Deferral options range from unexpected to uninspiring

This article originally appeared in The Capital. And yes, I give myself permission to repost it here on P-0x ;-)

As a resident of a lockdown state, I recently contacted four credit card providers to gauge their customer experience during a global pandemic. It’s apparent that, like most of us, they weren’t ready for this.

Two pounds of rice was the only important staple during a recent trip to the store, and I haven’t seen a sellable roll of toilet paper in as many weeks.

The local parks are shuttered, including the nearby mountain’s hikes. Since it’s impossible to stay 6-feet apart on narrow trails, it’s no longer safe to travel paths that provide a much-needed escape from quarantine.

Most of us remain inside — unexpectedly transforming into self-isolated, unemployed babysitters, caretakers, and teachers. And that leaves us with tough choices to make.

On the credit front, unless the situation suddenly changes for millions of cardholders, banks may just become victims of the novel ‘I-owe-ya’ virus.

In other words, food and shelter take priority over paying into the debt system. And after personally contacting four of them, it’s evident that the banksters aren’t straying far from business as usual.

All of these banks charge exorbitant amounts for carrying a balance — money loaned out from customer deposits. See how that works?

Banks loan customer deposits to other customers, charging borrowers double-digit APRs — some crossing 20% — while paying depositors what now amounts to 0.08%. Sure, that’s a fair and balaced system.

Monthly statements are kind enough to point out that continuing to make minimum payments means not only paying double the interest but also taking 17 years to do so.

Who knows what the markets will bring once we finally conquer the latest global virus. It’s safe to assume that, per usual, banks get bailouts.

And while the misnomer, private corporation (read: not a government entity) we call the “Federal” Reserve fires up the printing press, I’m checking into deferral options.

Beginning with $2.2T, “The Fed” intends to print “unlimited” cash to purchase “unlimited” assets.

Central banks' money presses go "brrr" all day every day

Call me crazy, but the current pandemic is sounding more and more like one phase of an elaborate scheme concocted by an elitist group intent on buying the globe at a discount.

And if that group continues to devalue the global monetary standard — ironically backed by nothing but the hot wind of politics — they only make purchasing assets easier on themselves.

Conspiracy theories aside, we’re still living in a world run by banks, and like you, I have bills to pay.

After contact, banks fell into separate ranking categories: overall service, and deferral leniency.

Surprisingly, one bank seems willing to take a rare financial hit on behalf of cardholders. Which one is it? I’ll tell you soon. But first, I’ll let you know which one it’s not.

👎 Wells Fargo

In times like these, and in “regular” times for that matter, I regret having to do business with this organization. I hear you asking, “but can’t you just transfer the balance?” Thanks for the suggestion, but it’s a little more complicated.

Move along — this isn’t the card you’re looking for

I’ll share further details in a bit, but I was victim to a fraudulent series of events a few years back. I had to deal with these fake-account-creating hucksters to file a claim.

And, especially compared to a competitor, this bank offered zero help.

So, unsurprisingly, I had the worst customer experience through Wells Fargo during my quest for payment deferrals.

In fact, it’s been days now, and I still can’t get through to determine deferral options. Here’s what’s transpired so far:

Thursday, March 26

No chat option on the Contact Us page, but there’s a number to dial.

After playing everyone’s favorite game of button-pressing and being instructed to “listen carefully because our options have changed,” as if we’d memorized them before calling, I was informed of a separate number to call.

One can only spend so so much time on hold. Every 15 seconds, we’re treated to an interruption in the jagged funk hold music to hear, “we apologize for the delay. All representatives are busy assisting other customers. Your call will be answered in the order in which it was received.”

After roughly 20 minutes, it was time to tap the red button.

One can stay on hold for only so long...

Friday, March 27

More of the same. Waiting and waiting, with no end in sight.

Saturday, March 28

I called too late. Turns out, this isn’t a 24/7 number. Once again, Wells Fargo sets itself apart in the wrong way.

Monday, March 30

Big surprise — nobody’s answering. Twenty more minutes and I gave up. It’s been a total of one hour on hold now.

Who’s got time for that?

Tuesday, March 31

Okay, now we’re getting somewhere. But at the same time, we’re not.

To compensate for the surge in call volume, WF deployed a notification to let callers know just how screwed they are.

Yesterday I called in the morning, so today I pushed it back a couple of hours. Mere seconds into the recorded message, I hear a grim statistic: 455(!) callers are ahead of me, and the wait time is 45 minutes.

Now, I’ll go out on a limb here and say that this behemoth of a bank has the funding to hire staff. But that equates to cutting into those precious profits, sooo… nope.

Overall Service: 1/5

The lack of a chat option is a disappointment, as is no mention of the special hotline on the Contact Us page — that’s a simple addition.

The entire weekend has come and gone, and I’ve yet to make contact with the proper dept. I guess the next step is to call the dreaded number and bring abundant patience.

Deferral Leniency: 0/5

Although I determined options from the other three banks within the same evening, after days of trying to contact WF, I still have no idea where I stand.

Are they hoping most customers’ lack of patience will force payments? What happens if I miss my next payment? Does anyone even know?

Total Score: 1/10

😫 Bank of America

BoA made the deferral process the easiest. I missed the online option the first time around, and since they, too, lacked a chat option, I called the 800 number.

Unlike Wells Fargo, BoA got right to the point and explained deferral options at the beginning of their recorded message. After less than a minute on the phone, automation directed me toward the online solution.

