Hey folks, I know I normally cover things on crypto-related products, but today I’m going to be sharing some of the research I’ve done in trying to find the best place to park your fiat.

If you’ve been covering the TradFi markets lately, you’ve probably gotten the gist that investors are a bit spooked right now from holding their fiat in traditional banks, especially since so many of them are failing. I’ll go into this a bit more in my “Risks to consider” section, but despite these risks, today I’m going to talk about Savebetter, essentially a market-making aggregator that allows investors to enter High Yield Savings Accounts (HYSA), High-yield CDs, and also no penalty CDs.

Despite my conviction for the future of blockchain technologies, following the advice of most financial advisors, I think it’s still wise to diversify your portfolio to make sure that all of your eggs in one basket.

Enter SaveBetter

SaveBetter essentially lists and allows you to access all the top high yield savings products for your USD, rates that can be significantly higher than what you could get by going directly to the bank or credit union yourself — all the while still retaining FDIC insurance on your funds.

Not only are you accessing significantly higher rates, SaveBetter allows you to access different financial products simply through the SaveBetter platform, essentially requiring the investor to have only one account, regardless of how many different financial products you decide to access.

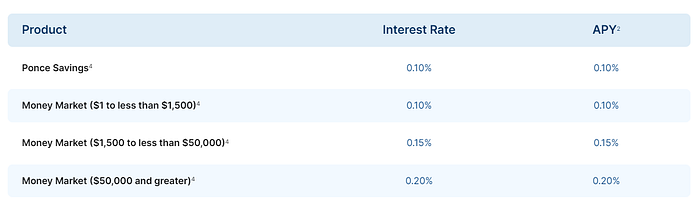

How high you might ask? Let’s take Ponce Bank for instance. On their website, they currently offer a range of 0.10% to 0.20% APY on their Money Market account, depending on how much your deposit:

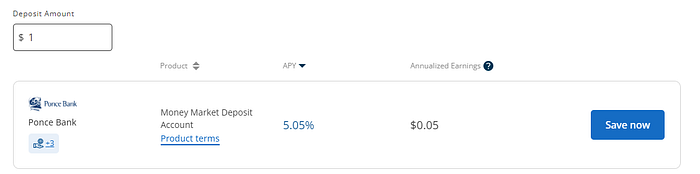

However by accessing Ponce’s Money Market savings account through SaveBetter, one could get an APY of 5.05% with a minimum deposit of $1.

This is a mind-blowing 25x better rate than going through Ponce directly.

How does SaveBetter offer these rates?

First of all, I should preface that SaveBetter not only offers FDIC and NCUA insurance, but they advertise “No Fees.” In other words, you’re not going to find a portion of your principal or profits shaved off when your deposit or withdrawal:

The fees are actually something that’s passed on to the prospective financial institution, not the retail investor. It’s unclear what SaveBetter’s exact terms are for each bank/institution, but what is clear is that these rates have all been negotiated, giving the bank a win because they’re able to attract more liquidity, giving SaveBetter a win because they’re shaving off a fee from the bank/institution, and giving the retail investor a win because they’re capitalizing on higher savings yields.

It’s actually quite typical for banks to spend huge amounts of money on different sign-up bonuses and advertising, so SaveBetter allows banks to negate some of these costs, ultimately leading to higher rates passed on to the retail investor.

Great. But this sounds eerily familiar to Voyager, Celsius, BlockFi, etc.

