Episode 2 was a great one. We talked about some 401k stories, a bit about the history of the different retirement plans over the past 100 years, and how the 401k has actually worked out (or not) for people since the ERISA act in the 1970s.

Listen to the show on your favorite podcast network:

Google Podcasts

Spotify

Anchor. FM

Links and images from the chat

https://www.businessinsider.com/personal-finance/average-401k-balance?op=1#average-401(k)-balance-by-income-level

https://en.wikipedia.org/wiki/Parkinson%27s_law

Transcript

Episode 2 - Are 401ks a Scam?

[00:00:00] Everybody it is Monday three o'clock and that means it's time for tax Sherpa stories. So welcome to the show. We've got a few people in the live audience. Oh, Shane just dropped in. Everybody blamed Shane. That's sorry. Ongoing. Our ongoing joke here. We got swoop. We got crim. We got inertia. We got scaredy-cat.

We've got our rundown or producer. W, you know, a dictator of all things that must be waves. And you know, there is, Oh, Shane's here since Ron is the lane, right. $1 million security cat says the $1 million stories was the highlight. No one needs to come back. Yeah, that is true. So that's talking about last week's episode, that's my own personal story of how I owed them a million dollars to the IRS and then ended up paying down a bit.

And that's kind of how I got into the whole tax world over a decade ago. So that's, that's my, my gig. I help people with their taxes over the past decade ish, I've done probably 50,000 tax returns and I've seen all kinds of stories, all kinds of [00:01:00] events, all kinds of everything in that time. And this show is about, you know, some of those stories and some of the lessons that I've learned current events, things that are going on in the markets related to taxes, finance.

All that kind of stuff. The political climate of everything, you know we have Biden as our new president and he has promised to raise taxes in lots of different. So the, and monitor that situation, how it goes overtime. But you can join us on discord live. You can interact, or you can watch on a P waves.com you can watch on vim. tv.

I don't think it's, data are still working run done. I'm not will Joe Biden raise taxes on everyone? Well, he wants to, that's what he says. We'll see if it actually happens or not. Hm. And you know, if you're catching the replay, you know, we're on the podcast networks, we're on YouTube and you can of course catch the updates there, but it's more fun in person.

So I recommend everybody jumping to the audience and, you know, we can go back and forth everything. So [00:02:00] that is all the interesting stuff. Oh, VIM does work. Plus swaves data is live. I didn't know that command existed. Let's waves give us all the links for MSP waves of M and data. Okay. Very cool. All right.

So yesterday or yesterday, last week, you know, I, I told a little bit about that. My story, and, you know, my million dollars owed to the IRS, I then went into one of the pre-submitted questions on the Biden proposed tax change. So that took up most of the time last, and I got a couple of complaints that it didn't leave enough time for.

Or the, or the Q and a, the back and forth inside the channel. But, you know, the Biden thing was a question from a listener. So that was relevant. And because it was so timely because Biden was about to be sworn in I thought we would go for it. So I think that counts, but. I've heard your complaints and, and I'm leaving more time for the [00:03:00] Q and an after my little story here.

So the question is what do you think about 401ks? This is going to be the topic of, my storytime today, because already, you know, so it is January 25th, 2021. The IRS has announced that they're opening for filing on February 12th, which is late. However, we're already doing tax returns and we're preparing them for submission on Friday, every 12th.

What's a 401k. That's a great question. We will, we'll get into that. So 401k or four, three B or four 57, or an IRA or whatever are all different accounts that you can set up to do for income. And then you take a tax deduction today. So it's, you know, Back in, I think it was 1973. It might've been 74, but there was a lockout Arista passed.

And this created what we all know now as retirement plans. So back before [00:04:00] Orissa, there was social security, it started in the, you know, in FDRs new deal. And there was your company pension if you were lucky enough to be with a corporation that had one. So in the seventies, they come up with this new thing, they come up with a Rissa, and I have a 401k with rental properties instead of stocks.

Yes, you can, but it takes some work. So they pass this law called ERISA and it creates various new code sections in the IRS. And under title 26, a sub-subtitle, a chapter one subs, subchapter D part one, Subpart, a section four Oh one, parentheses K is the law that creates the 401k.

And that's why it's called a 401k. Scaredy-cat says his 401k investing book is 90% done. Let's see what good info I can steal from Neil to add. All right. Let's this is all good. So so yeah, the 401k, the four Oh three B the four 57, these are all referring to the code sections in the, in the law.

So, that's where they get their names and what they are tax deferrals. So basic idea is that. You have a job, you have earned income, you then decide, I'm gonna save for rainy day. I'm going to not take some income today out of my salary, I'm going to defer it.

And therefore I don't have to pay income taxes today. Little known fact When you defer money into a 401k, it is true. You do not pay income taxes on it in that year. So you get a deduction against that, but you are paying payroll taxes on it. You are paying social security and Medicare tax on it.

So you're still paying your half of the 15.3% for payroll tax. Just something to be aware of the D the general thesis of the whole thing is, so you defer income today. You put it aside into a 401k qualified plan, and then you invest it for the [00:06:00] longterm. And the idea is that over many, many years over a working lifetime, that money adds up and invests in compounds and all that kind of stuff.