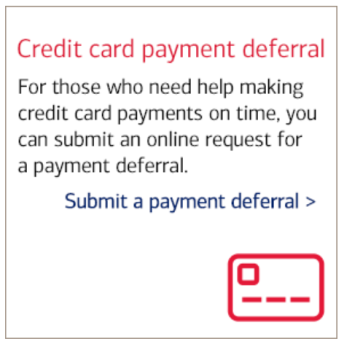

Yes, BoA is letting personal and small business customers slide for 2–3 months. Unfortunately, however, nobody can expect one cent of financial assistance.

“Interest charges or applicable fees will continue to accrue and be added to your balance.”

Those who get rich on the backs of commoners will offer little help in times of desperation. Sure, BoA is hitting the pause button, but the light at the end of our viral tunnel is nothing more than a larger balance.

Overall Service: 4/5

Finding deferral information is the easy part. Even if you don’t see it at first, BoA’s messaging will get you there eventually. Kudos for making an effort, but lack of chat knocks them down a point.

Deferral Leniency: 3/5

Sure, BoA is throwing customers a bone. But continuing to pile on finance charges is another story. BoA is now in the same boat as Wells Fargo — the S.S. Find Another Bank.

Total Score: 7/10

😐 Citibank

BoA and WF clearly don’t stop to consider their customers when making business decisions. And those attitudes are bound to come around and bite them on the backside. But with Citi, we’re starting to make a little progress.

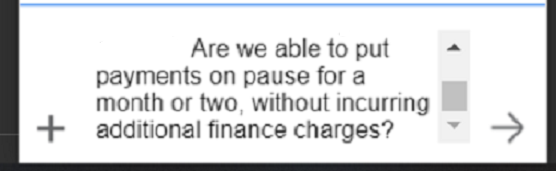

Live-chat screenshots

For holders of specific cards, Citibank already offers deferral options. Notice how I specifically asked about finance charges, and that query went unmentioned.

Overall Service: 4/5

Chat service is great, but Citi wasn’t prepared to handle the volume. After initiating a chat, three hours elapsed before a rep made contact. Compared to Wells Fargo, especially while tying up a phone line, that’s not too long.

Deferral Leniency: 3/5

Although late fees don’t exist, Citi’s cardholder rates are nonetheless predatory. Penalties and interest are separate forms of charges. Citi’s only alleviating one, but by default.

Total Score: 7/10

👍 American Express

Remember that case of entrepreneurial fraud I told you about earlier? Well, Amex came through for me on that one. While WF told me to get bent, Amex reversed the charges and gave me a clean slate.

That event was more than a decade ago, but I still remember. It’s no surprise, then, that Amex won the four-team contest of customer assistance during financial turmoil.

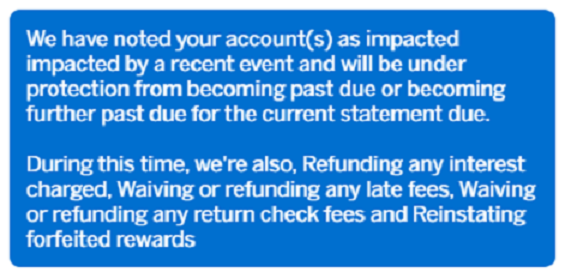

“We’re reversing any interest charged.”

Though I’d rather not carry a balance, it’s good to know that Amex is somewhat on our side.

Overall Service: 5/5

The Amex chat service was outstanding. I received a near-immediate response, with co were answered promptly. It’s almost as if — gasp! — one of these banks has prepared for the impending influx of customer queries.

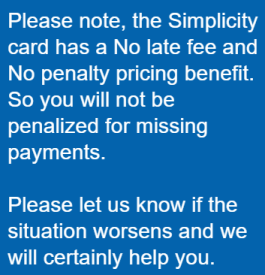

Deferral Leniency: 4/5

Fantastic to see that at least one bank is willing to waive interest charges. That said, it’s only for one month, which is the shortest deferral period among the four banks. We’ll have to wait and see what the next statement brings.

Total Score: 9/10

Wrapping Up

I wouldn’t live up to my profile if I didn’t mention the ability of blockchain tech and cryptoassets to provide a smoother, far more transparent banking system.

And that’s precisely why the likes of Sweden, China, the U.S., and even Facebook are rushing to mint digital currencies. It’s only a matter of time before one of these behemoths succeeds.

But unless the infrastructure is in place, like blockchain itself, it’s still too early. Like the Internet before it, the world’s not yet ready for distributed ledgers. The good news is that we’re making giant strides towards acceptance.

Companies like RedFOX Labs are using emerging tech to practice digital inclusion — providing the means for all smartphone-connected citizens to enter the digital economy. And now that everybody's sheltering in place, online gaming and shopping (think food delivery) are rapidly expanding.

Uniswap is vastly simplifying the DeFi space, and despite its relative failure as a method of payment, Bitcoin’s fixed supply means it operates exactly unlike the Fed’s dangerous, free-for-all, multi-trillion-dollar cash injections.

However, because we still rely on banks and their fiat onramps and offramps, digital assets and central banking have a symbiotic relationship. In other words, I’m not yet paying my mortgage or everyday bills with cryptocurrencies.

But one day, maybe sooner than we think, we’ll all use crypto for everything. Whether or not central banks are still in the equation remains to be seen.

Before we get there, we’ve got to unite and punch COVID-19 right in the mouth. I’m sick of it, and you’re tired of it — the entire planet is so over hearing about it and dealing with the repercussions.

We’re experiencing the most freakish times in recent history, but our days will eventually stabilize. And when peace returns, people remember those willing to lend a helping hand and others who turned their backs.

Our lives may never be the same, and unforeseen shakeups are bound to arise. But when the dust settles, my goal — until blockchain helps run the global economy — is to drop three banks from my list of contacts.

Keep it clean out there!

~BlockchainAuthor