Hey folks, if you’ve been following me through this bear market, then you’ll know that I’ve spent a lot of this time researching different platforms that are providing pretty solid returns on your assets while you’re waiting things out. I did an in-depth review about Juno Finance in the past (also not to be confused with the Juno Network), but they recently announced that they will be airdropping their own native token $JCOIN for Juno users.

I’ll get into more detail about the airdrop in a bit, but first let me do a recap on Juno itself and also other added benefits for why I think Juno is in a league of its own compared to other TradFi banks.

A quick recap about Juno Finance:

Launched in 2020, OnJuno (or officially relaunched as Juno in 2022) is what many consider to be a Neo-bank, but in fact, it isn’t actually a bank. It’s perhaps easiest to think of Juno split into two different arms — TradFi and Crypto. The TradFi arm acts as a bank because their banking services are provided by Evolve Bank and Trust, Members FDIC. In other words, just like any other official bank, your funds are federally insured FDIC up to $250,000.

On the flipside, the crypto-arm is not FDIC insured (as no crypto I know of is or can be), but is “under the custody of trust and licensed custodians who keep the majority of the crypto in cold storage, and have taken up necessary insurances.” From what I’ve read, this cold storage is from BitGo, who if you haven’t heard before, is a major industry cryptocurrency custodian who was involved (but not implicated) with the 2016 BitFinex hack.

Using Juno to Earn and Save

Juno has essentially been creating the easiest bridge between cryptocurrencies and traditional fiat which will increase adoption of users into the crypto-space. The features that make Juno stand out?

- 2.15% interest on fiat checking — I know that 2.15% interest earned in crypto is a pretty big nothing-burger, but in the TradFi world, this is more than 70x’s greater than the national average for interest bearing checking accounts. And unlike crypto-projects, because this is a standard checking account, your fiat is FDIC insured.

- Crypto paychecks — I’d imagine this is particularly attractive for people who like to DCA, but with Juno you can allot all/some/none of your paycheck to crypto. There’s even an “Autosweep” function to automatically send your purchased crypto to your 3rd party wallet like Metamask. And even if you don’t do a crypto paycheck, if you setup a direct deposit for at least $250 or more, then you’re eligible for Juno Metal Checking, which leads me to the 3rd feature…

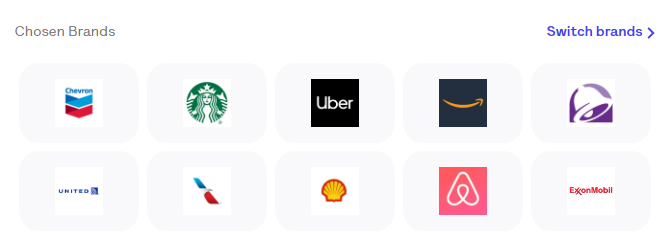

- Up to 10% cashback on select brands using your debit card — Normally it’s only 5%, but currently until October 15th, you can earn 10% cashback if you select to pay with $USDC on your Juno debit card. I wasn’t too hyped about this at first, until I saw what the brands are. Currently there’s more than 40 to choose from, but my current ones include:

I’ve been in the credit card miles and points game for awhile, and normally the highest cashback offers (without significant limitations) that you’ll see on credit cards is around 5% if you’re lucky, so 10% is almost an outright steal.

OK Enough, so what about the airdrop?

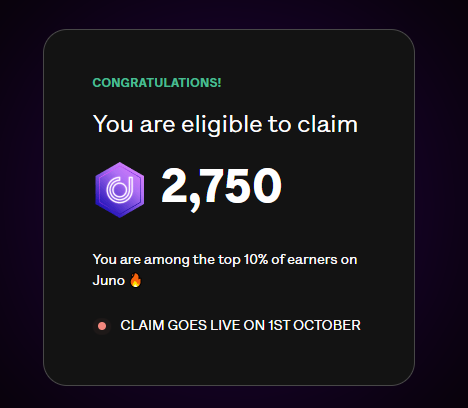

Tomorrow (September 30th, 2022) Juno will be doing a snapshot to check on existing user and the tokens will be distributed on October 1st:

So if you were on the edge of deciding whether or not to sign up for Juno, this might be the final incentive for you to do so. Honestly though I don’t know how accurate it is because apparently mine have already been allocated:

Does $JCOIN Have Utility?

