***HISTORY***

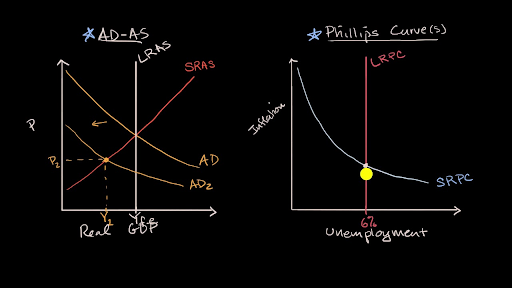

Economic theory has held that there exists an inverse relationship between unemployment and inflation. Again, in theory, if you think this through, it makes sense. When you have low levels of unemployment, workers have available more disposable income to go out and spend and with the rise in demand comes a rise in the price of the consumer goods purchased (increasing inflationary pressures). And, when there exists high unemployment there is less disposable income available decreasing the demand for consumer goods bringing on a corresponding decrease in prices (lowering inflationary pressures).

This inverse correlation was first noted by New Zealand Economist A. William Phillips in 1958 contained in a paper entitled "The Relation between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861-1957". [Phillips, A.W. "The Relation between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861-1957". Economica. 25 (100): 283–299. https://onlinelibrary.wiley.com/doi/10.1111/j.1468-0335.1958.tb00003.x (Accessed July 6, 2021). Following the publishing of Phillips' paper, many economists in industrialized nations took his work to believe that this inverse relationship was a stable one.

This was very important as it lead both economists and policymakers to believe that applying Keynesian theories to the economy, both inflation and unemployment could be kept in check. This would all be accomplished by manipulation of the money supply, and there would always exist a stable trade off between inflation and unemployment that policymakers would have to monitor and further adjust monetary policy as needed to stabilize the Economy.

Once Phillips broke ground with this inverse correlation, economists went to work on it taking the simple premise of the Phillips Curve and complicating it exponentially (Anything beyond the simple view of the Phillips correlation is beyond the scope of this article). And while the Phillips correlation historically is valid for short term periods, the lessons of the 1970's demonstrates that the Phillips curve is not stable for long term economic planning.

***THE DECADE OF STAGFLATION***

In the 1970's, many countries experienced what was referred to as "stagflation". More particularly in the United States for a majority of the decade, the economy suffered high inflation, high unemployment, and sluggish growth. Under the teachings of Phillips, this situation could not occur, but when it happened, economists were quick to attack the validity of Phillips. In fact, this attack was lead by Milton Friedman, one of the more noted economists of our time.

What happened historically in the 1970's which lead to the breakdown of Phillips theory. As always, it was a combination of factors, all converging at the same time.

Two major reasons exist worthy of mention. First, then President Richard M. Nixon, finalized the end of the Bretton Woods accord, in effect removing the US Dollar totally from the Gold Standard. As the Dollar was no longer backed by anything of intrinsic value, it was left to waffle about subject to whatever whim existed in the market at the time. [See, e.g. Office of The Historian. "Nixon and the End of the Bretton Woods System, 1971–1973". https://history.state.gov/milestones/1969-1976/nixon-shock. (Accessed July 6, 2021)].

But of much more significant import, Nixon imposed a series of wage and price controls mandating what sums businesses could charge for their goods in the market. As the value of the US Dollar decreased (unsupported by the backing of gold), the costs of producing goods correspondingly rose. But due to Nixon's price controls, producers were unable to raise the prices of goods to bring its revenue in line with the rising costs. To stay afloat, businesses were forced to cut costs by cutting payrolls. Thus with the continuing decrease in the value of the dollar coupled with the payroll cuts, both inflation and unemployment were rising at the same time. [See. Id.].

I would be remiss if I failed to tell how the US emerged from this period of stagflation (although it is not necessary for the purposes of this article). The US, by actions of one Paul Volcker, then Chairman of the Federal Reserve, undertook severe short term actions inflicting much pain upon the economy. To curb the rampant inflation he caused interest rates to soar to around 20% knowing this move would create an overall economic contraction. This contraction was in fact a recession that struck the US Economy in the early 1980's with GDP falling approximately 6% and millions of people jobless. However, the recovery from the recession was robust and corrective of the stagflation evils that plagued the Economy in the preceding decade. [See, e.g. Federal Reserve History. "Volcker's Announcement of Anti-Inflation Measures". https://www.federalreservehistory.org/essays/anti-inflation-measures. (Accessed July 6, 2021)].

***CONCLUSION***

It was a historical review of data that gave us the Phillips Curve analysis of an inverse correlation between inflation and unemployment. But it was the unique and severe historical economic conditions of the 1970's that proved Phillips analysis unreliable. Presently in the US we are experiencing high rates of unemployment and as of late we are experiencing higher prices for consumable goods. The current situation is disturbingly similar to that of the pre-existing conditions of the 1970's relative to stagflation, so with Phillips once again unreliable as a long term predictor, should it be scrapped?

Solely, in my humble opinion. Phillips curve analysis was merely an indicator of short term trends occurring in an inverse fashion, nothing more. The lesson's of the 1970's clearly demonstrate it's unreliability as a long term tool for use by policymakers in addressing disruptions in the Economy. For short term trends, in normal economic times, Phillips analysis is viable. But for long term predictability, especially in times of economic stress, Phillips is unreliable, and as history has shown inapplicable.

We never should have been attempting to employ Phillips as an economic policy tool in the first place.