I used to think the only way to use Bitcoin… was to sell it.

That changed.

Today, I haven’t sold my BTC — but I still:

- Create liquidity

- Generate yield

- And actively grow my position

This isn’t theory.

This is exactly what I do.

The Shift: From “Hold” to “Use Without Selling”

At some point, I realized something simple:

Selling Bitcoin solves short-term needs…

But it destroys long-term exposure.

And if you believe Bitcoin is going higher over time,

selling becomes the most expensive mistake you can make.

So I started asking:

How do I use my BTC — without exiting?

What 0.1 Bitcoin Might Actually Mean Over Time (Without Trying to Predict It)

My Setup (Simple, But Very Intentional)

Here’s exactly what I do:

- I deposit BTC (as WBTC) on Aave

- I borrow USDC only (no extra crypto risk)

- I keep my LTV at 30–35% max

- I take that USDC and put it to work in LP strategies

That’s it.

No crazy leverage.

No chasing 1,000% APR.

Just controlled, repeatable structure.

Why I Never Borrow More Than ~35%

This is where most people blow up.

They see they can borrow more… so they do.

I don’t.

Because Bitcoin moves fast.

A 20% drop is not rare — it’s normal.

If you’re overleveraged:

- You get liquidated

- You lose BTC

- Game over

At ~30–35% LTV:

- I can handle volatility

- I don’t panic

- I stay in control

This one decision matters more than anything else.

Why I Only Borrow USDC

I’m not trying to outsmart the market.

I want:

- Stability

- Predictability

- Clean accounting

So I borrow USDC.

That way:

- My debt doesn’t grow randomly

- My risk stays simple

- I know exactly where I stand

BTC is my upside.

USDC is my tool.

Where the Yield Comes From (My Actual Play)

Once I have USDC, I don’t just hold it.

I deploy it.

I use tools like vfat.io to find opportunities, and then:

- I enter liquidity pools

- I use ranges around ±20%

- I focus on fee generation, not speculation

Typical returns I see:

- 30–50% APR on the LP side

- Borrow cost: 4–6%

So yes — there’s a spread.

But it’s not free money.

It only works if you manage it.

Here’s a clean, natural version of the full section with the long-tail keyword clearly integrated:

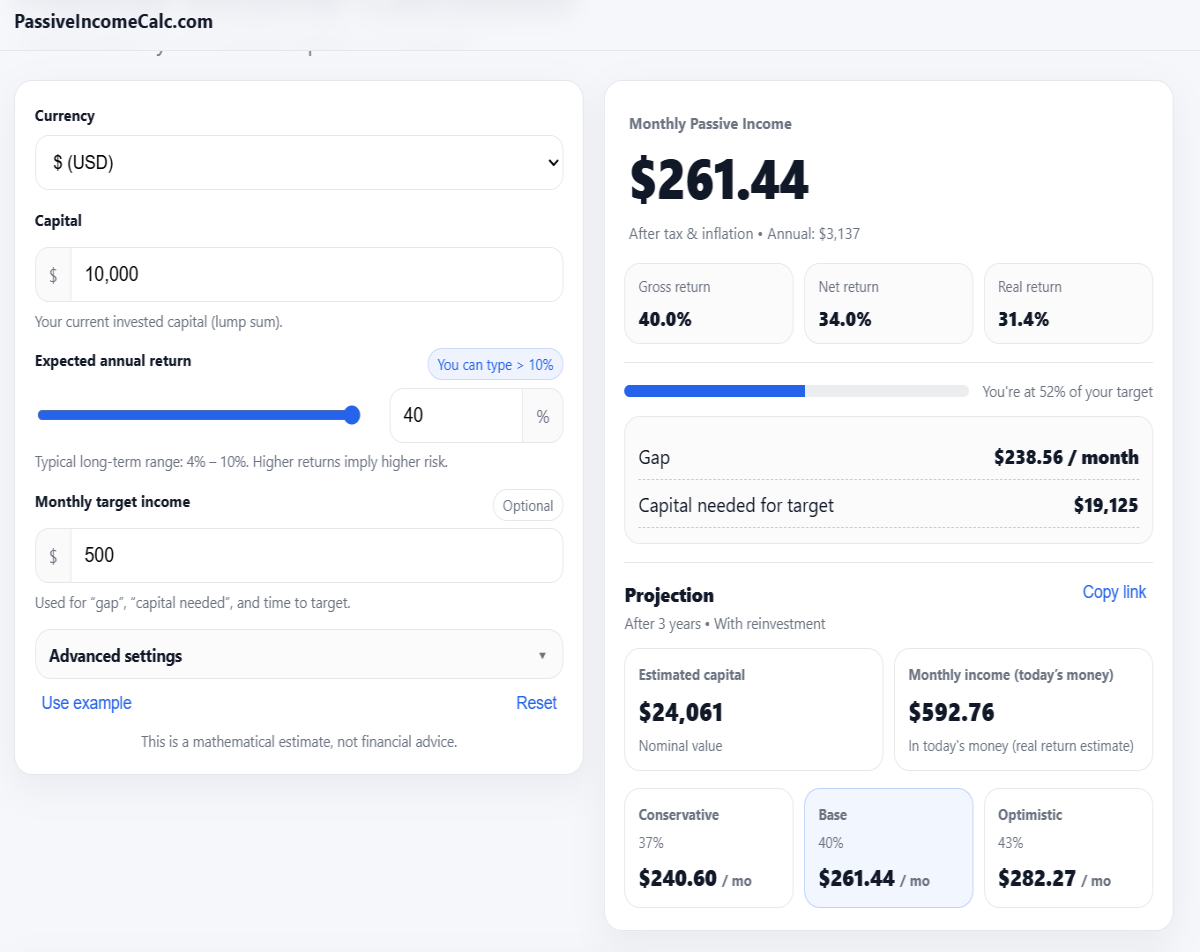

Here’s a simple passive income calculator monthly income example based on my setup. With $10,000 deployed at around a 40% return, it translates into roughly $260 per month after adjustments. That’s how I think about this strategy — not in terms of APR, but in actual monthly cash flow. Using a calculator like this helps me stay realistic, avoid chasing inflated yields, and focus on whether the setup actually moves me closer to consistent income.

What This Actually Feels Like (Not What You See on Twitter)

People talk about DeFi like it’s easy.

It’s not.

This is what it actually looks like:

- I check positions weekly

- I adjust ranges when price moves

- I harvest yield and redeploy

- I keep an eye on LTV constantly

It’s active.

But not stressful — because the structure is conservative.

The Risks (The Ones That Actually Matter)

Let’s not pretend this is risk-free.

1. Liquidation

If BTC drops hard and you’re too aggressive, you lose BTC.

That’s why I stay low LTV.

2. Impermanent Loss

If BTC moves strongly, LP positions shift.

You earn fees — but you don’t fully capture upside.

I accept this as the “cost” of earning yield.

3. Yield Changes

30–50% APR is not guaranteed.

It moves. Sometimes fast.

So I adapt.

4. Platform Risk

This is DeFi.

Even strong protocols carry risk.

So I stick to established platforms and avoid nonsense.

What Happens If Just 1% of Global Wealth Flows Into Bitcoin?

Why I Stick With This Strategy

Because it solves the core problem:

- I stay exposed to Bitcoin

- I generate cash flow

- I don’t need to sell

And over time, that compounds.

Not just financially — but mentally.

I’m no longer forced to choose between:

- Holding

- Or using my capital

I can do both.

The Part Most People Miss

This is not about maximizing returns.

It’s about surviving long enough to benefit from Bitcoin.

If you:

- Avoid liquidation

- Stay consistent

- Keep your structure simple

Then the yield becomes a bonus.

I don’t try to time Bitcoin anymore.

I just make it work.

And as long as I:

- Keep my LTV under control

- Stay disciplined

- And don’t chase stupid yields

I get the best of both worlds:

Exposure + income

Without ever selling.