And then you end up at the end of your working career with a whole pile of money. So and then you can start to withdraw that. And now, because you got a tax deduction, when you put the money in when you take the money out, you get a tax hit, so you have to pay income taxes on it, just like it was a regular job or it was any kind of other ordinary income.

So. If you listen to the talking heads on TV, they will tell you that, well, generally you're in a lower tax rate when you retire than in your, in your working years. So, you know, the arbitrage over time, that kind of works out. So you do, you do pay taxes, but it's a lower tax rate than the tax rate that you're saving when you put it in.

And that is possible it's by no means a guarantee. Because for one, we don't know what tax rates will be in the future. I think that is, that is very very simplistic to assume that they will be the same or lower. So, if we're not going to get into that so, you're, you're making that bet that you are going to have a lower taxable income and you'll be at a lower tax rate in the future.

Sometimes that's true. Sometimes that's not true. Just depends on your personal situation. And then there is the whole, you know, qualified funds sling. When risk was passed and when they started pitching these two employees, they said, well, there's going to be, what's called the three-legged stool.

Leg one is going to be the social security leg. Two is going to be your pension leg three is going to be this 401k thing. And all three different things are going to be part of your retirement plan. And they are all going to serve a different purpose. So social security is kind of your base level earnings that's tied into the Medicare system.

So you know, if you have 40 qualifying quarters or quarters of coverage then you're qualified for Medicare and you're qualified for the, basically, the bare minimum living standard that social security provides for you. And then you have your company pension, which of course when they pitched this whole thing then this was still a thing.

Pensions are very, very scarce these days, pretty much the only people that still have pensions are local government employees, like firefighters, police, officers, and administrators, that kind of thing. And then you have the 401k or four Oh three B or whatever. So the great switch. And that was perpetrated upon the American people was that companies realize, well, tensions are really expensive and there are huge amounts of liability associated with them.

And if you went through the eighties, so all the pension plan, all that, well, not all, but a lot of them go bust. And a lot of companies that were taking over the so-called hostile takeover or corporate Raider, you know, meme came, comes from pensions. Then, they were broken up or where they were passed over to the pension benefit guarantee corporation, which is, which is a federally sponsored entity and the bottom line is pensions are more or less a thing of the past.

When the companies realize, Hey, we can offer this 401k thing. And then, employees are on their own as far as for the same for retirement. Then we can wash our hands of the whole thing and there's no more liability that we have on an ongoing basis. So like Shane says here my, what does he say here?

I said, my 401k sucks. No employer match. So it's worthless. So employer match, this is. This is the sweet little carrot that they dangled for you where the employer will match a percentage. You know, maybe it's 5%, maybe it's 50%, maybe it's a hundred percent of the amount that you put into the 401k.

And so they'll kick in some money on top of that, which is, okay, great. Bottom line is that money was coming out of money, that they were going to assign towards payroll anyway. So that's kind of one hand versus the other six of one, half a dozen of the other.

But that's kind of what the 401k is. However, that is not what we actually see in practice. And so, as I said, I've done 50,000 some tax returns. And I see a lot of people dealing with our 401ks and the fundamental problem of the 401k is that it doesn't actually retire at all.

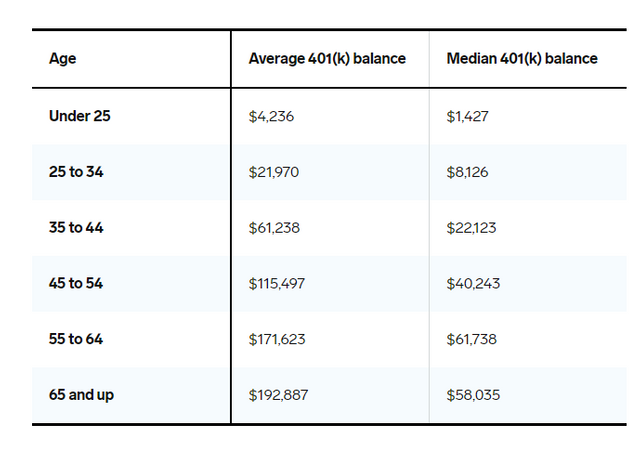

So I went ahead and I went and looked up on Google. There was a study done by Vanguard. These were 2019 numbers. Numbers are slightly dated, but general principles, general trends will apply. And it breaks out all the 401k balances by age by income level, gender, and industry.

So if we look at the 401k by age and again, this is just Vanguard's customers, but think art is the largest mutual fund company for this type of stuff. So there's a pretty good sample size there let's paste that there. So 401k it's got an average balance and a median balance. And the average balance at 65 is at 65 and up category, which is in that retirement age is one 90, two 87 and the median is 58 Oh 35.

So the average is four times larger than the medium, which is, which just means that there are a relatively few number of people that have a huge amount in their 401k. Right. And everybody else, as, you know, 58,000, basically. So problem number one with the 401k is that the people just don't put enough into it.

So, you know, Bye-bye. This idea, of deferring income and investing for your retirement, you have to do enough so that you can actually it higher because the goal, all of this retirement income is to provide some level of the living standard in retirement. And there've been lots of studies over us market it's and, you know, like the Trinity study is the most famous one where they looked at what's called the safe withdrawal rate and.

