In one of my previous article, I had explained the strangle option strategy and how it could be used to sell currency options especially USDINR monthly options.

Strangle option strategy serves best when there is no directional move or there is no trend in the market. The golden rule is to sell far OTM options, but not that much far OTM options, otherwise there will no value in the option premiums. At times, it becomes necessary to sell close to spot price as far out of the money options premium would not yield any fair value for the whole operation. In such situations, risk will always be there and it becomes necessary to protect the positions against the knee jerk reactions due to news flows or any event specific movements.

It is more challenging to adjust and manage the existing strangle option positions when there is a sharp move in the market. Many times it has been observed that USDINR pair has no direction but on a particular day due to event it might show the movement of more than 1%. Next day it might come back to its normal, this disturbs the existing positions. Let us try to understand using a simple case scenario, assume the USDINR pair has been strictly range bound within 73–73.80 for the current month expiry. In this situation the option sellers have clear opinion that USDINR has no trend and it is wise to sell OTM Puts and Calls. But due to certain event the USDINR falls below 73.0 lvl to make a low of 72.80 only to bounce back to 73.10 lvl the next day. In such situations any put option sold below 73.0 i.e., 72.75 PE would be disturbed resulting in exit. You might then reenter the position when the pair bounces back to its previous level. This would mean that you will incur some losses.

Is there any probable solution for such type of situation? Not exactly, but you can minimize the loss by securing the put position. To safeguard your positions both up and down we will secure our strangle positions by creating iron condor.

Iron Condor Option selling Strategy

This is a non-directional strategy, you can also call it a secured strangle strategy. The only difference between strangle and iron condor is the number of positions created or opened. In strangle minimum two positions are created (both sell). In strangle at least one OTM put and call is sold and thus the position is hedged. In case of Iron condor besides opening two sell positions additional two positions are created. These two positions are created by buying the OTM call and put options. The two buy positions act as insurance cover for the two sell positions or the strangle. These two buy positions are created by taking into account sudden knee jerk reaction. These two buy positions also minimize the losses if the currency pair suddenly starts to trend. Thus for each put sell there will be a put buy position created and vice-versa for call options.

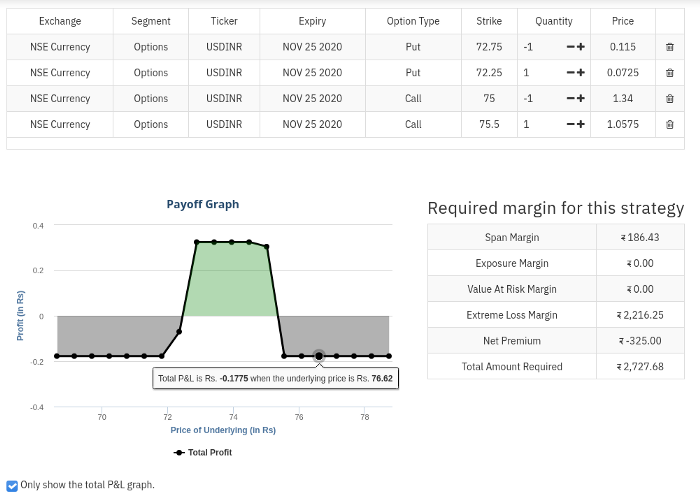

Let me explain with a use-case. Suppose USDINR pair is currently trading at 73.40 and over the last couple of months it has been range bound between 73–73.80, then it makes sense to deploy strangle strategy by selling far OTM put and calls. In this case I will be selling 72.75 or 72.5 PE on Put side and 75.0 or 75.25 CE on call side. But I will also secure these two sell positions by buying equal number of put and call options. So to secure 72.75 PE I will buy 72.25 PE and the buying position will be financed by the premium received by selling the 72.75 PE. Similarly I will buy 75.5 CE and this will be financed by selling the 75.0 CE.

In case the pair starts to trend or any event occurs then the buy position will increase along with the sell position. Here are some of the scenarios how this position will work.

a) Uptrend

Suppose the Currency pair starts to move in upward direction then 75.0 CE sell position will be at loss. To cover up for the loss the 75.5 CE position will also start to move upward thus each will balance out each other. Now, from here few things can happen. Either the expiry will happen just below 75.0 (74.90–74.95)strike price or just above 75.0 (75.01–75.10). In these two situation the premium would decay almost worthless and still you will get to book some profits.

If the expiry happens between 75.10–75.5 then there will be some minor loss. If expiry happens above 75.5 CE then also the loss would be fixed and no matter even if USDINR touches 76–78 the losses would be fixed as shown in the graph. Though the above situation is hypothetical, naturally you would exit if the expiry is going to take above 75.5 CE booking some loss. The below graph explains the scenario on Call side operations.

Payoff graph for an Iron Condor Strategy from upstox strategy builder

b) Downtrend

If the expiry happens just above 72.75(72.80–90) then in this case the premium would expire worthless and you will get to keep some premium till the expiry. If the expiry happens between 72.75–72.25 then there will be minor losses and if expiry happens below 72.25 then the losses would be fixed. The above payoff graph would explain this situation on Put Options operations

c) Neutral

This is the ideal condition and if the expiry happens anywhere between 72.75–75.0 then Iron Condor strategy would yield results to you and you will get to keep all the premiums.

Also, worth noting is the margin requirement. The above payoff graph has been generated for 1 lot of USDINR for November 2020 and the margin requirement is only Rs 2728. If you sell 20 lots then total margin requirement would be Rs 54560 and premium received would be Rs 6500.

Technical Specifications of Iron Condor Strategy

- Strategy Type — Non-Directional

- Ideal conditions for deployment — Non-trending markets

- Minimum number of positions required — four positions both for OTM puts and calls

- Loss Percentage — Fixed

- Profit Percentage — Fixed

- Condition — For every sell position equal number of buy position is created

- Margin requirement — Minimal compared to other strategies.

Conclusion

This strategy is a non-directional strategy and is deployed when there is no market movement. The profit and losses are fixed so you can relax without worrying much about the markets. While deploying this strategy equal number of positions should be created for the sell positions, i.e., if you are selling 20 lots of 72.75 PE then you have to buy 20 lots of 72.25 PE. This will ensure that balance has been created and each position will manage the adverse movement in another position. Some people even try different variation of this strategy which will be covered in the next article.