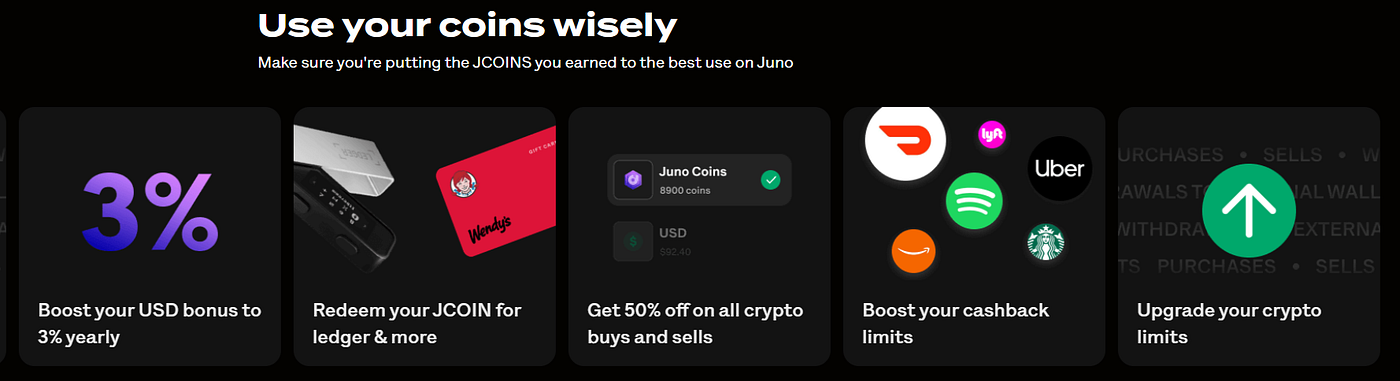

This is perhaps what most exited about because they’ve teased a lot of attractive benefits for $JCOIN holders including:

The feature that I’m most excited about is the the 3% USD bonus, making this 100x’s better than the average checking-earning interest account. From what I’ve gathered, instead of having a reward point system like many TradFi banks have, Juno is making their reward points into tokens — a concept that I would imagine 20-or-so years down the road, most TradFi banks might go to.

Conclusion

I honestly don’t know how much these tokens will be worth, and I wouldn’t recommend signing up for the airdrop alone, but I do think that Juno is a great product as you can park your fiat without the fear of getting rugged. Unlike platforms like Celsius or Voyager, because Juno is a TradFi/Crypto hybrid, your fiat is FDIC insured up to $250,000 dollars so in the case that something happens to Juno, your funds should still be protected.

And if you’re like me, you might have been saving up $USDC in order to enter the market for when we hopefully see that last capitulation that will (hopefully) signal the end of this bear market.

The way I see it, Juno offers one of the better options to allow you spend your $USDC on in-real-life purchases at a massive discount, while at the same time waiting to make the bottom-barrel crash prices that we’ll hopefully see sometime soon.

If you’re reading this and interested in trying out Juno too, please consider supporting this blog and using my referral link: https://onjuno.onelink.me/TkoI/referral?code=JAME4XIL. If you setup a direct deposit of $250 dollars or more, we’ll both receive $100.

Thanks for reading, and as always, please be sure to follow me on twitter to read all about my latest findings and updates: https://twitter.com/CryptosWith

Disclaimer: None of this information is financial advice, and is just speculation from me, a random guy on the internet. Please consider this for purely educational and entertainment purposes. As always, please do your own research or contact a financial advisor to find what investments might be best for you.