If you read my previous post on GMX, you’ll know that now that we’re in a bear market, I’ve finally found the time to dig in and do some research on some platforms that I have heard about but hadn’t really been able to play around with. With Juno’s current “Stellar Madness” promotion (which I’ll breakdown a little bit later), I finally did my homework and I thought it would be useful to share some of the information that I found about Juno, and why I decided to finally sign up.

What is Juno?

Launched in 2020, OnJuno (or officially relaunched as Juno in 2022) is what many consider to be a Neo-bank, but in fact, it isn’t actually a bank. It’s perhaps easiest to think of Juno split into two different arms — TradFi and Crypto. The TradFi arm acts as a bank because their banking services are provided by Evolve Bank and Trust, Members FDIC. In other words, just like any other official bank, your funds are federally insured FDIC up to $250,000.

On the flipside, the crypto-arm is not FDIC insured (as no crypto I know of is or can be), but is “under the custody of trust and licensed custodians who keep the majority of the crypto in cold storage, and have taken up necessary insurances.” From what I’ve read, this cold storage is from BitGo, who if you haven’t heard before, is a major industry cryptocurrency custodian who was involved but not implicated with the 2016 BitFinex hack.

How does Juno make money?

So for the TradFi part, the way Juno makes money is pretty straight forward— they’ve partnered with their selected brands to shave off some of the sales generated from card users which in turn generates their income stream; I’m assuming like an affiliate link. And then secondly just like any store owner will tell you, fees can be generated every time a user swipes the debit card itself.

With all the contagion events we’ve been seeing, I think a deeper question is how Juno generates its crypto-related yields — which unfortunately I couldn’t find that much specific related information. The limited answer I did gather was that they use their “regulated exchange partner, Wyre, [who] primarily deals with institutional lending desks and some minor on-chain protocols to generate yield on crypto assets.”

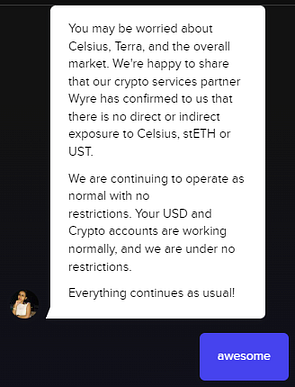

Also, speaking directly with customer service, I was informed that:

Although we know that the spread of contagion goes much farther than Terra or Celsius, this was relieving to hear nonetheless.

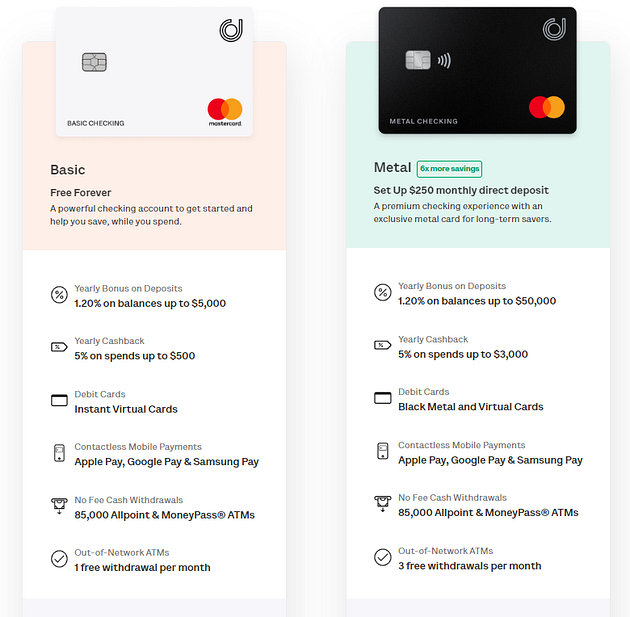

Membership plans

In a nutshell, there are two different options: Basic vs. Metal

Dissecting some of these features, there are some things worth noting.

- Yearly bonuses on deposits drops from 1.20% to 0.25% on the balance of funds greater for $5,000 on basic and $50,000 on metal. (But honestly if you’re parking that much money on there, I strongly suggest you seek out a financial advisor).

