A bit of economics

The eminent economist Hernando de Soto wrote a wonderful book called “The Mystery of Capital” with the subtitle of “Why Capitalism Triumphs in the West and Fails Everywhere Else”. That is the question to which de Soto seeks answer in the 290-page book.

The book’s premise is that the failure of capitalism in emerging and developing economies is a legal rather than a financial issue. Since it sounds cryptic if you haven’t read the book, I’ll elaborate on this. Contrary to what you might think, the poor of the Third World save. A lot actually. Per de Soto’s and his research team’s estimates the value of savings among the poor is forty times all the foreign aid received after the World War II. Even though the book was published in 2000, we don’t have any reason to assume that the reality nowadays is much different.

If this is the case, then why these countries don’t seem to be able to generate capital? If they have assets worth trillions of dollars, what hinders them to create capital? What does the West, the developed economies have that Third World countries lack in order to generate capital? What is the mystery of capital?

The reason is, de Soto confidently claims and convinces his reader, the “representational process”. Emerging and developing economies cannot create capital as efficiently as the developed world is that most of the resources in the hands of the poor are in defective forms. What does he mean by “defective forms”? in these countries poor’s houses are built in places where land ownership rights are not meticulously and adequately registered. Industries in these poor regions are located in places inaccessible to foreign investors and financial institutions. Even their businesses are not incorporated according to legal procedures accepted in the West. As de Soto puts it, these countries have “houses but not titles; crops but not deeds; businesses but not statutes of incorporation.”

That’s why the majority of the assets in most developing countries cannot be easily converted into capital. It is dead capital, an asset that has potential but cannot be put to use as capital. Assets in these economies cannot be used for purposes other than their direct physical uses. For the poor in the Third World, the house is a shelter only; it isn’t and cannot be used for business purposes or for taking a loan unless its ownership rights are accurately recorded. Resources cannot be used as a collateral for a loan; they are traded in the narrow circle of trading partners; they cannot be used as a share against an investment. What this means is that since businesses are mostly unincorporated, they cannot offer share of the venture to investors seeking to put capital in these businesses.

On the other hand, West developed the necessary kind of “representational process”. Almost all resources — equipment, every parcel of land, every inch of real estate, stores of inventories — are represented on paper. This property document integrates these visible, tangible resources to the rest of the economy. Thus, in the West assets can be and are used for purposes other than their direct uses. Here resources live invisible lives which are separate from their physical lives. This representational process makes it possible for assets to be used as addresses for collecting taxes and owner’s credit history among other uses. Not only this but assets can also be used as a foundation for the issue of securities, such as mortgage-backed bonds.

The Problem

Finance gap

That a significant part of available resources in emerging markets is dead capital has serious consequences. People don’t and sometimes cannot represent their assets on the paper. Couple this with high interest in these countries and regulatory requirements which make it harder for legacy financial institutions to lend to small businesses, and we get the infamous problem of finance gap.

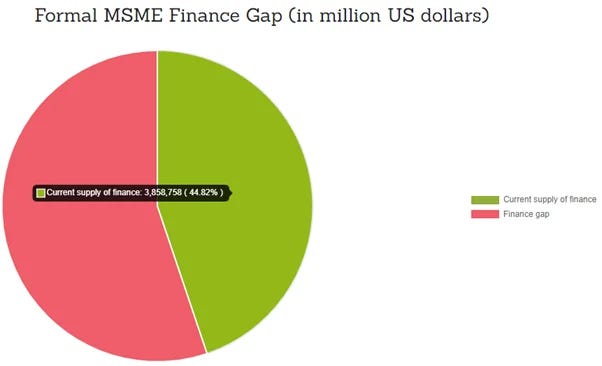

Finance gap for Micro, Small and Medium Enterprises (MSMEs) in developing economies is estimated to be about $5 trillion. This gap is 30% higher than the current level of MSME lending.

