Hey folks, so the following article is just a lot of observations from my deep dive into $USDR and $TNGBL, respectively the stablecoin and altcoin of Tangible.store, a pioneering project designed to offer stablecoin yields backed by real world assets (RWAs), namely real estate. Similar to any crypto project, one should do their own research and it should be known that the cryptomarket is inherently risky. So I will give my personal takes when all is said and done, but please DYOR and determine what your own risk appetitive before investing into anything.

Why $USDR?

So if you’ve followed me for a while, you’ll know that I’m really into looking for lucrative stablecoin plays, and lately, $USDR has been extremely hard to ignore:

That’s right, currently 9 out of 10 top yields involve $USDR — strange for a stablecoin that barely has $64 million in total marketcap:

https://www.tangible.store/realusd

https://www.tangible.store/realusd

Therefore looking at all of these crazy yields, I found it worthwhile to try to determine if we’re dealing with a Terra-like scam, or if maybe the Tangible team is truly onto something novel and revolutionary. First let’s discuss how the mechanics work…

What is $USDR?

$USDR otherwise known as “Real USD,” is an overcollateralized stablecoin that is primarily backed by RWAs, namely different real estate properties, but others including gold, watches, and even bottles of wine. If you’re familiar with real estate in particular, the first thought you’re probably thinking is: How is this possible to create moveable liquidity from a non-liquid store of value such as real estate? Well first, part of the answer is that $USDR is not technically 100% backed by real world assets, instead it is composed of by the following:

As you can see in the breakdown above, approximately only 41.44% is backed by real estate, which is roughly 2/5th’s of the total marketcap. Another almost 40% is backed by crypto, including $DAI and 3CRV LP, but you’ll also see that 29.79% is backed by $TNGBL — the native altcoin of the protocol. Now for those of you that have warning signs blaring for a stablecoin that is backed by low marketcap altcoins — history would justify your concerns. Yet it appears that the Tangible team has recognized these concerns and created an Insurance Fund (which you can also see in the graphic above) which accounts for nearly 9% of TVL. According to the docs, the Insurance Fund’s sole purpose is to be deployed to help ensure that users can redeem their $USDR 1:1 with $DAI if the collateralization ratio falls below 100%.

What is $TNGBL?

With a max supply of 33,333,333, the $TNGBL token is the native altcoin for the Tangible project that accrues rewards for its holders depending on how long you decide to lock up your tokens via a “3,3+” NFT:

Like most voter-escrowed models, the longer you decide to lock up your tokens, the greater rewards you can expect to receive, with a multiply-decay rate decreasing over your escrowed time. In other words, in month 10 you can expect a multiplier of 8.5x, but by month 20 that multiplying effect will be reduced to 4x.

According to the docs, 66% of protocol fees are given to the NFT holders in $USDC, with the remaining 33% to be “used to buy and burn the token.” Similar to BeethovenX’s $maBEETs, NFT holders can claim their rewards at any time, yet they are incentivized to not “claim all” early because that in effect would kill your multiplier level. It should be noted however that you do have allotted “claimable rewards” where you can withdraw with no penalty.

Diving into the tokenomics, the vesting schedule is a bit interesting because the majority of tokens that are allotted to the team and Tangible Labs is through the 4 year 3,3+ NFTS:

What’s different about this compared to most other projects is that theoretically the token shouldn’t be dumped all at once; instead their allotments are what their 3,3+ NFTs themselves are emitting, albeit at the highest multiplier rate.

OK, so we’ve learned about the tokens behind the protocol, what about the RWA’s?

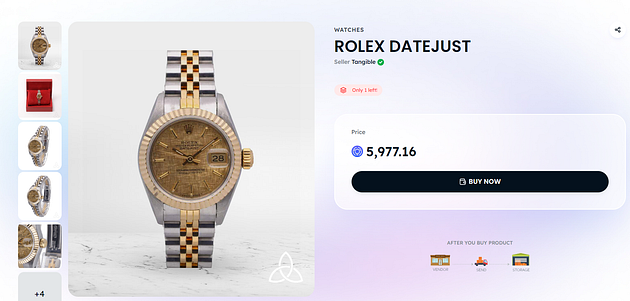

As I mentioned earlier, the RWAs that back $USDR aren’t just real estate, for they also include things like gold bars, wine, and yes, watches:

All these items are tokenized by NFTs, called “TNFTs” which gives the NFT holder technical ownership of said asset. Also if you’ll look closely, the price listed above is in $TNGBL not $USDR/$USDC, which means that as $TNGBL is trading currently closely to $10 dollars, the price for this Rolex is closer to $60,000, not $6,000.