- The 5% cashback is limited to only a certain number of brands, the last I counted 43. The big names include Amazon, Target, Netflix, Spotify, Apple, and Starbucks. If you don’t normally put any spend on any of these vendors, then…this card probably doesn’t make a whole lot of sense. Also, the brands are subject to change.

- The cashback also can only be received for eligible purposes, and they spell out specifically that purchases on prepaid card reloads or prepaid gift cards are not eligible. (Sorry MS’ers)

- The interests rates can (and have in the past) changed. For instance back when they first launched in the Fall of 2020, they were offering an interest rate of 2.15%, but they reduced their rates to 1.20% in May 2021.

- Both plans are essentially free, the only qualifier for the metal card is an ongoing direct deposit of $250. And speaking of “free,” this leads me to my next section…

Are there fees?

Whenever I see the words “free” or “forever,” I naturally get a bit skeptical, because I always assume that free comes with a cost, and with debit cards, that usually means hidden fees. Juno does cite a FAQ for fees in their terms and conditions, but the link that’s supposed to direct people to the fee break down goes to this:

And upon further digging, it does appear that they really don’t have a fee structure, even for overdrafts. In fact, if you take a look at their disclaimers page, they state that there are no maintenance fees, no overdraft fees, no minimum balances required on either the metal or the basic card. And even with the the upgraded metal card, if you discontinue your direct deposit, they will essentially just downgrade you back to the basic card.

Essentially I couldn’t find any mention any fees with the TradFi arm, but with Juno’s crypto arm, there are fees I found for which I’ll talk about in the next section.

The Crypto Arm of Juno

So what makes Juno a “Neo Bank” is how well integrated Crypto is within its platform. There are multiple crypto-related features such as:

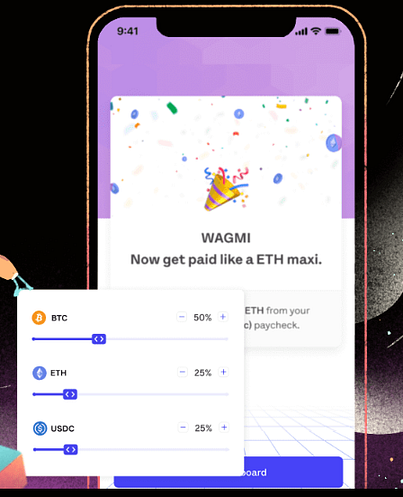

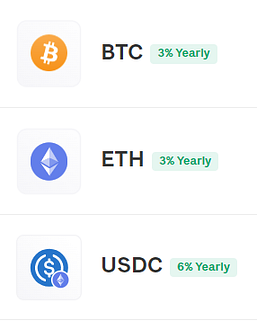

1. You can allot a part of your paycheck across multiple cryptocurrencies:

This is a pretty awesome feature to be able to on-ramp fiat to crypto. As shown in the graphic above, the 3 options are for ETH/BTC/USDC, and they also have an option to auto-sweep your crypto into your cold or hot wallet.

2. You can earn yield on your crypto deposits:

These rates are pretty low with respect to what you can earn in DeFi, even without leveraging. Nonetheless, it’s still a cool feature to have.

3. There’s no ACH settling period for deposits.

This is a BIG difference compared to other on-ramping CeFI platforms as most (if not all) have at least some minimal lock-in period where you cannot withdraw your deposited funds until the ACH has cleared. As much as I use and respect platforms such as OkCoin, the 10-day ACH hold on deposited funds can get extremely annoying.