If you’ve been burned in the past by Voyager, Celsius, and BlockFi (like I have), you’ll probably have alarm bells ringing in your head that SaveBetter sounds like it’s doing the same thing. The short answer to this is both a yes and a no. Yes, in the fact that they’re using your funds to produce higher rates, but it’s a no in the sense that your funds are no longer yours (as they were in the above mentioned crypto-centralized exchanges). Although your funds are stored in a “Custodial Account,” these funds are directly deposited into the bank/institution that you choose to deposit with — all which are FDIC/NCUA insured. According to their terms of service:

The Service Bank has established an omnibus custodial account at the Service Bank (the “Custodial Account”) to hold funds of individual customers participating in the Service, including you, until such amounts are transferred by the Service Bank to the applicable Deposit Account (as defined below) or Customer Account, as applicable. The Service Bank also has established omnibus custodial deposit accounts at each Product Bank to hold the funds deposited by individual customers participating in the Service, including your funds, into CDs and MMDAs at such Product Bank(s). Each of these omnibus custodial accounts is referred to as a “Deposit Account.” Each Deposit Account at a Product Bank will hold only funds of customers participating in the Service who choose to deposit money with such Product Bank and will be used solely for the purpose of the Service.

This form of “Custodial Account” is actually not so different from any other FinTech product such as Robinhood, that essentially offers financial services while not being a bank itself. Likewise, SaveBetter is not a bank itself, but it acts as a conduit for you to access high yield products/yields from the banks/credit unions directly.

The biggest problem with centralized exchanges such as Celsius/Voyager/BlockFi, is that funds were lent to certain bad actors, namely 3 Arrows Capital (3AC) who mismanaged funds and were certainly NOT FDIC/NCUA insured. Now of course if we rewind back to early 2022, at the time 3AC wasn’t really known as “bad actors,” so can’t we say the same thing about banks such as Ponce Bank? What if they’re really bad actors in disguise? This leads me to my next section…

Risks and other things to consider

Banks can fail, just like 3AC: Yes, banks can be considered bad actors, but because of how they’re regulated, the federal government insures up to $250,000 if they for some reason go under. This is perhaps the biggest reason why I greatly wish that the government would appropriately regulate the Crypto industry so that retails investors could have the same assurances and protections that they have in TradFi, but I digress..

“24/7 online access to funds may not actually mean 24/7 online access to funds: From every review that I’ve read, everyone has been able to eventually access/withdraw their funds upon request, but there have been a few complaints where at times it took “several days” for their funds to be released, or other instances where funds were temporarily inaccessible because the site itself was under maintenance.

You’re accessing a bank’s yield, but not all the bank’s services: In the case of SaveBetter, just because you’re depositing money into a savings account, doesn’t mean that you’ll be able to actually use your money as it were in a savings account. In other words, if you need money to do things like pay bills, fees, etc., you won’t be able to do that with SaveBetter. The only course of action that you’ll have is to deposit, accrue interest, and then withdraw.

Only one 1099: Less paperwork and less complications are always a plus in my book when doing taxes. I’ve only started using SaveBetter myself this year so I haven’t gotten one of these yet, but from my understanding SaveBetter will consolidate one 1099-INT with all your earned interest from no matter many different financial products you access.

Conclusion

SaveBetter has now been around for nearly 3 years, and so far it seems like it’s generally been successful in offering retail to get better interest rates on their deposits than they would if they were negotiating directly with the bank/credit unions themselves.

Given the times, I understand if people are a bit hesitant about holding their funds (let alone different FinTech companies) to different banks, but I would argue that holding 100% of their assets in cryptocurrencies can be risky as well too.

If you’ve tried out SaveBetter yourself, I’d love to hear about your experiences in the comments below. If you haven’t used SaveBetter yet but are interested in trying it out yourself, please consider supporting this blog and signing up and using my referral code jamesk004242. (But even if you don’t, I’d still suggest using someone else’s referral code when you sign-up, otherwise you’ll be missing out on a $125 bonus that comes with your first 5k deposit).

Thanks for reading, and as always, please be sure to follow me on twitter to read all about my latest findings and updates: https://twitter.com/CryptosWith. Also, looking for a gift for your Crypto-loving/hating friend? Give them a REKT journal to cheer them up!

Disclaimer: None of this information is financial advice, and is just speculation from me, a random guy on the internet. Please consider this for purely educational and entertainment purposes. As always, please do your own research or contact a financial advisor to find what investments might be best for you.