In my previous article, we took a brief exploration of Modern Portfolio Theory or MPT. In case you didn’t get a chance to read it, I have linked it here for you: https://www.publish0x.com/investing-principles/building-a-winning-crypto-portfolio-part-1-modern-portfolio-xmngkr

To summarise the key points, we want to hold multiple assets in our portfolio that are either independent or negatively correlated. By doing this we reduce the overall risk of the portfolio and improve our risk-return position through a process of diversification. The holy grail of a diversification strategy is to build a portfolio with negatively correlated assets. If we can do this, then we can significantly reduce the riskiness (a.k.a volatility) of the portfolio.

In this article, we will take a more practical look at this, review some of the issues and think about how we can best apply these principles to investing cryptos.

Practical diversified portfolios

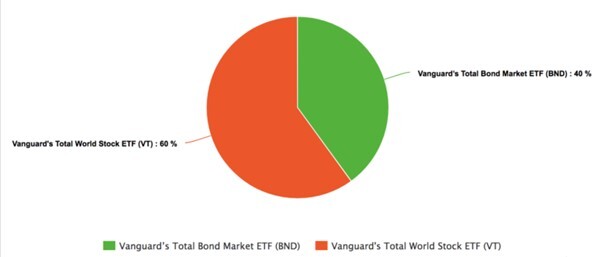

Ok, so we have gone to the trouble of finding assets which we think are uncorrelated with each other. Let’s assume we invest 60% of our assets in a well-diversified shares portfolio and we put the remaining 40% into a well-diversified bond portfolio. This portfolio allocated has been touted by Jack Bogle (the founder of Vanguard) as the ideal portfolio since it provides diversification across asset classes, as well across different companies. The idea is that this portfolio can provide diversification and reduce our risk across the economic cycle.

Fig 1. Jack Bogle’s ‘Ideal Portfolio’

When company earnings growth starts to slow (as we might see in a recession), then we would expect stocks to perform badly. The Central Bank wants to stabilise the economy and so will drop interest rates to try to help companies and protect employment. As interest rates fall, the fixed coupons received on bonds become more attractive and the value of bonds increases. Ideally the increase in the value of bonds offsets the decrease in value of the equities and our overall portfolio performance is protected from the economic downside. However the asset allocation will have changed and so to maintain the 60:40 mix of Equity vs. Bonds, we would be buying additional shares when prices are low (a good thing!). Over time, due to lower interest rates, companies can borrow money more cheaply and can reinvest in new projects and growth opportunities, which help to raise earnings. At the same time, foreign savings flow out of the economy in search of higher interest rates elsewhere, causing the exchange rate to fall. Goods and services now become cheaper in foreign currencies, improving the competitiveness of exports and again helping to raise earnings. Over time as employment rises, there is inflationary pressure on wages and domestic price levels, as the economy becomes ‘over-heated’. At the same time, due to the improved earnings, equity prices rise. To maintain stability in the economy, the Central Bank now raises interest rates, which in the short-term cause bond values to fall. Again, we rebalance the portfolio, but this time we buy more bonds whilst their prices are low.

Liquidity – the spanner in the works

Through the course of a ‘normal’ economic cycle (as described above), where economic conditions change in a reasonably ordered fashion, the diversified portfolio performs quite well and does its job. The problem is when there is a unexpected or ‘black swan’ event which leads to an economic crisis, and everyone rushes for the doors in a panic. This is exactly what happened during the 1997 Asian financial crisis and the 1998 Russian Financial Crisis. Embarrassingly this was also the time when the hedge fund run by Noble Prize-Winning geniuses, Myron Scholes and Robert Merton, called ‘Long Term Capital Management’ went spectacularly broke. They used the wizardry of ‘financial technology’ (i.e. modern portfolio and options theory) to build their portfolios, with seemingly uncorrelated, often exotic and negatively correlated assets. The problem was that as a result of the crisis, the correlation of all assets went to 1 (i.e. they all became perfectly correlated).

Fig 2. Long Term Capital Management – ‘Genius’ FAIL

When everyone is trying to sell at the same time, in an indiscriminatory manner, there is no benefit from diversification as everyone races to the safety of more liquid assets. In this race, ‘cash in king’. So, at the very time we most needed the benefits of diversification, it deserted us. Exactly the same thing has happened, time and time again; the dot-com crash of 2000, the 2008 Global Financial Crisis and now the 2020 CoronaVirus crisis.

