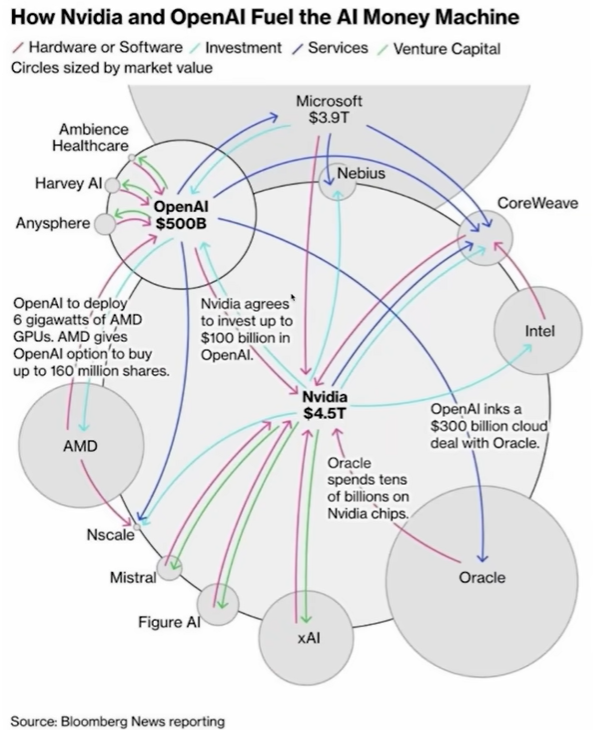

Nvidia is not an AI company in the traditional sense. It does not sell chatbots, assistants, or consumer software. Nvidia builds the one thing every AI company needs to exist: the chips. Every serious AI model today is trained and run on Nvidia hardware. That single fact places Nvidia at the gravitational center of the entire AI economy.

Around Nvidia, you see companies like OpenAI and Oracle playing very different roles. OpenAI builds products such as ChatGPT and provides the application layer and model structure that other companies build on. Oracle focuses on infrastructure by building and operating massive data centers where these models actually run. But both ultimately depend on Nvidia chips.

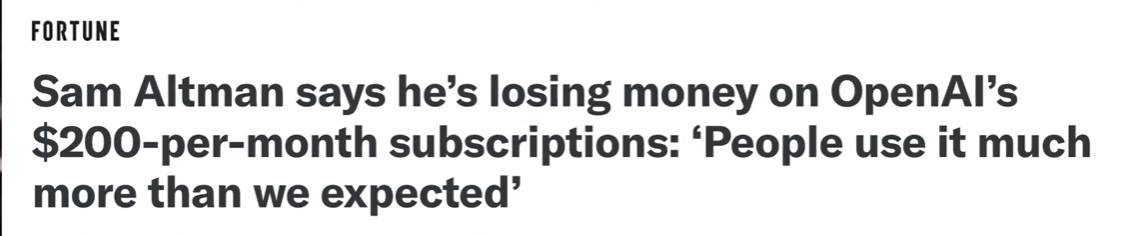

This is where the revenue contrast becomes important. OpenAI is valued at around 500 billion dollars, yet its reported revenue is roughly 12 billion and profitability remains negative. OpenAI itself has admitted that each ChatGPT user costs money to serve. Sam Altman has even said that some premium users cost the company hundreds of dollars per month. That is why many people call AI a bubble.

The argument goes like this. If AI companies are losing money, then the entire ecosystem must be inflated.

But that logic breaks down when you look at Nvidia.

Nvidia is the only company in this chain that is consistently increasing revenue. Not projected revenue or future revenue, but real revenue. Demand for newer and more powerful chips keeps rising. Prices are going up, not down. Orders are booked years in advance. If this were a bubble with no real demand, chip prices would be collapsing. Instead, they are climbing.

This creates a contradiction. People say AI is a bubble, yet Nvidia chips are becoming more expensive and more scarce. Bubbles usually show excess supply. Nvidia shows persistent shortage.

At this point, Nvidia has become more valuable than the entire pharmaceutical industry combined. Investors are not betting on hype alone. They are betting on continued demand. Nvidia must keep producing faster and more efficient chips, not to create demand, but to keep up with it.

Still, skepticism remains, and it becomes more interesting when you look at investment flows.

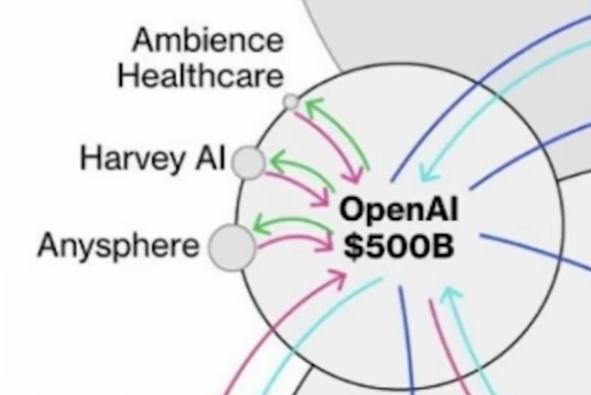

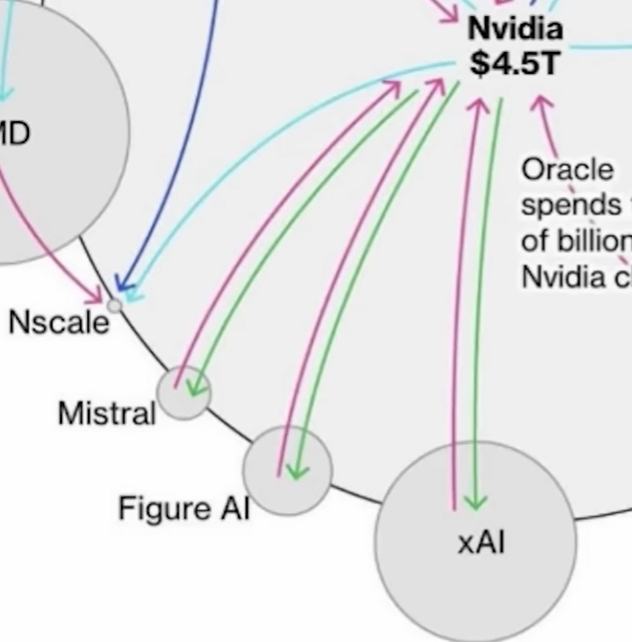

OpenAI spends billions buying Nvidia chips despite not being profitable. Nvidia, in turn, invests venture capital into AI startups like OpenAI, xAI, and Mistral. Those same companies then buy Nvidia hardware. The visual representation often shows green arrows going both ways, investments flowing out and purchases flowing back in.

This raises an uncomfortable question. If demand is truly organic, why does Nvidia need to invest in these companies at all.

The key detail is that these diagrams usually do not show monetary scale. Nvidia may invest billions, but the amount OpenAI and others spend on hardware is far larger. Nvidia is not propping up demand for its chips. It is securing future customers and accelerating ecosystem growth. The money coming back to Nvidia is significantly more than the money going out.

The same pattern applies to OpenAI. While it currently loses money per user, demand for its products is real. People use ChatGPT at scale. To move toward profitability, OpenAI is slowly expanding monetization through higher pricing tiers, enterprise usage, and now content and feed based experiences that can generate recurring revenue.