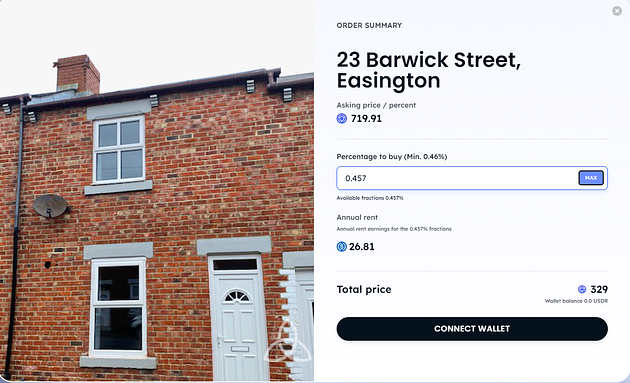

On the real estate front, at the time of writing there were a total of 162 different TNTF properties, including this one where you can buy a 0.46% fraction of for 329 $TNGBL:

Doing the math, this would be a $3,237.36 investment to earn $26.81 annually, or in other words a 0.83% APR. Now on the surface level this might sounds like a poor investment, but regardless of how $TNGBL fluctuates in price you will still own 0.457% of the property, and given market history, the inherent value of the property may increase which (should) trump the value that you would get through rent.

My Takes

I am really excited about what Tangible is doing, but there’s a few items that still give me some yield signs before aping in. These include…

- Tangible provides a great deal of transparency, but the industry demands more. Real estate management can be a complicated process, and it’s clear from a lot of questions I’ve seen on their discord that people want more and more. Is it fair to have 100% transparency in novel tokenization protocol right away? Probably not. Nonetheless, first reading about this gave me some YieldNodes vibes where the team said that all these things were being done to support their “Decenomy”…right up until they froze people’s ability to deposit and withdraw their funds.

- In the same vein, a Proof of Reserves are needed, otherwise we’re blindly trusting our funds with a centralized authority. If you’ve been burned by the likes of Celsius, Voyager, or BlockFi you’ll know exactly what I’m talking about — a centralized authority can tell you whatever you want about trust, but as everyone should know about Crypto, don’t trust, verify.

- I know that some may disagree with me on this one, but the housing market is not invincible. It may not necessarily happen tomorrow, but there have been many calling for another housing crash to occur soon. Regardless of when it may or may not happen, the 2008 financial crisis left the housing market in shambles and there’s no guarantee that it can’t happen in again. Is real estate less volatile than crypto? Sure. All I’m saying is that it’s no fun when the value of your home drops by 40–50%.

- An Insurance Fund full of altcoins isn’t really an insurance fund. Once again referring to the docs, the Insurance Fund is reportedly consistent of different altcoins including $BAL, $CRV, and $AURA. Let’s take a look at the price action for some of these tokens shall we?

$CRV has had a -60% price drop in the last year:

$BAL has had a -50% price in the last year:

That being said, I am pleased with the fact that an insurance fund is in place, but honestly as much as I believe in some of the projects like Balancer or Curve, I certainly wouldn’t use them to insure my own home, or even my car.

Conclusion

From what I’ve gathered, Tangible is genuinely venturing in uncharted territory and on the verge of establishing a clear bridge and use case for tokenization of real world assets, and for that reason alone I’m rooting for them to be successful because ultimately their success will help drive the adoption of cryptocurrency and blockchain technology forward. We need people like Tangible to figure out how to make this work, and for all of us crypto-nerds I truly hope that they do.

For me personally, I’m going to be sidelined a bit longer until I see more transparency, especially with the Proof of Reserves that they’ve reportedly been working on for the past few months gets released.

Are you a 3,3+ or TNFT holder? If so, I’d love to hear about your experience in the comments below. Also, please feel free to speculate with me if you yourself are sitting on the sidelines because I’d like to know if there’s anything I missed.

As always, thanks for taking the time to read this and be sure to follow me on twitter (https://twitter.com/CryptosWith) to get all my latest updates. Also, looking for a gift for your Crypto-loving/hating friend? Give them a REKT journal to cheer them up!

Disclaimer: And as a final reminder, this is not financial advice and this is for educational and entertainment purposes only. Please as always, do your own research and find what investments are best for you. Cheers everyone!