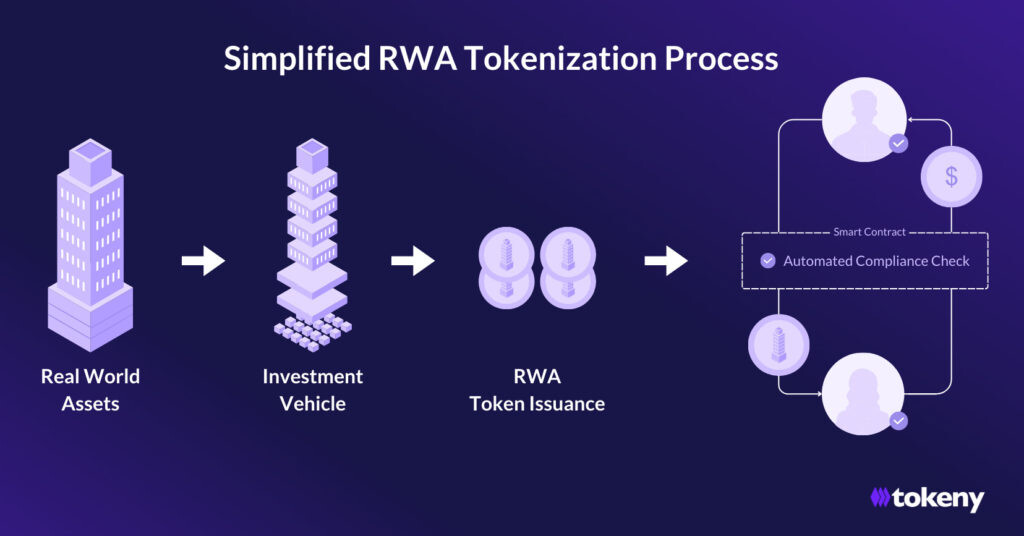

RWA (Tokenized Treasuries/Credit)

Yields: 4-15%+ (Ondo USDY ~5-10%, Centrifuge private credit 8-20%)

Pros: Backed by real assets (US Treasuries), on-chain 24/7, composable with DeFi (Pendle boosts to 30%+)

Cons: Custody/regulatory risks

TradFi (Banks/Savings/CDs)

Yields: 0.5-5% (high-yield savings ~4-5%, CDs similar)

Pros: FDIC insured, zero risk

Cons: Low returns, locked funds, inflation eats it

CeFi (Platforms like Nexo, LedgerPrime)

Yields: 5-12% on stablecoins

Pros: Easy fiat on/off, higher than banks

Cons: Platform risk (hacks/bankruptcy), no real backing sometimes

🔥 Why RWA Wins in 2026:

Beats TradFi yields with similar safety (Treasuries backing).

On-chain magic: Instant access, no banks.

Institutions (BlackRock BUIDL >$2B) validating it.

Net higher after low gas on Polygon/Arbitrum.

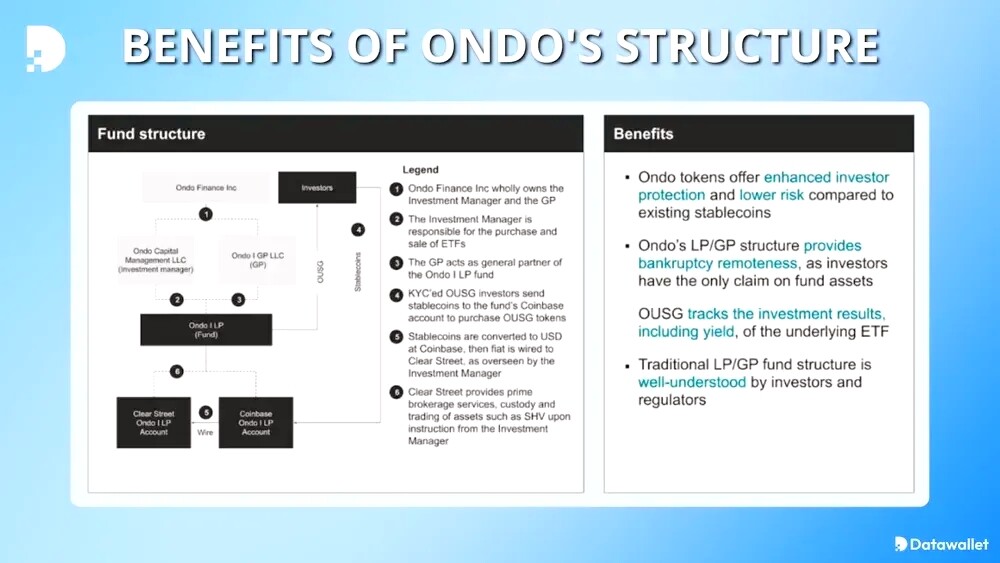

Quick Tip: Start with Ondo USDY for ~5-10% stable — better than bank, safer than pure CeFi.

Sources & Links (early Jan 2026 data):

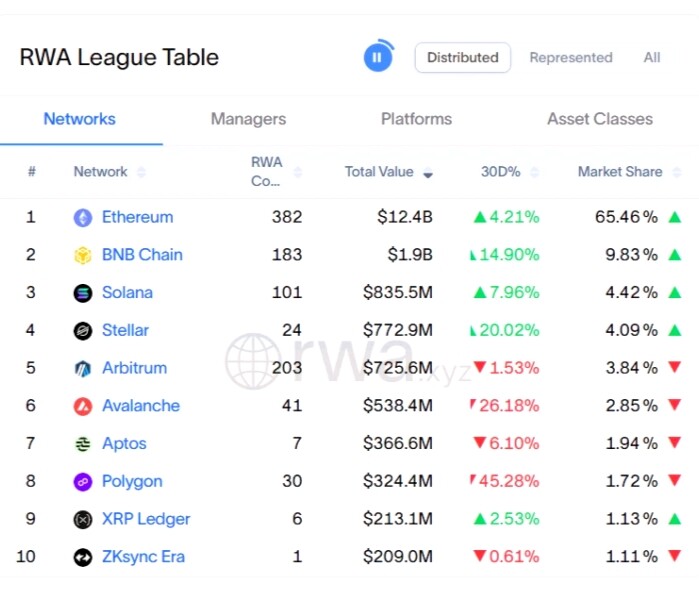

DefiLlama RWA: https://defillama.com/rwa

rwa.xyz analytics

Bank rates: FDIC/Federal Reserve reports

Ondo/BlackRock data: app.ondo.finance

Where do you park your money in 2026 — RWA, banks or CeFi? Share your yields/experience below, tip if this comparison helped shift your strategy, and let's stack real passive income together! 🚀👇

DYOR. Not financial advice. 🚀