More or less 4% is the number. And if you go to any financial planner and they'll say, you know, you save up a nest egg and if you withdraw 4%, let's say it gets in the back and all that kind of stuff, then it will last you through retirement. And the definition of how they did things in the Trinity study leaves a little bit to be desired, I think.

But the bottom line is you'd still have at least a dollar at the end of a 30-year time horizon. Okay. Great. In fact, the author of the fraternity study now says that maybe 4.5 is a better number because of the increased returns that we've seen over the past couple of decades. But whatever number is 4.4%, 4.5%.

If you have $61,000 in your 401k, in the 55 to 64 group, what does that mean? So let's, let's say 61, seven 38. Times 4% is $2,469 a year. So that's not going to do it. I mean, it just isn't that is one month of income may be on top of your social security. And like we said, the pensions are gone for the vast majority of people.

So that is that is no longer a source of income. So what are these people to do? So problem number one is, is that it's just, it's not enough. You know, well, there are, you know, anytime the IRS gives you a break on it, right? So there are limits to how much you can put into a 401k.

Or right now it's a 19,500 for 2021. And I believe that it changes a little bit every year. And then, you know, theoretically, a match, an employer could match you up to $57,000. A year, but you know, that that is very rarely done and that's pretty much a retirement planning strategy for people who own their own businesses.

They can, they can have huge employer matches on top of the employee contributions, but if you're a rank and file kind of employee in a company you don't own then the match he's going to be if there is one is going to be in the low percentage points. So you're not going to be getting some kind of sweet executive pay package there.

So, one is just not enough. The second problem with 401ks is that very few of them, at least in my practice and what I've seen actually go to retirement. So things happen throughout a working lifetime. People get sick. People are unemployed people astronauts for any number of reasons.

And. there is there's a penalty. If you take your money out when you're younger than 59 and a half and C3 is saying Ross Jor is great and everything, but so different between Roth and traditional Roth. You, you take the tax hit upfront. Then when you take the money out, it's tax-free, you still have penalties.

If you take it out under a 59 and a half, and contributions, you can take out, you know, after five years and all that kind of stuff. Yeah, my green screen does, my lighting is a little weird today. I dunno why, but it's making my face a little bit transparent. So so yeah, I mean the so even with the penalties, with all the strings and everything, the, I would say the majority of people actually don't let their money sit until retirement.

So they're not viewing it as a retirement savings vehicle. They're viewing it as just a savings vehicle. And something happens. They come along as I said, let's lose a job, right? They, they tap that money and they want to buy a new house, have that money. And then the balance just is never left alone to do that, that growth plan over a working lifetime.

It says I stopped contributing to the 401k and I'm now buying dividend stocks with payouts. Sure. That'll work just fine. Swoop says what if all your money comes from delivering groceries, drugs, and NFT art sales. Well, those are all like, self-employment kind of things.

So you could say up your own retirement plan if you want it to. But, but fundamentally the retirement savings cool. Whether it's traditional, whether it's Roth, whether it's 401k, whether it's three B, or whether it's an IRA, it doesn't matter because not enough money is being put into it and it's not being left alone.

So the people that 401ks do work for are people who make a pretty high salary, so they can actually afford to put in that maximum contribution. And they have enough Slack in their financial lives where they don't have to then well that money out over their working lifetime. So for those people, it works great.

And, you know, you can build up millions of dollars of value over that working lifetime. Whether it's better to take the money now and invest in a taxable account or a tax-deferred account. That's really not the point that I'm trying to hear. It's just that the because, you know, depending on market things and what you do and fees internal to the 401k, it may or may not actually work out in Texas efficient way, but when you, when you pull that money out and you're paying penalties, Then you are definitely just taking an extra tax on the money that you would've gotten anyways.

With the coronavirus pandemic, Congress passed the cares act, and inside the cares, the act was an interesting little feature where they allowed people to pull out a hundred thousand dollars of their, of their qualified plan balances like 401ks and not pay any of them the penalties. Still pay income tax on it cause it's still income, but you don't pay the 10% additional penalty.

And in fact, on the tax forms, it's form 53, 29 there's a little line that says, you know, if you, one of these qualified purposes allows you to exempt the penalties. So in normal years, it's things like paying for higher education. One of my favorites is that if you owe the IRS money, they will allow you to pull money out of your 401k and not pay the penalty to pay the IRS.

So like, if you have a lien or something so buying your first house if I think it's only for IRAs, but you can pull out 10,000 there, but now we have a coronavirus line. You can pull up a hundred thousand. Additionally, you can also spread it out over three years.

Now, this is the same disaster mechanics that they've put into place in previous years with hurricanes and things. Massive floods and that sort of thing, same three-year distribution and same hundred thousand. But this year for 2020, everybody's qualified because everybody's affected by the coronavirus pandemic shut down and people lost their jobs.

And obviously, we've all seen the craziness with the unemployment numbers, all that sort of stuff. So as a result, We're seeing already, you know, even though we're only three weeks into to actually filing stuff or two weeks, I don't know whatever it is. I'm seeing already a lot and lots of people hitting their 401ks and lots of people who are hitting their 401ks, even though they didn't lose their jobs.

I saw one client, so, you know, all names are false because protect identity. But so one client pulled out she actually retired in March, I guess she was at that age and things were kind of going to hell with the economy anyways.

