Fitch also released a moderate assessment report for the Eurozone. The report stated that "There appear to be some signs of recovery in consumer spending" for the Eurozone. It was announced that consumption growth rose to 0.5 percent quarter-on-quarter in France and 1.1 percent in Spain in the third quarter, while in Germany, after a decline in the second quarter, an increase was observed in the third quarter.

The statement drew attention to the significant increase in real wages, and said, "Eurozone growth is slowly beginning to recover as rising real wages create a more supportive environment for consumer spending."

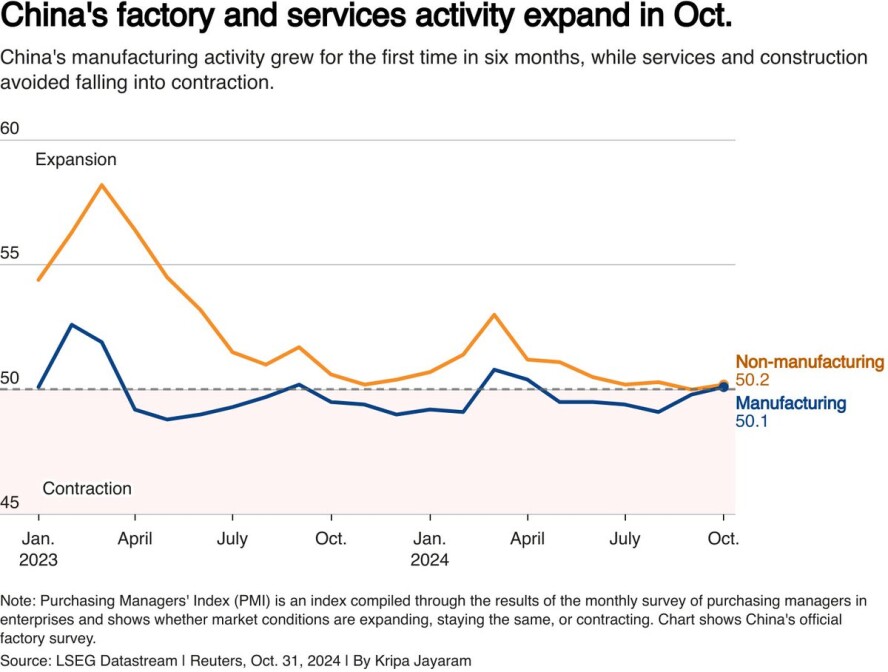

Supportive data came from China on the energy and commodity side. Despite signals of a slowdown in economic activity in China, unexpectedly positive manufacturing data was released in October.

The official manufacturing purchasing managers index (PMI) rose to 50.1 in October, rising above the 50 threshold for the first time since April. Economists participating in the Bloomberg survey expected the manufacturing PMI to be 49.9. The non-manufacturing PMI, which includes the construction and services sectors, also rose from 50.0 in September to 50.2 in October.

The manufacturing sector has been on a sluggish course in recent months due to falling producer prices and decreasing orders. In addition, China's exports fell last month and the economy recorded its slowest growth rate since the beginning of 2023 in the third quarter. Despite this, officials are optimistic that the latest stimulus package will soon have an impact.

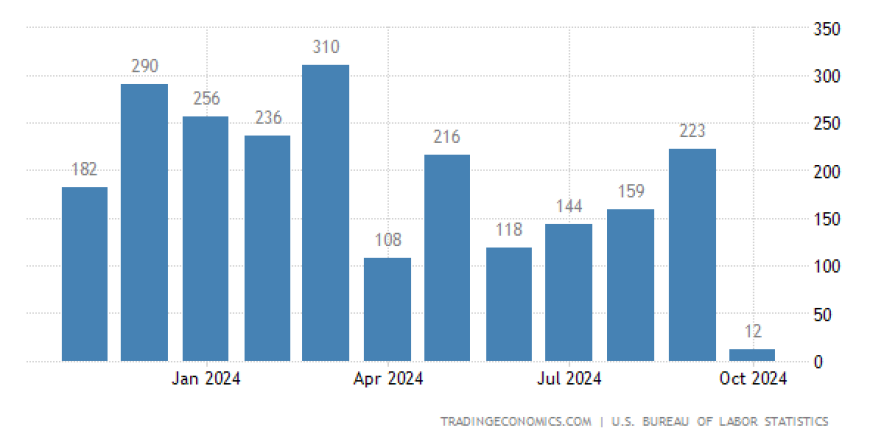

We are sensitive to nonfarm payrolls data in the US. Nonfarm payrolls increased by 12,000 in October and the unemployment rate was 4.1%. Economists who participated in the Bloomberg survey expected the increase in employment to be 100,000.