So, diversified portfolios don’t work then?

Well, most of the time, diversification does work, but when we need it most of all, it fails. The thing to bear in mind though, is that we only realise a loss if you are also running for the exits. The only sure-fire way to get through this mess is by having a longer-term mindset. Even though you may see deep red everywhere in your portfolio, it is exactly the worst time to panic. If you have constructed a well-diversified portfolio and not over leveraged, then you have no reason to sell. The downturns are generally great time to bargain hunt and pick up more of the stocks you liked. If it was good value at $10 a few weeks ago, then surely its even better at $7 or $6 now. In the current crisis, I have taken advantage of the dips to dollar cost average on my long-term equity portfolio (my HODL stocks) – I have done the same with my crypto portfolio. As Baron Rothschild most eloquently coined it: “Buy when there's blood in the streets, even if the blood is your own." In the long run, this ends up being a winning strategy.

Fig 3. Contrarian investing by Baron Rothschild

What does this mean for crypto?

Since crypto assets are not subject to the same drivers as other asset classes, such as equities, bonds, property and commodities, we should reasonably expect them to be uncorrelated to these traditional asset classes. For this reason alone, I believe that every well-diversified portfolio should have some allocation to crypto. Personally, I am targeting an allocation of 10%. Needless to say, this is not investment advice but merely the personal choices I have made.

In the recent COVID crisis, we didn’t see crypto acting in a non-correlated way relative to other assets. All asset prices were impacted but as we noted above, this is what typically happens in an economic crisis as everyone is looking for liquidity and to try to preserve their wealth in cash. (All uncorrelated assets become correlated).

But that doesn’t mean that all is lost. We must remember that crypto as an asset class is still very immature and speculative and so the investors it attracts are probably biased towards speculators. I see myself more as an investor or HODLer and believe in the long-term benefits of crypto. Over time, as the asset class matures and dare I say it, more institutional money flows in, we may see it increasingly fulfil its promise as an uncorrelated asset. For this reason, I continue to hold crypto in my portfolio.

So what are the implication of this for the specific cryptos I should hold? The issue on this point is that the market is still dominated by BTC and ultimately, all cryptos rise and fall with king Bitcoin. The exception is the rare phenomenon of ‘Alt Seasons’, when Alts decouple from BTC. Over time, as crypto matures, we can expect the correlations to change as individual cryptos mature and gain adoption or fail. So, in anticipation of that time, I hold a portfolio of cryptos, rather than putting all my eggs in one basket.

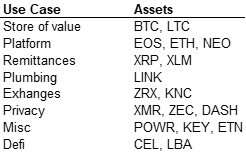

Table 1. Crypto use cases

The basis that I use for my diversification strategy is the crypto’s use case. I take care to ensure that I am not buying all assets that meet the same use case. In this way, I am anticipating a future where the values will be driven by different and uncorrelated factors.

The majority of my holdings are, of course, in BTC under the use case of ‘store of value”, with a small amount also held in LTC, following the view that LTC is digital silver if BTC is digital gold. My second largest holdings are the ‘platform’ use case, where I hold mainly ETH, but also a small amount of EOS and NEO. Much smaller holdings are then spread out across various other use cases, with my next largest being the ‘privacy’ use case. Right now, all of these use cases are correlated but I believe in the future, as adoption rises and the use cases mature, that they will decouple from tight correlation with BTC.

Conclusion

The lesson of diversification learned from modern portfolio theory apply to crypto markets as well as any other asset class. However, the thing to note is that at times of great dislocation and panic (such as now), all asset prices will fall. The only safe-harbour is typically cash. To avoid the need to liquidate at the worst possible times, make sure that you only invest what you can comfortably afford to lose. (That doesn’t mean you won’t be pissed off, just that you won’t be homeless and starving). Always try to keep some allocation to cash (‘dry powder’), so that you can go bargain hunting when there is ‘blood in the street’.

If you believe that in the long run, cryptos will be uncorrelated with other assets, then it makes sense to have some allocation to them in your portfolio. Right now, all crypto assets are tightly correlated to BTC (except during ‘Alt Season’), but you can construct your portfolio with the future in mind when individual cryptos will perform based on their own adoption and utility. My preferred way to do this is by thinking of the different ‘use cases’ and spreading my bets across the most promising use cases (e.g. not the ridiculous seeming ‘Car Taxi Token’ from the last bull cycle).