So she's like, okay, I'm just hanging up. And so this person makes made on salary, had a decent salary, made, I think like $120,000 a year. And work January to March made whatever the proportion of that is 40,000, something like that, and then pulls out 180,000 of the 401k, which has all of it.

So this is, this is like the third scenario that I see happen is like of the people who managed to save up a little, but inside their 401k, once they hit retirement, they just cash it all out. And it's gone in one, two years anyway. So, you know, again, it's just, this whole system just doesn't work for the vast majority of the people in these circumstances.

So, cash is out the 401k and, you know, does whatever with it. It doesn't even matter what's done with it. The point is that there's no more money. I did a couple of tax returns over the weekend of a couple of guy gay couples. I'll say Bob and Bob and, and then you know, they, they are both still employed.

You know, didn't lose her job, didn't go on unemployment or anything. They worked for a pretty stable place and, you know, between the two of them, they cashed out. A whole mess of 401k balances and yeah, they're able to not pay the penalties because of the coronavirus, but still, you know, that's, that's money that they spent it's the same thing over and over and over again.

And these are, this is kind of the idea behind the tax stories is like, these are stories that. I ran into just over and over and over again. And so from my 50,000 tax returns or so that I've done, my official opinion is that 401k is for three, for 50 sevens IRAs, all the rest of it work for a very small minority of people and those people who earned enough to, to make the whole system work and are disciplined enough to leave it alone.

Because just because you aren't enough, does not mean you were actually able to leave it alone. So, so that is kind of like my, my quick version of, of the 401k story. Now, there were some questions earlier, can you buy real estate? Can you do all this stuff? You can it depends on theon the setup of the plan.

And usually, if you're talking to real estate and things then you're talking about a self-administered plan. Or pretty much you have to own your own business to do that. You're not going to be working at home at a mainstream kind of company that offers a 401k and be able to do that.

99.999% of those types of plans. You're, you're restricted to a family of funds kind of offering it might be Vanguard. It might be fidelity. It might be whoever, but they're going to say, here are the different things you can pick from, and by and large, they're just broad market funds. There might be an international fund.

There might be a growth fund. There might be some this, that, and the other fund. But basically, it's some brokerage is, has gotten a contract with your employer, and then you get to pick from that brokerage fee, Emily, a list of investment options. Then others there's plenty had been written about those, those administrators and whether or not the fees that they're charging internal to that is legitimate or not.

But you know, That's a whole other discussion even the backing, all that, it's just, it's hard to make the math work for you. If you don't make just a very high salary and if you don't leave it alone, so. My preference is to save in non-qualified plans and yes, you do pay taxes along the way, but then you have more control and you don't have penalties and you don't have to worry about any of this kind of stuff.

I can't afford one. KB Bitcoin pegged. That's an interesting question, inertia. So if you had a solo 401k, or like you own your own business and, and you set it up that way you could. You know, I guess you would have to buy like grayscale trust or something that so yeah. I've never seen one do that, but I don't see why not.

C3 says, have you ever seen anyone cashing out to buying an online business? Absolutely. People, people cash out 401ks for, for any kind of money purpose. I will say that if you have a whole pile of money in a 401k, like in a corporate, a large employer kind of plan one thing that you can often do, and it depends on your particular plan administrator.

You, you can borrow from that. So if you see an investment opportunity one option is to borrow against that. Usually, they'll go 50%. And then they'll take payments out of your paycheck to repay it, but you know, if you have a good cash loan opportunity, then it does make some kind of sense to do that.

Ron Dunn is asking, should I liquidate my 401k and buy? I bet. I don't give investment advice, I can't say you should, or you shouldn't, at any way, it's a trick question cause you don't have a 401k, but still, it's a legitimate question. And there have been if you read on Reddit and things in the stock in the stock trading kind of.

Sections. There are lots of people who, over the years, it's like, Oh, well, I cashed out my 401k and, and bought Apple or you know, more recently about Bitcoin and those kinds of things. So know if you're right, then it works out if you're wrong, it doesn't. So, standard risk tolerance and being aware of the financial hit that you take when you cash out.

I had one client co last year, the year before, and he cashed out a, he had a large 401k, you know, he's one of these disciplined guys. He had, you know, several hundred thousand dollars in there and he cashed out, I think. And he put it into insurance vehicles as a place to store capital.

And, you know, I am personally, I'm a fan of the insured vehicle. I am not such a fan. And if cashing on a 401k to do it, just because of the taxes and penalties involved, But you know, he was he thought that it was worth it because he thought the market was very toppy anyways and that things were going to go down and you'd be better off saving that, saving that money and taking the tax hit.

As it turns out the market did crash in March. We had a nice little drop with the COVID issues. And since then it's back up to record highs. So I don't know, I haven't talked to him yet this year, so I don't know how it feels about all that, but you know, if you're right, you're right.

And if you're not, you're not, it's, it all just depends on, on your viewpoint of things. But just know that when you enter into a qualified plan of any particular type. Then you have all these strings attached, so you can do with that kind of what you will, but the main point here is that it's just, it's just hard to make the numbers work.

So if it's a matter of doing that versus nothing. Okay, good. Go ahead and do that. You would in a way that you can let the system work for you, and that means not touching it. So you can't just save in a 401k or a fourth review or whatever you have to also have, you know, savings that are available to you and not for retirement.

