Aave? What is it? Is it a crypto trading platform? Can I make money on Aave? Is Aave a trustworthy place to do transactions? If you have any of these questions in your mind, then you are in luck. Because today's topic of discussion is Aave. I strongly recommend reading their whitepaper to get to the meat of it, where they discuss about all the maths and other calculations that power the Aave system. Here, we will talk about Aave from the perspective of a common man.

What is Aave?

The word 'Aave' is Finnish in origin and it's literal translation is - ghost (The logo of Aave has a cartoon ghost as seen in the picture below). Aave is a decentralized version of a traditional bank on smart contracts which enables lending and borrowing where an algorithm determines the interest rates. In other words, it is a part of decentralized finance or DeFi (which simply means financial systems controlled by smart contracts without any central authority like a bank) that lets people to lend and borrow cryptocurrency anonymously without having to go through any intermediary. If you lend, you earn interest; if you borrow, you pay interest. Such platforms are also known as a decentralized lending pool protocol (very similar to liquidity pools but with more services), which is an ecosystem of smart contracts running on top of the Ethereum Blockchain. Aave is a form of (or an example of) a decentralized autonomous organization or DAO which are organizations powered entirely by smart contracts and it's associated community votes for changes & upgrades using it's governance token. In the case of Aave, it is governed by the Aave community which uses the Aave token (which are traded on all the popular crypto exchanges) to vote for changes and upgrades. The more tokens you hold, the more voting power you have. We will talk all about it in the following paragraphs.

History of Aave

Stani Kulechov is founder and CEO of Aave (Kulechov is not a developer; he has a background in law). Aave started out initially as a project called ETHLend which was launched on the Ethereum MainNet network in early 2017 (this was the period known in the crypto world as the 'ICO boom' where a lot of ICOs were launched every other day). ETHLend collected a sum of $16.2 million from it's ICO where it released the 'LEND' token as it's governance token. It was one of the first DeFi protocol to have launched. ETHLend was quite different from Aave that is today; it was a P2P loan service, which means it simply connects people who are looking to borrow money to people who are willing to lend (this is an oversimplified version but essentially this was how it worked). It was further upgraded in 2018, but the development team quickly realized that such a P2P lending model is a difficult concept to actualize and put into practice. For instance, it was very difficult to find matching lenders and borrowers.

Around this time, other DeFi protocols began to emerge. There came a popular DeFi protocol called UniSwap DEX (Decentralized EXchange) which leveraged a P2C (Peer-To-Contract) model where a liquidity pool is created by the lenders using smart contracts (read the linked article to know more about liquidity pools) instead of everyone trying to find a borrower individually. ETHLend developers took this idea and soon enough, ETHLend adopted this P2C model, then rebranded themselves as Aave, as they are known today. Aave's lending pool now has over $7 billion worth of liquidity at the time of writing this article. Aave is now competing with other DeFi lending pools like Curve, InstaDapp and Compound (You can visit this website called DeFi Llama to check the liquidity of various DeFi pools). The 'Lend' token which was launched during the ETHLend ICO has been converted to 'Aave' token by the end of 2020 by a ratio of 100:1, i.e. 100 Lend tokens were converted to 1 Aave token (if you had invested in either Lend or Aave, it would have been an excellent investment as both the tokens has become 'multibaggers' where they 10x'ed and 40x'ed their value respectively by 2021). This change was a part of a series of updates to the Aave protocol called Aavenomics. There were several updates to Aave after this, with the most significant one being the launch of Aave V2 (check the link for more information) where the team took feedback from the users & the community to solve various challenges and issues with the existing Aave protocol.

How does Aave work?

As mentioned before, Aave can be considered as a decentralized version of a bank. And every bank offers two main services - lending and borrowing. You may wonder how does this work? Well, let me explain. Aave works based on it's liquidity pool. This is how it operates - investors (people with crypto holdings) can deposit their crypto into the Aave protocol and get interest in return. These crypto assets can then be accessed by people who wants to borrow it for a specified borrowing interest rate decided by the pool. This interest amount which are paid by the borrowers will be given equally to the investors or the lenders for providing liquidity to the protocol based on how much liquidity they have provided. Also note that you can take a loan from the protocol if you have any crypto assets deposited within the protocol, i.e., your crypto assets that are currently in lending within the protocol can be considered as a collateral if you ever wanted to take a loan.