4. You can choose to make payments in either crypto or fiat

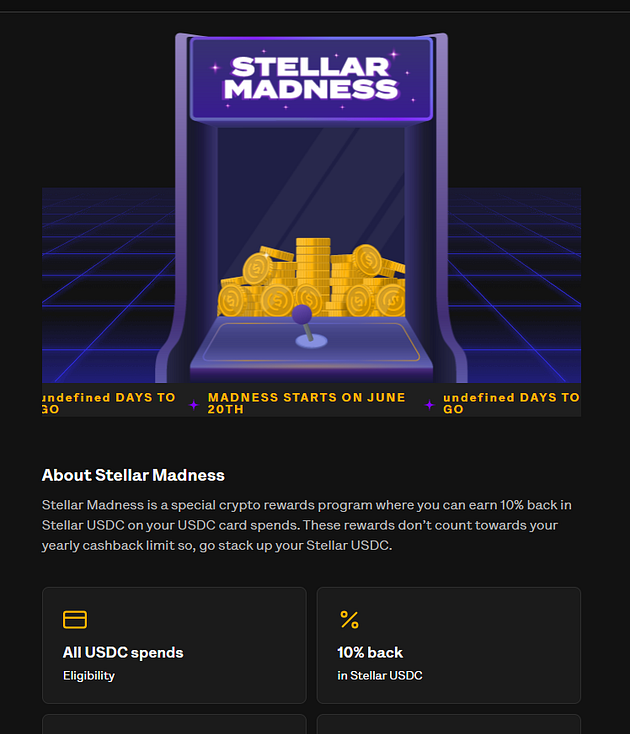

This is perhaps the most revolutionary — you have an on/off switch for whenever you want to pay with cryptocurrency or fiat. You normally get 5% cashback if you pay in fiat, but until at least July 31st, you can get 10% cashback if you decide to pay in USDC, for up to $300 dollars per year. And currently with their Stellar Madness promotion, if you decide to make your payments in $USDC, you can get 10% back on purchases for up to $100 in cashback in Stellar USDC:

And just to clarify, the stellar madness promotion is for ALL spend done in USDC (not just your selected brands), and this does not count towards your normal $300 dollar cashback limit.

5. Buy/Sell Fees:

So the fees around Juno’s crypto arm were perhaps the hardest thing for me to decipher, simply because the fee structure appears to keep getting pushed back. However what I found is that all crypto buying and selling below a total volume of $250,000 is free until July 31st (this was pushed back from June 30th), and everything over that amount has a 0.50% fee per buy and sell order. After July 31st, everything will have a 0.50% fee.

Other factors to consider

Financials: Juno like many DeFi platforms is VC funded and back in 2019 where they raised $3 million dollars in seed funding from the likes of Sequoia Capital, Consensus, and Dragonfly Capital Management. You can find more information about this here.

Based out of India: Juno is based out of India, and it appears that their team is doxxed with many of their associated linkedin profiles.

User Reviews: I’ve read through countless user reviews on Trustpilot and Youtube, and although most of the reviews were positive, I think the most common complaints were from people either not getting their $100 bonus for setting up a direct deposit, or other technical issues like not being able to setup their direct deposit at all. Another theme I saw were that some users were not able get a hold of customer support, but in my experience, I was easily and quickly able to access customer support through their chat feature — which was incidentally how I found many of the specifics for this article.

TLDR; Conclusion

From what I could gather, Juno (or OnJuno) is a pretty stellar fintech platform that helps bridge the world of TradFi and Defi. Could they be more transparent about their financials? Yes, but I wonder how limited their ability to be transparent might be if their crypto-yields are actually generated by Wyre, rather than through their own team. Also taking a look at the yield rates themselves, I wouldn’t classify 6% on USDC or 3% on ETH/BTC to be in the “too good to be true” category and instead as relatively conservative. Does this rule out the possibility that they could be making degen loans like Celsius? No, but any experienced person from DeFi could easily hypothesize these returns pretty rationally.

Given my findings, I will definitely start depositing at least the minimum $250 to qualify for the $100 bonus into my newly opened Juno account and see where things go from there. My direct deposit won’t hit for the next couple of weeks, but I do see this as a good method to help me DCA into ETH/BTC while I’m waiting out this bear market.

If you’re reading this and interested in trying out Juno too, please consider supporting this blog and using my referral link: https://onjuno.onelink.me/TkoI/referral?code=JAME4XIL. If you setup a direct deposit of $250 dollars or more, we’ll both receive $100.

Thanks for reading, and as always, please be sure to follow me on twitter to read all about my latest findings and updates: https://twitter.com/CryptosWith

Disclaimer: None of this information is financial advice, and is just speculation from me, a random guy on the internet. Please consider this for purely educational and entertainment purposes. As always, please do your own research or contact a financial advisor to find what investments might be best for you.