So you need those emergency funds. If you listened to the Dave Ramsey's and the Susan Romans and whatnot, they'll tell you three to six months. I think that's a good rule. You know, I know I have. Some very conservative clients who like to go out for a year and I have a couple of even do two years.

But again, it's, it's hard to build up to that just because of the amount of money compared to the income that people spend. So the ratios I've been I've been flirting with this idea lately about so I'm profit first professional, you know, I coach businesses on how to structure their cash flows to maintain their profits.

And I've been thinking about this in the personal finance world lately I think implementing profit first or your personal life is actually a good way to go. And I'll be developing that idea more over time. But this is that book. If anybody's curious, it's called profit first.

It's, it's a pretty short read and I highly, recommend it for anybody who's in any kind of business. But that's, that's a little bit beyond the topic of today. So yeah. Yeah. We are at the halfway mark, which means that that is Storytime. Let's see, I got some people hitting me on Slack. Ah, we've got Chuck.

We've got Matt. Mike Mike is having trouble, I guess. Oh, I guess this Matt here is that matter for there, right? So yeah, now it's just a time for Q and a kind of stuff. And this is. This is the potentially unrecorded portion. So up till now, you know, my little rant here about 401ks, all been recorded, all going into the replays.

So if you have questions that aren't or you don't want me to record it, just let me know and I'll, I'll hit the stop record and, and we'll, we'll talk, you know, off the air and it's the online business buying questions. Yeah, I figured that was him. So let's see, Jim says no one should kick listeners until after my show is to inflate my numbers.

I guess there were some, some shenanigans here that Ron Don was, was picking scaredy-cat out. And I was scared of cats trying to get rolling in here. Yeah, Roland's here, but he's not listening. He's got defin on So what are the biggest mistakes you see with the 401k? So, yeah, the biggest mistakes with the 401k are one is, well, okay.

This is going to get a little bit tactical. So. If you have a very limited offering in your 401k and you have to dive into the fees that are being charged because there are administration fees of the 401k, which is going to eat into some of your return. There's also going to be mutual fund fees of a billion different GYNs inside of whatever ones you pick.

So if you have it, if for whatever reason your employer has a plan, that's just has a very high fee load. You're almost always better off. You know, not doing the 401k and investing into, you know, Vanguard or something on your own. So that's, that's issue number one, and that's, that's not even a mistake, but that's like a wall street.

Gotcha. That, that they try to perpetrate upon people. Cause it's just, it's a fee Bonanza the whole 401k thing, because they get, you know, automatic deposits every two weeks or twice a month or whatever your pay cycle is. And then it automatically goes into their stuff. You know, into their assets and our management and, and the charge all their fees.

So it is just billions and billions of dollars that is being siphoned out of people's retirement savings into, you know, wall street administrators. So that's issue number one issue number two biggest mistake. And this is, this is a mistake is, is not putting enough into it. So I touched on this a little bit earlier, but.

You know, you gotta figure the richest man in Babylon, John's been personal finance stuff for a hundred plus years. It talks about, well, you know you know, pay yourself not less than one 10th of all you make. So they're talking about a 10% savings rate. That's not enough. I've run the numbers many, many times.

And, you know, with, with the historical, you know historical patterns that we've seen in the markets and the taxes that you pay, whether you pay them today or whether you pay him when you withdraw. 10% is just not enough because you also have to factor in the fact that, you know, there's inflation in salary.

So if you read a lot of personal finance stuff, you'll see that it's like, Oh, you know, if you make $50,000 a year and you best 10% and you do this and you do that it's. It's just not true because you know, if you look back 40 years ago was 1980, right? Salaries were not, you know, median salary right now is like $55,000 or something.

Salaries back then were a third as much. And that's just because of the inflationary, monetary system that we have over time. So if you're talking about 10% of a number, that's one third as much. Then, you know, you're talking about a very, very small number and yes, there is compound growth, but it's not enough to overcome all that.

So from, from my analysis, it's gotta be 20% 20% savings it has to be done. And that, that can be in qualified plans. It can be Allstate qualified plans. It can be a mixture. It's just, there has to be enough money working for you to make retirement possible. Because, you know, if you look at social security statistics, basically 95% of people rely on social security for the vast majority of their, of their living standard in retirement.

And you know, another 3% are doing okay, you know and then the other, the top one or 2% are doing just fine. They don't need any help from the government. But the 95% of people are completely reliant on the government system and the government system. If you run the numbers there, as far as like if you imagine social security is an investment, it's not a, but if you imagine it was.

Then you would calculate the cash flows over time. So I put in so such and such over my working lifetime, I guess, such and such in my retirement. Then, if you take that model and you calculate the return on your investment, it's less than 1%. So it's pretty much the worst thing you could do from an investment standpoint.

But that's, you know, it's, it's this forced kind of system that, that is put on to people. And as it turns out, 95% of people need that because they don't have anything else. To, to go on You know so, so C3 saying, but when you retire, you should have the same level of expenses. Your house should be paid off furniture, et cetera.

That's the theory. Then you will hear this again and again, that you have fewer expenses in retirement. I just don't find that to be true. You know, with all my clients, all the thousands of people I talked to every year, you know, they are spending plenty of money in retirement. You know, maybe their house has paid off, but more often than not, they're moving every seven years on average, just like everybody else.