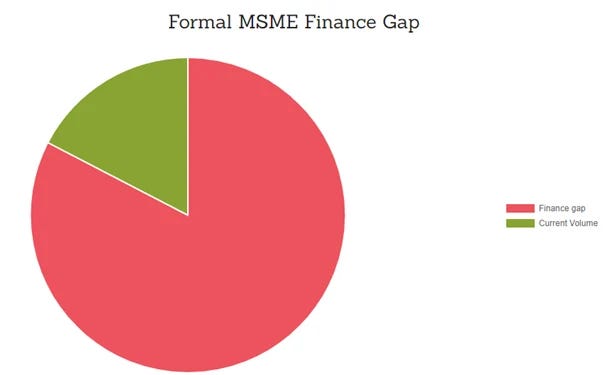

If we look at specific regions, the problem of finance gap looms more severe. Below is the diagram of MSME finance gap for Africa. MSMEs have been lent $70 billion while there is $330 billion finance gap — gap is 4.7 times of current supply of financing!

DeFi protocols

High interest rates make it harder for local businesses to access affordable credit. Given that emerging markets are chronically underserved in terms of lending and financing and legacy financial institutions and newly established fintech lenders cannot properly address this problem, it is almost inevitable that for the solution we should look beyond TradFi (traditional finance). This creates opportunities for DeFi which it has started to explore successfully. Bringing cheap credit to MSME in emerging markets and solving at least part of the notorious finance gap will bridge real world assets, developing economies and DeFi. Perhaps this is the way for DeFi to really alter the traditional finance industry and be adopted by masses.

Goldfinch

Goldfinch aims to create a global credit marketplace where anyone can originate a loan. The process begins with the Borrowers proposing deal terms for credit lines called Borrower Pools which are smart contracts containing information on the loan, such as interest rate and payment schedule.

Once Auditors verify a Borrower Pool, investors can provide liquidity by adding USDC to the pool. There are two kinds of investors on Goldfinch: Backers, who directly supply liquidity to the Borrower Pools’ junior tranches, and Liquidity Providers who diversify their capital by investing in many pools’ senior tranches across the protocol.

Borrower pools on Goldfinch consist of junior and senior tranches. A repayment made by a borrower to a Borrower Pool first goes to the payment of principal and interest owed by the senior tranche. Once the senior tranche is paid, any remaining part will go towards to the payment of the interest and principal of the junior tranche.

This is by design — it aligns the incentives of participants. Recall that the system depends on the Backers who assess the viability of Borrowers. Since they take highest risk by supplying first-loss capital into the junior tranche, they have to do a good job to evaluate an individual Borrower Pool. Liquidity providers, on the other hand, are more secure because they have first lien on the pools. This means in case of default they will be the first to be repaid. Since they bear less risk than Backers, senior tranches’ APY are less than that of junior tranches.

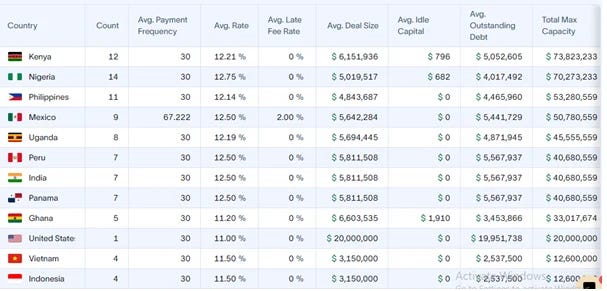

So, which countries does Goldfinch protocol serve? The dashboard above taken from rwa.xyz, the pioneering analytics company for tokenized real-world assets, shows that local businesses in two African countries, namely Kenya and Nigeria took out more loans than other countries. Excluding the US, where the protocol issued only 1 deal, all countries in the list are either emerging or developing economies.

Performance of the protocol

Lending pools on Goldfinch protocol are utilized efficiently. The chart taken from Dune Analytics shows that pool utilization rate has been almost always — barring several days when the ratio fell to 97+% — over 98% since 2022 May; it is 98.6% at the moment.

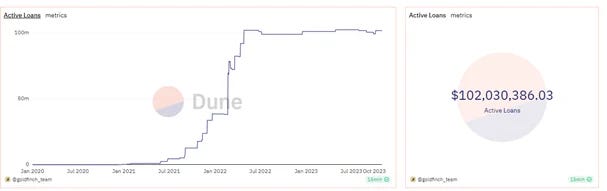

The chart below reflects the growth of the protocol in terms of active loans. We see that the volume of loans tended to increase since inception; in April 2022, the loans issued by Goldfinch reached $100 million mark after which it hit plateau. This is I believe not related to the protocol’s performance in particular but to the plight of DeFi after the infamous Terra blockchain collapse. Given the evolving landscape of the emerging economies, Goldfinch protocol has the great potential to grow even further.