The Ample or the Bond

The article image is of a compliant mechanism*

**important author's note** The term "stable" is used loosely in this article at times. You will see a call for the need of "stable" value in this article for writing DEFI smart contracts. While Stability does imply a constant equilibrium, nothing in this world is perfect, in the same sense that no blockchain protocol is actually "truly decentralized" because it has centralizing components to it depending the context in which you are judging it, compared to one's abreast ideals of "decentralization". Im not an expert on that topic, but the general consensus is that Decentralization isn't a sigular state, but rather a spectrum. Allow me to apply the same logic to "stable" for the purpose of my essay. I'll put forth then, a caveat for this writing that the "stable" value we search for more accurately fits the definition of a Semi-Stable property within the spectrum of "stability", from completely stable, to completely unstable. The point is that Ample will converge around "stable" state, while unstable assets like bitcoin always diverge to "unstable" state. Language is very precious and I simply don't want to confuse anyone. My usage of words could be wrong; either ultimately, or simply in your own opinion, but the only goal would really be that you can understand the contents of the article. **

Smart contracts and decentralized computation require certain properties to work. For starters, you need to have a stable value that is liquid in the network; meaning there needs to be a certain tool or set of tools which act as either stable value or a proxy for stable value, and it has to have deep liquidity on open markets. Blockchains like Bitcoin will forever have their significance within the global economy because they offer the only viable, fiscally sustainable, and scalable solution to borderless and uncensorable exchange of a unit of account. No other asset has or will have these qualities, and therefore the internal currency must be native; it must be Bitcoin, otherwise these properties are referential to an asset that can nullify them. The problem is that Bitcoin is obviously unstable. While its unit of account (bitcoins) is borderless and uncensorable, it does not offer any sort of stability for the foreseeable future. If you ask someone who thinks Bitcoin is a fad, more often than not they will recite to you that Bitcoin is too volatile; while this is true, Bitcoin is most obviously not a fad. Bitcoin, and more expressive blockchains such as Ethereum, offer the viability to have economies that are more open, trustworthy and efficient. Tamper proof digital agreements are a transformation; rather than a fad. The value of these tokens, and by proxy, the value of the network, offers people a bandwidth for the maximum amount of economic activity that can take place on the network.

While very interesting applications arose from these Network Protocols; such as payment escrow, collectable non-fungible assets, digital identities, lending and borrowing and so on, the holy grail of these decentralized financial applications is the stable coin. This, for example, means that if you took out a blockchain loan, the repayment amount doesn’t randomly skyrocket. In these decentralized economies we call “Blockchains”, we need on-chain (native to, and “living” on the network) assets that behave in a stable manner so that the blockchain network has stable bandwidth in it to write stable contracts; sort of a Stable Liquid Value if you will, or SLV for short. The more completely on-chain SLV bandwidth that your decentralized financial network (economy) provides, the more utility it provides to the broader economy (like lending and exchange markets). That way these financial applications can write contracts with stable value represented purely on-chain. While there have been many attempts to produce tools with all these combined properties on the blockchain, most seem to either repeat the same mistakes as old finance, or fail to offer an efficient and scalable solution, and ultimately compromises on the properties I described about blockchains. One such solution is the “Bond Coin''. We will dive into why this solution doesn’t work, and why I believe The Ampleforth Protocol and other elastic currencies are the most scalable, simplistic, efficient and viable solutions that we have.

Bond Redemption Coins

Disclaimer: I will note in very good faith that these projects do offer a product with instant viability when it comes to its semi-stable value. In other words, these products undeniably offer a more stable asset in the short term. If contracts are worth tens of billions of dollars, then a simple $.50 fluctuation on the agreed asset is massive and could trigger marginal clauses such as a stop loss. Stability matters, but in my opinion it still matters less than exactly how you get there.

Among the stable asset solutions is the bond coin. Basis (previously Basecoin) is one implementation of bond based stability mechanisms. The Basis Protocol consists of 3 coins: The Basis Stablecoin, Basis Shares, and Basis Bonds. The Basis Stablecoin is pegged to the U.S. Dollar 1:1, and Basis Shares are a parametric governance token that shareholders can use to vote on policy changes. The Shares token has a fixed, finite supply. This is similar to the Maker governance token in Makerdao and is expected to be volatile throughout the protocol's history. The only main difference being that Maker’s supply is not fixed; its inflation policy keeps shareholders on the hook for DAI having its $1 market stability. The Bonds in Base Protocol come into play for the stabilization mechanism of Basis which we’ll now go over.