And they have mortgages. You know, maybe the kids are out of the house and, and they are not such a financial drain, but you know, we've seen the whole, you know, boomerang generation with the millennials and, and the zoomers too, where some crazy number, like half of them are living with their parents after college up until their thirties.

The theory that you'll, your expenses will be lower in retirement. I've just hit. In, in practical experience, I've not found it to be true. And the so tied in with that, with the biggest mistakes is that, you know, people we'll pull out money from a 401k at the drop of a hat, you know, penalties be damned.

So you know, yeah. And there are even those exclusions, there is, you know, $10,000 for for your first house or you know, higher education purposes, those kinds of things. And so even the IRS says, okay, those are legitimate you know, purposes to access your, your qualified money. But, you know, it's, that doesn't mean that the math has necessarily changed because in order for long-term investing to work, it has to sit there for the longterm and compound over time.

So if the, if you're constantly pulling that money well, you know, for whatever reason doesn't matter, what the reason is, then it never has that chance to grow. Those I'd say are the biggest mistakes. And Frankie is asking, do you offer renounced services? Do you mean renouncing your citizenship if that's what you mean?

No. I couldn't help you prepare exit taxes if you want. Where if you are leaving your citizenship and you're, you're trying to say I'm no longer a us taxpayer. If your, if your income and or net worth are higher enough, then you have to pay an exit tax, which is basically saying, okay, I want you to got, we're going to take a percentage on your way.

But no, I don't know. I don't offer any kind of immigration or. Immigration and services. So should your money be sunk in-home or BTC? You know, sinking money in your house is always, is always a contentious thing. So there's the math answer. And then there's the emotional answer. And I have this conversation with clients frequently.

So the math answer says that you have a mortgage rate in your house. So, you know, whatever it is and rates are at historic lows right now, talking to people, getting, you know, two-point something percent mortgages over the past year, which is just insanity. It's almost free. So So there, the math says that if you can, you can use that money and put it to work for you and get a return that's higher than whatever you're paying in your mortgage.

Then you come out ahead in that now one caveat with that is that you have to risk adjust those returns. So, you know, if you're putting it all in Bitcoin, I mean, if Bitcoin does well, then then you know, Great. If it does poorly, then you're sunk. So Natasha says, rich dad, poor dad, answer by assets, not liabilities.

That is true. And the rich dad, poor dad version of assets is assets are cashflow positive. So if so, if you want to if you want to refinance your house or finance your house in the first place and use that money and then invest in whether it's Bitcoin or whether it's stocks or whether it's real estate or whatever that's all fine.

And as long as, as long as the returns over on the investment side, exceed the returns, on the cost side, then you're positive now. And then you have to take into account, the variations of those returns and make sure you don't get yourself upside down in the future market conditions.

But all that said that that's what the math says. So then there's the emotional side of things where some people just don't want to owe money on where they live. And it's, it's just, you know, it's a, it's a safety thing where it's like if everything were to go to hell and my job was to blow up and there's another pandemic, there's, you know, whatever you know what, we're China, whatever's on the horizon.

Then I know at least I don't have to pay, you know, Towards my house. Yeah. I mean, it's still, we're going to have property taxes are struggling and utilities, but you know, that's generally a small fraction of whatever a mortgage payment is. So, you know, It's really, it's really a personal preference thing.

And you know, interest was fundamentally right by assets, not liabilities. So you know, if you buy enough cash flowing assets, it kind of doesn't matter. And you can, you can do and live, you know, whatever you want. And, you know, that's, that's the phase I'm in. I'm trying to build up as much cash.

Cashflow positive kind of assets as possible. And so like I've got this real estate company with scaredy-cat and with Agra and we have proof of home and, you know, we have some idle funds and we were talking just today about putting that those idle funds to work, you know, while we're waiting on, on some things to go on internal to the integral business.

So yeah, sure. Should you be, should your money be sunk in-home or BTC? Well, it's a false dichotomy, but really fundamentally it's up to you. And it's an emotional decision rather than a, a strictly rational one there she says it's so simple. It is simple. It's just not easy. It's very simple to buy things that pay you the end.

It's like, you know, if you had to write personal finance on one page, that's it buy things, they pay you. And then over time, those payments add up to enough to pay for all the rest of your stuff. But it's just not easy because, you know, there's that whole Parkinson's law thing. So if you guys don't know there was a behaviorist economy, behavioral economist, even though that term didn't exist at the time in England Northcote Parkinson, and he, I think he was in the, in the British public service stuff.

And he found it that you know, if you give somebody a week to do something, it'll take a week. If you give them three months, it'll take three months. And from this, he kind of generalized out that you know, things take the amount of time or the number of resources that are, that they are given.

And you know, so that applies to pretty much all of human nature where, you know, if, if you make a certain salary then you tend to spend that certain salary plus maybe a little bit more. Cause a lot of times the savings rate is actually negative for people. So those things, you'reying the proof of stake coins are probably better than I am not saying that at all.

For a long-term investment. So yeah. Proof of stake coins is attractive. The hive is very attractive in the, in the return on assets kind of viewpoint because, you know, you can make 23, 25% on, on your stake coins, but then there's the whole market value of those coins, which you know, I'm, you know, I'm perfectly guilty of.

