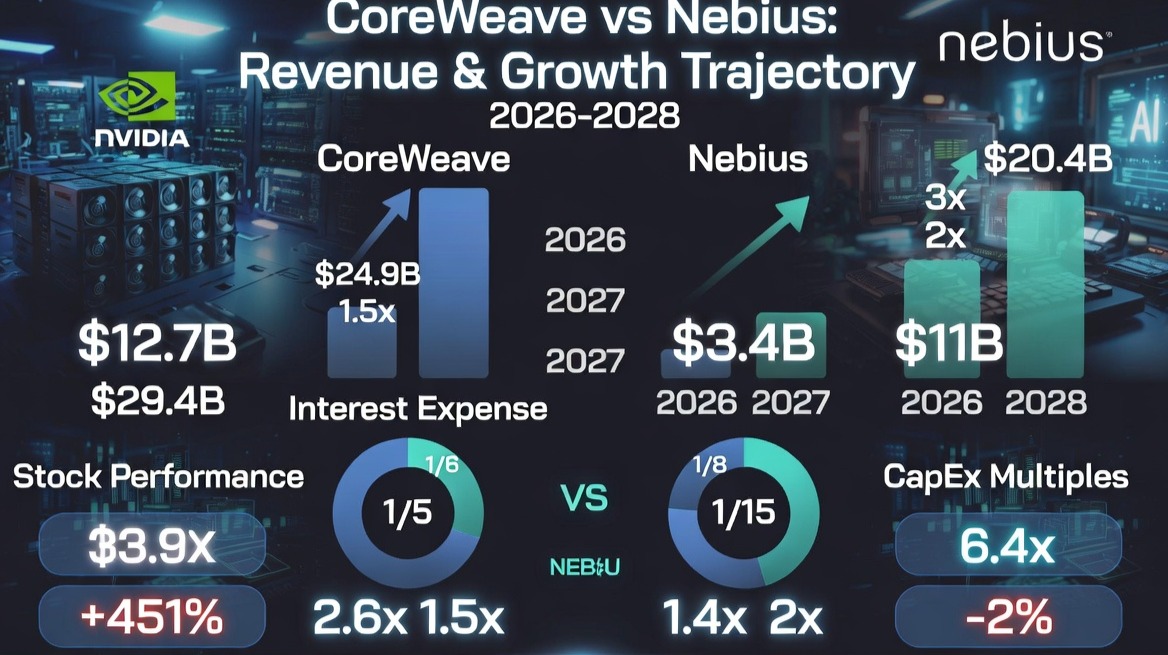

Now I would like to make a comparison between $CRWV and $NBIS for you. CoreWeave is expected to generate $12.667 billion in revenue in 2026, rising to 24.907 billion in 2027, roughly doubling. $NBIS is expected to generate revenues of $3.441 billion in 2026 and $10.993 billion in 2027, which roughly corresponds to 3 times the revenue. Now let's look at the 2028 revenues of the two respectively: CoreWeave 39,416, Nebius 20,384. This tells us that CoreWeave has 1.5 times its 2027 revenue, while Nebius has roughly 2 times its revenue. This is the first difference between the two companies, you will say that since CoreWeave's numbers are larger, it is more difficult to grow like NBIS, yes, you are right at one point, but this is just the beginning.

Let's look at interest expenses. CoreWeave gives 1/5 of its 2026 income as interest payments. In 2027, this figure is 1/6 and in 2028 it is 1/7. NBIS pays 1/8 in 2026, 1/15 in 2027 and 1/20 in 2028. Did this turn a light on in your mind?

If we also look at its CapEx, CoreWeave is spending 2.6x its revenue in 2026. In 2027, it reaches 1.5x and in 2028, it reaches the new breakeven level. NBIS spends 6.4x of total income in 2026, 2x in 2027 and 1.4x in 2028. Here, CoreWeave is better, now look at the margins, which one is better and look at the cash flow per share, when you put these in place, it can be better understood why one stock brought 451% in the last year while the other one brought (-2%).

Now let me draw a little road memory with my own thoughts. Oh, by the way, the data above is S&P Global Market data and I interpreted them with numbers, not with stories. Although CoreWeave stands out in some notes, Nebius is ahead. NBIS was a company that I was pleased with as an investor for a while, and I like it very much. Now let me tell you what we should look for in CoreWeave or whatever I might be a buyer for. If interest rates come down and OpenAI becomes profitable as early as Anthropic, that would be a plus for CoreWeave in my opinion. However, the company's debt CDS, which originates from OpenAI, declines. At that point, debt restructuring seems more attractive to me. The entire CDS will not improve, only the part originating from OpenAI will decline, other risks may continue, remember this. Of course, having Nvidia behind it is an advantage, but also a disadvantage in terms of dependency, but this is less of a problem, of course. I also look at companies mathematically in this way, when I exclude the story. After all, mathematics never lies.