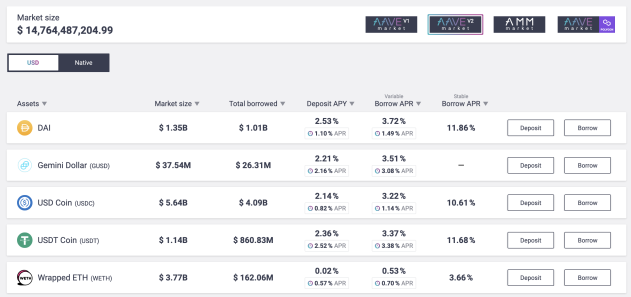

For example - take a look at the above screenshot from the Aave site. Here for the DAI token (a stablecoin) for example, if you deposit or lend this token in this pool, you'd get 2.53% APR or Annual Percentage Yield of your holding (APR simply means you'd get this much percentage of the money that you've put in after one year) and if you borrow this coin then you'll have to pay 3.72% APR to the pool. You may notice that for stablecoins like DAI or Tether, the interest rate higher compared to the WETH or Wrapped ETH, which is pegged to Ethereum. This is because of the fact that ETH's value is subject to a higher degree of fluctuation than a stablecoin. Now you may wonder - how do I borrow from this pool? Normally if you go to a bank to get a loan, they'd ask for a collateral in the form of housing, gold, vehicle, etc which is worth more than the amount you are trying to get so that if you default on your loan, they can simply take ownership of your collateral, sell it and get their money back. In the world of DeFi lending protocol, you have to give the collateral in ETH and you will get about 80% of your collateral amount as the loan amount.

Now you may ask - why would I want to take a loan if I already have more than that amount in ETH? Well, consider this situation - you have $100 worth ETH and you put that as a collateral to take out a loan of $80 worth Tether, a stablecoin. Then after a couple of months, you've decided to pay the protocol the $80 plus interest rate to get you ETH back. Now your ETH might have doubled it's value. So when you cash out, your ETH is now worth $200. This is a tricky situation though because Aave has got something known as a 'liquidation threshold limit' (which is somewhere around 82.5% of it's original value of the collateral), and if the value of the ETH that you've kept as collateral drops beyond this limit, then Aave will automatically sell or liquidate your ETH to prevent any loss. This is done to protect the investors or the lenders investment. So in our example, if the ETH's value became $82.5 from $100, then Aave will automatically sell it. You can keep the $80 worth Tether though but you won't get back your collateral, i.e. the ETH. This may not sound that appealing to the average joe like you and me but what this means is that Aave allows something known as leveraged lending which is attractive to a lot of crypto traders.

Leveraged Lending

Basically this is 'lending on steroids'. Let's understand it with an example. Say you've $100 worth ETH where you've put that as collateral and took a loan worth $80 in Tether. You take this Tether, head over to another lending pool like UniSwap, where you swap it for equivalent amount of ETH. Then you came back to Aave and deposited this ETH so you've got $180 worth ETH in the Aave pool. Now comes the interesting part - you can still take another loan worth 80% of this latest addition of ETH, which is around $64 in this case, which you can then again swap for ETH and put this ETH back in Aave, making your total deposit as $244 worth ETH, even though originally you only had $100 worth ETH. Now imagine that ETH's value went up by 10%. You'd gain a profit of $24.4 from your current position; if you hadn't done this leveraging, then you'd only have gotten $10.

However, if it went the other way, i.e. if the value of ETH goes down, well, you wouldn't want to be that person especially if the value crosses the liquidation threshold limit, which basically means you'll lose all your deposits, including your original $100 worth ETH. Essentially this type of lending can be considered as a 'high risk, high rewards' type of trading.

Loan Repayment

In a traditional bank, if you have taken a loan, then you need to pay it back along with the interest amount by a fixed time period. Aave loans are not like that. Aave loans doesn't need to be paid by a certain date. Since you are in an over-collateralized position (which means you've had put up more than 100% of the loan amount), you just have to login and repay the loan every now and then a little bit at a time. As long as your collateral (ETH) is nowhere near the liquidation threshold limit, you can borrow for an undefined period.

However as the times goes by the accrued interest rate grows making your loan's health factor to decrease, which more likely leads to a point where your collateral needs to be liquidated to prevent loss. Now such a scenario arises when you don't pay the interest amount; if you do pay the interest amount regularily, then you and your collateral is fine.

Flash Loans

Aave offers a new feature unique to it's protocol (which is one of their main USP) called flash loans. Flash loans are essentially loans where you can borrow millions of dollars worth of crypto without putting up any collateral for a small fee. But here's the thing, such a loan needs to be paid back in the same cryptocurrency block that it was borrowed in (which is around 11-13 seconds in the Ethereum network at the time of writing this article). Why would you need such a loan which you need to pay back almost immediately? It's mostly used in arbitrage trading where you buy crypto from exchange A or liquidity pool A for X amount, say $1, then sell it on exchange B or liquidity pool B at a slightly higher rate, say $1.10 and the difference in the trade is your profit. Now imagine such a trade where the transaction amount is worth $1 million. You could essentially make $100,000 from such a trade.