I put way too much money back into steam in 2017 or 18, whatever it was. And I just, even though the internal rate of return in steam terms, I made great money, you know, I mean, 30% a year or something like that. But the market value of that went from a dollar 65 when I started getting in or $2, something like that down to, you know, 13 cents.

So not, not a good use of my funds. So you know, you have to take it away, count the risks associated with any particular investment and just things that the goldfish bowl theory I'm not familiar with that term, actually see old fish bowl theory. See what the old Google has to say there. Einstein in the goldfish bowl, reman Ramani in geometry.

I don't think that's thank philosophy. Ah, here we go. Here's me somewhat proven that a goldfish will grow to suit the size of its tank. That if you increase the size of the thing, the goldfish will continue to grow. Some goldfish weighed up to 90 pounds and as much as three feet long, conversely, if you keep a goldfish in a small tank will stop growing or dive, and this is analogized to humans.

So yeah, it's, it's similar. But this, so, you know, if you look at Parkinson's law, You'll come up with plenty of results. I'm sure I've even has a Wikipedia dropped us in the chat Parkinson's law or the pursuit of progress by C Northcote. Parkinson. Yeah. So, it's just working expands. To fill the time available for its completion.

So yeah, the. A particular application he was looking at was actually time spent to complete a job. But then since then it's been, you know, like I said, generalized out to everything where, you know, just people just take up the resources that they can. And if they don't have additional resources they make do with what they have, but if they have more, they'll continue to do other things.

And I think, I think most people can and kind of feel the truth of this in whether it's their own lives or in, in the Things that they've seen in people that they know, you know, it's just, I reminded of this guy. So when I was in college, I lived with a friend of mine. We had an apartment off-campus and this was like a senior year or something.

And my roommate had a buddy who was down on his luck and I don't know the full backstory, but he, you know, he ended up staying on our couch for a few weeks. Like three or four weeks, it was awhile. And you know, I said, okay, [00:43:00] fine. You know, and you know, he was struggling and he was having this and that problem, so sure enough, you know, lend a helping hand or whatever.

And I come to find out that's he gets a job with a law firm as a filing clerk or so. Great. You know, he'll, he's got this opportunity. I'll start making some money. There'll be off on his own. Fantastic. Right. So the first day of work rolls around and he doesn't go in and, and I remember talking to him and I was like, what, what are you doing?

You know, why, why didn't you go to work? And I forget exactly what he said, but basically it came down to, Oh, you know, he wasn't feeling it. You know, he didn't feel like going in or. You're tired or something like that. And I just lost it. So clearly I had made too many resources available to this guy and he was too comfortable.

So at that point, I talked to my roommate and I was like, this, the guy's got to go, and if he's not going to, if he's not going to take advantage of the resources that we were providing for him, then. There's no helping them. And there's just, this happens in the movie industry to limited resources, gets you a new hope unlimited resources gets you the force awakens that's, that's harsh, that's harsh, but but true solos asking what is this proof of home project you were working on?

So that is a company that we have. It's an investment, a company that's only available to accredited investors. And basically we buy single-family houses, rent them out and enjoy the cashflow. That's the basic basic idea. Yeah, pretty star Wars nerds, you know, that, that hurts. But one of my best friends, his brother actually for Lucas or I guess he used to work for Lucas, Lucas sold, but the nose is like the nerdiest Star Wars Northern.

You could think of good times. In fact, when COVID ends, we will do our, our marathon episode watching of all-star Wars group delinquent, Texas, actually. No so this is random point, but a lot of people think that tax sales are usually [00:45:00] related to income taxes. They are not. They're usually related to your property taxes.

You'll guy on the couch. You killed my dog. So, so yeah. I have done the whole tax sale thing, tax liens, and all that kind of stuff. It can be pretty lucrative, but no, these are just regular, you know, market deals that are just, you know, attractively priced for rentals. No, just going back to what nurses said about about, you know, rich dad, poor dad had buy assets, you know, so if you're willing, if you're looking for a decent return from a rental there's, there's hundreds of markets across the country there are.

Thousands hundreds of thousands, millions of homes that are decent deals. And, you know, we'll, we'll cashflow nicely as long as you buy. Right? Right. And you know, are careful with your, with your tenants. No property management is as everything when it comes to real estate. But yeah, I mean, there, there are assets to be bought.

The great thing about real estate for buying assets is that it's a pre-packaged business for you. You know, [00:46:00] each property is a each property is its own is its own little mini business, but because it has very relatively few moving parts and you know, your marketing is, is pretty straightforward and your, your channels of sales are pretty straightforward.

It's. It, it, it works for a lot of people, whereas, you know, investing in single stocks and things can be very difficult to come out ahead on. And scaredy-cat yeah, I was just talking about some cash flow markets, good cash on cash. Turn zero appreciation. Yeah. I mean the particular market that that scarcity Kat and I were talking about I am not such a fan of because it has a declining population, but You know, and that's the probably still cashflow nicely.

I just got off the phone with the client. Who's investing in upstate New York and is getting, you know, 30% to 50% cash on cash return. This is just insanity, but you know, he's doing it. And solos asking, have you looked at doing Airbnbs or would you rather have long-term tenants? [00:47:00] So yeah, Airbnb is, are, are pretty attractive.