Stabilization Mechanisms

- When the Basis Stablecoin’s price goes below $1, the protocol burns holder’s tokens through an open auction for its network’s “Bonds” which have no fixed price but function as a promise to 1 Basis stablecoin at some point in the future. Supply burns function to regain $1 value equilibrium

- Now with that “1 Basis within 5 years, only after a certain maturity time” bond, you will expect the oldest bonds to be redeemed first, as the system works on a “first in first out” Bond Queue, where, you guessed it, the oldest bonds are first to be sold at a 1:1 ratio during Basis (stablecoin) supply expansion. Bond holders are incentivized to want these bonds at a price below $1, in order to later convert them for a premium based on the expectation that the Basis (stablecoin) will return to or above $1.

- When the price conversely rises above $1 the mechanism in place for lowering the price is to mint new Basis (stable) and distribute them to the shareholders, those who hold the Shares token in the protocol. New Basis (stable) will be minted until the selling of tokens brings the price back down to the $1 target.

The Bond market (assumptions gone awry)

With any monetary scheme comes inherent risks. Some risk is very simple, like “demand for Decentralized Finance may fall or disappear”. While I find this particular risk to be more implicit and less likely, there are explicitly auxiliary risks that plague the space, such as collateralized debt positions and junk bonds (risky low-grade investments) that have much more systemic, cyclical, and pronounced risks, and even defects, than their simplified source monies, or base monies (bitcoin, ether, gold, amples). I think conflating these risks isn’t just a disservice to investors, but an intellectual disservice against mankind. I believe that conflation of ideas, especially in economics, leads to decades if not centuries of stagnation and misunderstanding in social dynamics. I find these effects to be ephemerally pronounced and existentially profound, but I also believe that cryptocurrencies have alleviated this blockage in thinking, and generated a more transparent and open ecosystem. That being said, let’s look at potential shortsightedness in the Bond scheme’s design.

The bond coin wants to offer a sustainable and reliable exchange rate for their stable asset. This design takes a lot of inspiration from the open market operations of the Central banks where the banks go to the open market to buy and sell U.S. backed securities in order to adjust (increase or decrease) liquidity on reserve in the U.S. banks. But there is a primary difference between traditional Central Bank OMO’s(Open Market Operations) and the bond coin, and that is that OMO’s are reinforced by legal requirements and the need for secure assets in reserve. The government bonds sold are considered safe assets, and they tend to be yield-bearing unlike cash. The bonds are so reliable that foreign countries will buy them; especially because of the high and seemingly endless demand for the U.S. Dollar. The real world demand for dollars and the United State’s global dominance makes these bond IOU’s extremely sought after, even in times of turbulence, the bonds can be negative yielding and still be more desirable than holding riskier assets. I believe the mass utilization of negative yielding bonds at scale, especially in hedge fund portfolios to hedge losses, is a testament to the economical output, dominance and reserve of the United States, and causes these yields, positive or negative, to still be sought after. In other words, the United States Bonds are not reliant on high yields to stimulate demand for them; However, these stablecoin schemes with bond coins are.

Whenever the stable coin naturally loses demand, the protocol needs to raise the exchange rate, or price, and it can do this by reducing supply. So the protocol issues “bond” coins in a staking contract with a yield. Market speculators will keep buying bonds thus reducing Basis (stable) supply until it reaches the desired peg again. Market speculators chose to buy bonds and instigate this stability mechanism based on the opportunity of yield from the series of bonds that were created. By definition, the yield from these bonds results in more Basis (stable) coins than were originally in the contract, and thus generates larger Basis (stable) liquidity than before the bond issuance epoch. This premonition of a diminishing value may have already set in with you, if not let’s elucidate everyone. This means that the mechanism of yielding bonds, by definition generates an ever increasing oscillation of lower pricing in the stable asset. Eventually the demand for bonds will be exhausted and the peg will break. And that is why the bonds act more as corporate junk bonds than U.S. treasuries, because they ultimately rely on speculator’s demand for risky yield while U.S. bonds do not.