September nonfarm payrolls data was revised from 254,000 to 223,000. Although the 12,000 number may sound strange, the reason for this was the Boeing strike and Hurricanes Helene and Milton hitting the southeastern states. No change is expected in the inflation outlook because this data was anticipated.

Leading indicators indicate that the October employment market is lively. ADP private sector employment exceeded expectations with an increase of 233,000, while unemployment claims fell by 12,000 weekly to 216,000 as of October 26. Continuing unemployment claims fell to 1.86 million.

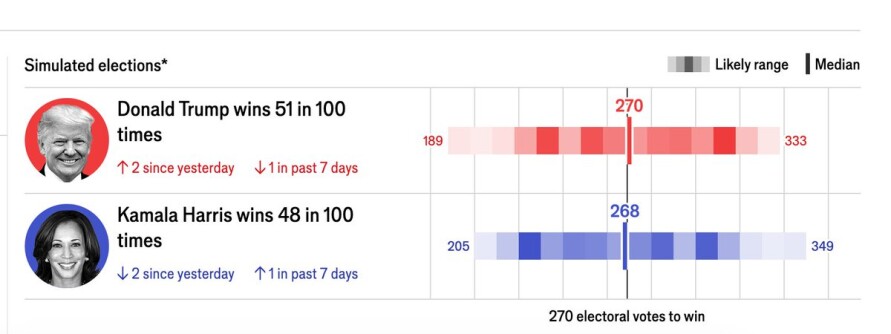

The US elections are just a few days away. The latest polls show that the election will be a close one. Trump led Harris for the first time last week in TheEconomist’s model. The model shows a 51% chance of Trump returning to the White House. This change in the model is due to Harris’s recent decline in national polls.

New polls released state by state also show Trump’s lead in swing states. Both candidates are making efforts to get voters to the polls in the final stretch of the election. The 2020 election had the highest turnout in US history since 1900. This was due to the ease of voting by mail due to Covid restrictions.

While Republicans’ early voter turnout increased from 27% to 32%, Democrats’ turnout remained stable at around 48%. While this development gives hope to Trump’s supporters, some experts say that there is ongoing debate over whether early votes are just a possibility of splitting the votes that will fall on Election Day or whether they include new voters in the process.

Oil prices have retreated since the beginning of the week after Israel’s attack on Iran did not target oil or nuclear facilities and Tehran responded with a measured response. Brent fell to $72.5, while West Texas Intermediate (WTI) fell to $69. The declines came after Iran’s Supreme Leader Khamenei signaled a measured response to Israel’s attack and refrained from directly threatening retaliation.

Demand-side pressures may now be more decisive for oil than supply-side concerns. China’s weak demand is the main driver of the decline in oil prices, and market players are more sensitive to this data. In addition, the expectation of an increase in Saudi Arabia’s oil production on December 1 is another factor that is putting pressure on prices. There has been no official statement from Saudi Arabia on this issue yet. Goldman Sachs says the market’s focus has shifted from the Middle East conflict to the risks of a possible oversupply in 2025.

Çinli otomobil üreticisi BYD Company, 30 Eylül 2024'te sona eren üçüncü çeyrekte, yıllık %24 artışla 201,1 milyar yuan (28,2 milyar dolar) gelir elde ederek ilk kez Tesla'nın aynı dönemdeki 25,2 milyar dolarlık gelirini aştı. BYD'nin net kârı %11,5 artışla 11,6 milyar yuan (1,6 milyar dolar) olurken, Tesla'nın net kârı 2,2 milyar dolar olarak gerçekleşti. Elektrikli araçlara olan talebin azalmasıyla birlikte, BYD'nin hibrit araçlara odaklanması, şirketi Tesla'dan farklı bir konuma taşıyor.

The information, comments and recommendations contained herein are not within the scope of investment consultancy. Investment consultancy services are provided within the framework of the investment consultancy agreement to be signed between brokerage firms, portfolio management companies, banks that do not accept deposits and customers. The comments in this article are only my personal comments and these comments may not be appropriate for your financial situation and risk return. For this reason, investments should not be made based on the information and comments in my articles.