You know, I kind of thought they would die with the whole COVID thing, but they're doing just fine in a lot of markets. You got to look at your regulatory environment and see if they're subject to lockdowns and things. But assuming that you're not Airbnb is, are, can be killer seeing that you're trading with Airbnb use.

Yes, you do get higher profits, but the expense is the much, much higher management costs. And whether that's in time or money or both. Depends on how you set it up. But yeah, so security cats says basically owning a hotel fun fact about Airbnb that nobody does, right. When it comes to taxes, is that if your average day is less than seven days, it's actually ordinary income and not passive income.

So it's a C versus an E one, which is again, nobody does it. Right. But you know, you should at least be aware that there is potential tax out there. I gotta find a good cleaning service. Yeah. The cleaning service has not, is not the big deal. I mean, there's no in cleaning services. It's, it's the management it's the it's the listings and the communicating with the I don't know if you want to call them tenants. But the renters and dealing with that whole thing and, you know, doing the marketing and all at stuff. So like long-term rental, you know, you advertise, hopefully, no more than once a year. And ideally once every, you know, three to four to five years, So it's a whole different thing.

Is the growing rate 10% for management? Yeah, for long-term rentals, 10% is, is kind of a good average. It could be 8% could be 12%, but yeah, if you're talking about Airbnb rentals, then no, it's 40% is what people are charging. Scaredy cat here says his investor buddy here has a 30 Airbnb units and has team managers that are 50 it's a full-time job.

Absolutely. And you've got to treat it like a full-time job. So that is kind of the story when it comes to Airbnb, every me is 20% management. Well, I mean, it depends you know I, I have seen letting places that charge 40 it's sort of like vacation rentals. Well, like if you have a cabin up in the mountains and there's like a little you know, a whole group of cabins and it's run by a particular operator, a lot of times you're gonna be paying 30, 40%.

And obviously, every particular company has its own deal and everyone's different, but it is, it was high. So Yeah. So Lou says K costs a little bit more for Airbnb med, but yeah, it does. But there are more and more companies that are popping up to do that. And yeah, I got to think that if, you know, if the competition increases, then supply will increase in price will go down of management.

But like cat says definitely depends on area and type of property. So so yeah, that's kind of. Thing that's going on here and I did want to get to a couple other questions. Let's see here. I had them all written down, extra explain and who's eligible. That's a much longer question and I have time for right now, cause we've only got about five minutes left.

See, what is a write-off and what can I write off? That's a great question. So these are the questions that I have had people write in ahead of time. What is a write-off? So yeah, it is a question. That question is a whole show, but you know, here's, here's the quick and the super simple version. Our write-off is simply a purchase that you make.

It doesn't even have to be purchased. A write off is a expense for tax purposes. So like we're talking real estate here. One of the great things about real estate is, and the way his tax advantage is with depreciation. So depreciation is writing off a portion on the property over time.

So if you buy a standard residential piece of real estate, the building is written off over 27 and a half years. And the land is not written off at all. Very few people do that correctly. And then the interior contents, depending on what they are, you can do some cost segregation and figure out that, Oh, you know, the, the appliances are five-year property.

And so they wrote off over five years. The building itself is 27 and a half year property. You know, this and that his three-year property, this other thing over there, seven-year property. And so you, you write off a portion of that total over time and the cream already has a travel FOMO. Yeah.

So yeah, once all restrictions are lifted, everybody's going to go nuts. So there is that. But yeah, so, right off is an expense for tax purposes, whether it's an actual cash expense, where you, where you were money, leaves your account and goes into somebody else's account, or whether it's a Phantom expense, like depreciation, it lowers.

It goes against whatever income you have coming in. And so, so as far as what you can write off the. The IRS definition is things that are necessary and ordinary for your business. And that's, if you're a business owner, if you are an individual then very, very, very, very little can you write off?

So part of the tax cut and jobs act, which was Trump tax reform is they got rid of a lot of stuff on the personal side. So you know, if you're an educator, you can write off $250 worth of you know, books and supplies and things that you buy for your, for your class. If you are in the reserves you can run up some of your reserve training expenses.

If you are if you have if you have a mortgage, you know, you can write off mortgage interest, maybe a property, or maybe mortgage insurance property taxes, subject to limitations, that kind of stuff. Depending on how much you have and how much income you have, you might be able to write off the medical expenses.

You can rent of charitable contributions. But by and large, that's kind of it there used to be a lot more but you know, part of the tax cut and jobs act the way they, they quote-unquote paid for the tax cuts was that they got rid of a whole bunch of things that used to be able to deduct.

And so let's talk about Georgia has some of the most straightforward delinquent tax auctions compared to most States I've attended. Yeah. So Georgia is actually really interesting when it comes to its tax sales, but we'll get into that probably next week because we are about out of time.

Let me check the clock here. We got about 40 seconds. One minute left. Yeah. I, I, I'm not accurate. I know one of the ends of the show is coming. So I am going to, I guess, for the recording purposes, I'm going to call it here. And I hope you all had as much fun as I did. It's a show number two, and this is weekly Mondays live audiences, way better than listening to the replays.

But if that's all you got, if you're living in Australia, there'll be it. I hope to see you all next week.