Basis Shareholders need to believe that Basis (stable) coins will have an increase in demand. Bonds may become worthless because the stablecoins need to constantly be in demand in order for bonds to be effective at stabilizing price. Since these coins’ values are so intertwined, if the price of Basis (stable) falls far enough from the peg, market speculators may lose faith in the Protocol’s ability to return to the peg. This means a majority of Bond holders may end up with worthless bonds if a downward spiral persists and the blockchain continues to lower the auction price of bonds.

- Secondly, to address further inefficiencies, Basis Shareholders have a financial incentive to let the price rise as far above the target price as possible so that they receive as many minted tokens as possible. Compare this to Ampleforth, which not only has incentives that encourage market speculating arbitrageurs to close gaps in price oscillation, but it also benefits the ecosystem as a whole with its proportional and non-dilutive expansion policy. In other words, with ampleforth it is in the collective’s implicit and explicit interests that the asset remains stable, and everybody’s “share” or “slice of the pie” naturally grows with the network which is far more efficient to benefactors and holders without introducing an extra token or two.

- Sharp price drops may create a negative feedback loop where the falling price of the stablecoin causes speculators to back away from bonds which would let the price simply continue to fall. In this case the monetary scheme would stop functioning

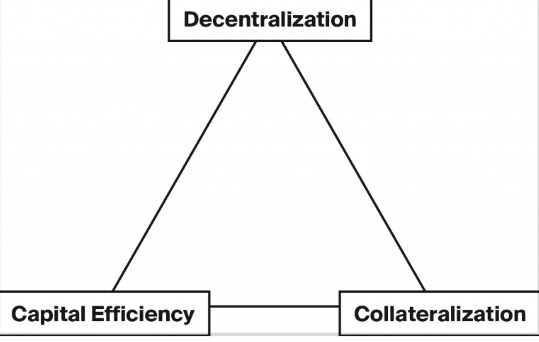

Capital Efficiency:

There are trilemma issues in the Stable coin sector, just as we see scalability issues in blockchain: 1. Decentralization 2. Collateralization 3. Capital Efficiency

- We rate “stablecoins” partially with how decentralized they are. Totally decentralized money like Bitcoin or Ethereum favor highly in this category; however, neither have any stabilization mechanism. We opted towards centralized stable-coins, which would maintain its 1:1 peg by more or less using a centralized custodian who would add and remove dollars from a reserve pool that backed the digital stable-coin. The clear issue with this solution is that breaking away from the decentralized ethos of blockchains will eventually erode the guarantees and atomicity of digital tamper proof agreements. Because we use blockchains to prevent counterparties from defaulting on an agreement, a scenario with ever increasing risk of insolvency and default introduces systemic risk to the Defi and blockchain ecosystem. This is how we came using solutions like MakerDAO, which would use fully decentralized money for the collateral.

- Projects with fully decentralized collateral, like MakerDAO, will by definition have fully decentralized functionality in contracts. This would mean, for example, that lending and borrowing contracts with stable assets can meet the same decentralization standards as all the other on-chain contracts. With this ability, we can continue to build complex contracts with many protocols together without systemic threats of centralization or counterparty risk due to an off-chain source. The only problem with fully decentralized collateral like Bitcoin and Ethereum is that these assets are inherently volatile. Once again, we run into problems due to volatility. Due to so much inherent volatility in the decentralized native blockchain assets, these stablecoin solutions like MakerDAO have to overcollateralize their stable DAI coin.

- Overcollateralization means the token can’t be minted with equal collateral, like $1 for 1 DAI. You need to lock up $1.5 for 1 DAI, even though DAI will only get you $1 on the open market as per the stability policy. This makes the stable token very inefficient for scaling capital into, because you will always need a far greater degree of collateral to generate stable currency. It is worth noting that in a higher order of things, the collateral in this scheme is the base money from which the Stable asset derives. This is why many stables are called “derivatives' '. This means that there will always be a greater importance put on the base money, and it is treated as a first class asset, while the stable currency is subject to policy parameters enacted by the protocol shareholders. Also, this makes it very inefficient to use with on leverage. Since you need to overcollateralize positions for generating DAI, these “collateralized debt position-based” systems result in a diminishing rate of return, for each round of borrowing being done in a leveraged position. This makes it harder for users to utilize leveraged positions in decentralized applications and to perform borrowing for arbitrage opportunities across the market.

