I am a certified public accountant (not an artist) that is based out of New Jersey, and I'm continuing my extensive guide covering the interactions of United States tax law and cryptocurrency.

The cost basis of an asset is its original value which is typically the price that you paid to acquire it, or the assets value when you exchanged something else for it. Cost basis accounting revolves around deciding the methodology to use for determining what the cost basis of an asset should be when you make a sale. There are many cost basis accounting methods, each of which become more or less beneficial depending on your own circumstances. I'll be covering the more popular methods out there, along with things to keep in mind when deciding on which method makes the most sense for you.

Which cost basis accounting method does the IRS require?

The IRS allows tax payers to utilize specific identification for reporting gains and losses during the sale and exchange of cryptocurrency. This enables you to decide which cost basis method you would like to use, as specific identification encompasses all of them.

There is one thing to keep in mind: if you do decide to go down the route of specific identification, you should keep track of, and be able to show the following:

- The date and time each unit was acquired,

- Your basis and the FMV of each unit at the time it was acquired,

- The date and time each unit was sold, exchanged, or otherwise disposed of,

- The FMV of each unit when sold, exchanged, or disposed of, and the amount of money or the value of property received for each unit

To put this into slightly nicer language:

- When did you buy it?

- How much did you pay for it?

- When did you sell/exchange it?

- What were they worth when you sold/exchanged them? What was the value of the money/property that you received? (These two are generally going to be the same, unless you paid any fees during the sale/exchange)

In the event that you can't you provide this level of detail, then the first in, first out (FIFO) basis will be used.

FIFO (First in, first out)

FIFO is the most common cost basis accounting method that is utilized in day-to-day business transactions. FIFO is also straight forward: the first things you sell (first out) are first things that you bought (first in). The perfect example is the produce section of a grocery store. When new produce comes in, the stores employee will rotate the product, and bring the older stock to the front of the display. The new product will then be placed behind the old product. This encourages shoppers to pick up the produce that was first brought into the store, which will prevent spoilage.

Thankfully: cryptocurrency doesn't really spoil.

LIFO (Last in, first out)

LIFO is used sparingly in business transactions as generally accepted accounting principles (GAAP) is converging with the International Financial Reporting Standards (IFRS) which does not permit the usage of LIFO. LIFO is almost exclusively used to reduce a company's tax burden, and doesn't typically match up with reality. LIFO is the opposite of its other half, FIFO. The first things you sell (first out), are the last things that you bought (last in). It's hard to think of an example of LIFO that makes sense, as LIFO doesn't really make sense from an actual usage perspective.

In that case, why exactly is LIFO used? Generally, the last items you bought were the most expensive. This means that selling those items first will result in the lower income position, reducing your taxes.

HIFO (Highest in, first out)

HIFO is a method that typically comes up in the cryptocurrency space, and has the best advantage of LIFO in a market that fluctuates a lot more than grocery store produce does. When it comes to HIFO: the first things you sell (first out), are the most expensive things that you bought (highest in).

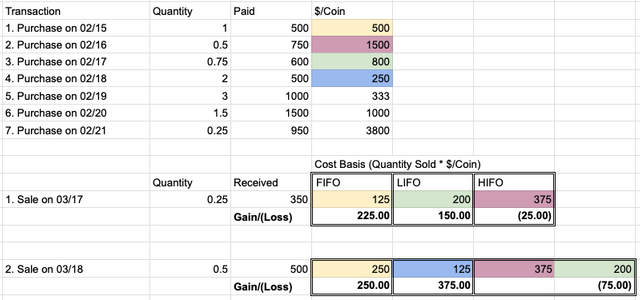

Comparing FIFO, LIFO, and HIFO

This short list of transaction shows you how the cost basis method that you choose to use can drastically impact your gain and loss on a given transaction. As is expected, HIFO results in the lowest overall gain/(loss), but LIFO and FIFO can swap places depending on when you made your purchases.

I also showcased why precise tracking is very important. Using HIFO resulted in selling through the cryptocurrency that was purchased on 02/16, requiring you to sell a portion of your 02/17 purchase as well.

HIFO is only good as long as you continue to have cryptocurrency to sell that you purchased at a high price. Eventually, all three of these methods will result in the exact same gain/loss if you sell off all of your investments. For this reason, I think it's more important to consider your individual circumstances instead of flatly deciding to adopt any of these methods.

The Best Strategy Depends on Your Circumstances

While having a method to follow is all well and good, the best tax scenarios can only be materialized if you take a look at your own individual circumstances. While I can't account for everything, I'll try to provide a general overview of what you should consider before you decide which unit of cryptocurrency to sell or exchange.

Your Current and Expected Income

If your income levels are currently on the lower side, then selling off your investments with the lowest cost basis now may make the most sense.

Similarly, if your income in the current year is higher than what you'd expect in the future, then selling off investments with the highest cost basis may make the most sense.

Your Holding Period

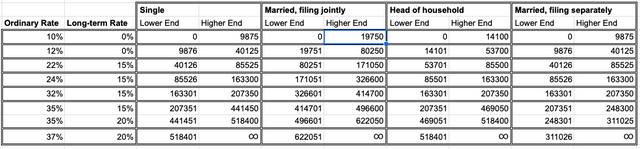

Length of ownership is also important: do any of your cryptocurrency purchases have a holding period of longer than 1 year? You could pay as little as 0 tax on long-term capital gains, depending on your income levels.

Your Generosity

While I do plan to cover donating cryptocurrency to charity more in the future, it is important to mention that there are deductions available for donating to a tax exempt organization. (This can get fairly complicated, check out Publication 526 if you are considering making charitable contributions.)

Your Expectations on Future Tax Laws

This one is a bit of a weird one to think about, but it can change your decision making process as well. Do you expect Congress to increase individual tax rates as time goes on? Do you expect the tax treatment of cryptocurrency trading to become harsher?

In Conclusion

Cost basis accounting can be complicated and incredibly cumbersome to manage as we engage with dozens of exchanges and different wallets. The IRS treatment of cryptocurrency as investment property means that your cost basis will change with each exchange that you make. Diligent record keeping, while difficult and time-consuming, will translate to real world dollars saved when it comes time to file your taxes.

If you have any questions, feel free to ask them below, or on Twitter. They can relate to the items above or about anything else that is tax related.

This material, and any responses below, have been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal, investment, or accounting advice. You should consult your own tax, legal, investment, or accounting advisors before engaging in any transaction.

US Tax Law and Cryptocurrency:

- Part 1: The Basics on LeoFinance, my own blog, Medium, Reddit, and Publish0x.

- Part 2: Tax Loss Harvesting and Wash Sales on on LeoFinance, my own blog, Medium, Reddit, and Publish0x.