Aave do charge a small fee for such flash loans which is around 0.09% (i.e. for $1 million dollars, the fee is $9000). Since the repayment time is just a couple of seconds, such trades are conducted using smart contracts. But it is rare for such a trade to happen nowadays as the margin difference between crypto assets in various exchanges are not big enough to reap expected profits. Nevertheless it is possible. There are two other things that you can do with flash loans - self liquidation (where need a lot of money to repay a loan to withdraw your collateral which went up in value ) and collateral swap (where you can borrow money with less steps). You can read more about it in Aave's official documentation.

Now there is something known as a 'Flash Loan Attack' where flash loans can be used to exploit vulnerabilities in a smart contract. For example someone found out that there was a bug in the pancake bunny protocol which is a yield farm (a form of DeFi protocol where users can lend their crypto funds, which remains locked up within the protocol, in order to earn fixed or variable interest in the form of it's governance token); the protocol pays it's investors in pancake bunny tokens as interest for their coins and tokens which are locked up. The bug they found could be exploited to make a lot of pancake bunny tokens for a given amount, more than it is supposed to. So the attackers borrowed around $700 million worth of crypto, used it to get 7 million pancake bunny tokens which they immediately sold for $745 million, then they repaid the $700 million which earned them a nice profit of $45 million. Flash loans in this way is a risk a any small bug's impact can be maximized to a huge impact. So there are two factions within the crypto community - one faction thinks that flash loans are dangerous and it should be illegal & banned whereas the other faction believes in it's use cases and want to allow it because according to them, anyone including the developers behind pancake bunny could have found & exploited the bug all smart contracts are prone to bugs.

Aave Token

In the cryptocurrency market, there are three main categories: currencies, platforms, and tokens. Bitcoin is an excellent example for the first category, which is currencies. They are all built as peer-to-peer digital currencies and have no other significant features. Ethereum is a good example for the second category, which is platform. These currencies are also referred to as frameworks or operating systems for distributed apps as we can write smart contracts on Ethereum network with runs on Ethereum Virtual Machine. Solana, Polkadot, Cardano and Binance Smart Chain are some other examples. Tokens, the third category, are issued on such platforms. Tokens could be either utility tokens (tokens that promise a future use of a product or service like ETH in Ethereum) or governance tokens (tokens that can be used to make decisions in the protocol) where they serve a role inside it's corresponding application. Aave tokens belongs to this category and as mentioned before, it is a governance token.

Token price for governance tokens is a bit difficult to evaluate. Unlike utility tokens, where the price grows with the increase in demand for the underlying network or application, for governance tokens there is no real connection between the token price and increasing liquidity in the pool. Ideally, it should be the case but in reality it is not. Many investors say that trading volume of a protocol is a good way to evaluate the token price of a governance token but there are instances where this doesn't hold. So far, the biggest influence on the token price of Aave has been the growth of the entire industry itself as it saw it's biggest boom during the DeFi boom period between late 2020 and early 2021. Nevertheless, as discussed before, Aave token has been a good investment so far as it 10x it's original price. But in general, investors tend to stay away from such tokens because such governance tokens are deflationary in nature, i.e. their value depreciates over time as more tokens come into circulation every single day.

Conclusion

So there you have it folks. That's all you need to know about Aave to get started. To reiterate, Aave is a decentralized lending and borrowing platform like a DeFi bank. Aave is powered by smart contracts and it's community where the governance is done via Aave token, which has been a good investment so far (this is not a financial advice by any means; do your own research before buying or selling this token). There are other lending protocols similar to Aave like Compound, Curve or InstaDapp. We even discussed about how Aave works, how it lends money and how is a loan repaid. I hope this article has cleared your doubts regarding Aave to some extend. I recommend to research more about Aave if you want to seriously get involved in the lending - borrowing before using this protocol as this post is just meant for beginners who have no idea about Aave or DeFI lending platforms.

Couple of other articles which you might be interested in:

- Is Solana (SOL) the real 'Ethereum Killer'?

- All you need to know about Stablecoins

- All you need to know about Liquidity Pools

- All you need to know about Hardware wallets

- All you need to know about Hyperledger

- All you need to know about NFT

Check out KuCoin exchange if you haven't already for better crypto services.