Final reflections on capital efficient solutions and “Derivatives vs. Base Monies”

One of the greatest problems that still tends to persist within (or plague like a haunting spectre) the capital efficient solutions of stablecoins is the governance itself. As the need for overcollateralization is removed, the now efficient stable currency pegged with bonds has an even more extreme pressure to preserve the health of the network. MakerDAO and Synthetix at least have these inefficiencies with collateralization and leverage in order to scale the protocol in a safe and pragmatic manner. The capital efficient, fully decentralized bond coin, despite all of its pros or cons, has a strictly greater responsibility towards healthy monetary policy, mitigating systemic risks, and maintaining the pegs in their system, while onboarding potentially trillions of overleveraged positions of the financial market. I think it’s worth noting that governing protocols like these comes with a need for active time and effort to maintain safety in their financial product, with less systemic risk. And while I do complement them for their efforts, it’s easy to conflate the systemic risks of protocol contracts, and the general systemic risks of leveraged finance. I believe there will always be high risk environments in finance, and because of that, I tend to focus on low entropy, simple, flexible protocols that can take the burden of financial risks and adapt to them, without the need for governance (health parameters like CDP ratios, debt ceilings, interest rate). I think this was always Satoshi’s vision, and I believe truly in a renaissance happening in Defi among the Ampleforth communities that are connected to the “un-governance”, crypto-anarchist ways of the space.

If we observe the Basis Shares token as extractive and rent seeking because it rewards holders through inflation, it can also be seen as an inefficient waste of energy and plutocratic by design. So while Basis has more initially scalable stability, its governance is extractive and will result in centralized tendencies around “supporting the growth, health and development” of what is effectively a bond or “options” market on stablecoin futures. The Shareholders effectively have to encourage the growth and adoption of the stablecoin and its demand, in order to assure predictive long term health and viability. This, in a meta sense, is EXTREMELY capital inefficient and should ultimately dock points off of the Bond market stablecoin scheme. The only thing that any of these projects have over Ampleforth, or other simple elastic rebase protocols, is their short term success at stability. But that appears to be the only plus ever in sight, and as the saying goes; “it’s best not to sacrifice long term goals for short term gains,-and to avoid a parasitic, conflicting rent extraction systematically within the defi primitives''. Most of these stable currencies, without calling any out in particular, are nothing more than convoluted ponzi’s to extract money from the increasing demand in defi for stable liquidity. That’s the most cynical way of looking at it. The most positive outlook is that it solves the short term inefficiencies of “capital efficient Defi stablecoins'', by integrating an extraction scheme of dividends for the wealthy, which doesn’t have an effective purpose beyond stabilizing the network in the long run. This creates a permanent necessity of rewarding stakeholders of a bond market. On the other hand you have Ampleforth, which is a base money. It’s therefore a first class asset that accrues fundamental value in its own right by being an elastic medium of exchange and unit of account. Ample is used for monetary purposes only, and is antifragile in policy because it simply rebases the base money, and nothing more. While ampleforth is rough around the edges in terms of fluctuations, it still won’t be able to suffer from runaway deflation, or any other health risks. Ample is an elastic primitive and its “health” condition, like its contract’s security, are redundant.

Ending thoughts to be left with: there are many new effects that come from elastic non-dilutive money. I have mentioned many concepts already but here is one more to think about when pondering elastic finance:

Hyperinflation immunity

When a nation or civilization goes through hyperinflation many horrendous things like poverty, homelesnness and death will almost certainly occur. One of the main reasons we enter such a vicious cycle is due to the weak mechanisms in place to balance national fiat currency. Creating new debt positions and bank balances to stimulate the economy results in an excoriating inflationary spiral of the money, and an egregious devaluation ensues. Humans will attempt to avoid paying for higher prices tomorrow by hoarding durable goods like scarce metals and mechanical equipment. In an extended period of hyperinflation that is indefinitely out of control, humans will also start hoarding perishable goods as well.

If the economy were a bodily blood stream, these instances of hyperinflation would all be blood clots blocking the healthy flow of goods and services from circulating. One incredible side effect of Ampleforth’s strict smart contract based, immutable monetary policy of perfect elasticity is that it can hypothetically (and in my opinion, likely) prevent these instances from occurring at all. The inadvertent incentives of hoarding created by hyperinflation is a non issue in the Ampleforth Protocol. I like to think of this hyperinflationary gridlock on the economy as an economic halting problem, which Ampleforth’s pure uncorrelation from external states seems to have the potential to eradicate in the long term. Rules based (smart contract) economies have the power to save economies at the protocol level <3 . good monetary policy saves lives.