As China continues to make great strides in its digital yuan project that should allow it to challenge the hegemony of the U.S. dollar in the digital world where China can have the first-mover advantage, the Fed is taking a deeper look at the pros and cons of a digital dollar. The big question the Fed is asking is how a digital dollar could improve the American payment system.

In January 2022, the Fed published a study entitled “Money and Payments: The U.S. Dollar in the Age of Digital Transformation” which I invite you to read.

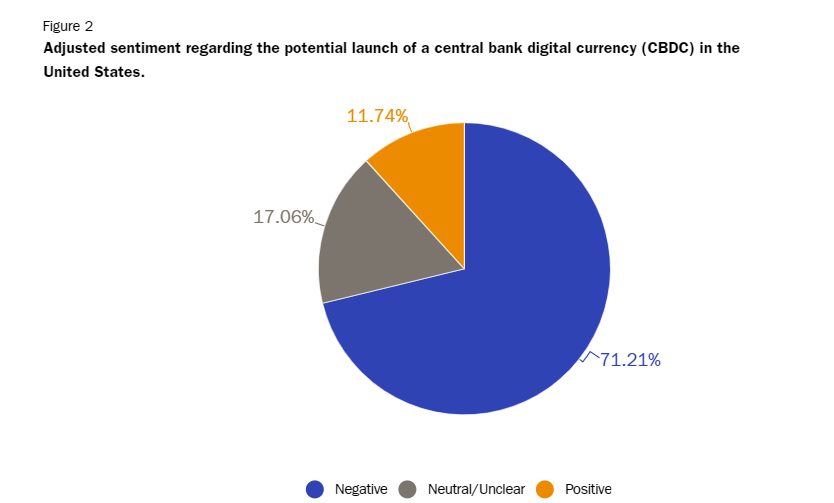

Nicholas Anthony, a policy analyst at the Center for Monetary and Financial Alternatives at the U.S. think-tank Cato Institute, points out that “a clear majority of commentators continue to view the potential launch of a digital dollar negatively.”

To verify this, you need only look at the more than 2,000 comments left on the Fed's platform following the release of the Fed's study on the advisability of launching a digital dollar.

More than 7 in 10 respondents say they are concerned or outright opposed to the idea of the United States programming its own digital currency.

The most common concerns are financial privacy, financial oppression, and the risk of disintermediation of the banking system.

A digital dollar would mean the end of financial privacy

It is true that a digital dollar, a stablecoin issued by the Fed, would look very similar to the current digital forms of the U.S. dollar (via bank accounts, online transactions, and payment applications). But this CBDC (Central Bank Digital Currency) would establish a direct line between the government and the financial activity of the public. In doing so, a CBDC would erase what little financial privacy still exists in the United States.

“Contrary to popular belief, an American CBDC is not necessary to digitize the dollar, as the dollar is largely digital today. However, issuing a CBDC would fundamentally rewire our banking and financial system by changing the relationship between citizens and the Federal Reserve,” the American Bankers Association (ABA) argued in its lengthy letter to the Fed's Executive Board.

A fully transparent CBDC, where information about its users and all their transactions would be accessible to the relevant authorities, raises legitimate privacy concerns but also about fundamental freedoms, with the potential use of digital currency to apply arbitrary sanctions against citizens.

Entrepreneurial Opportunism

Cato's political-economic analyst pinpoints an interesting trend in the notices given to the Fed: large companies working in finance, technology, and regulatory compliance are showing the most interest in the digital dollar:

“Some commenters seemed explicitly interested in securing a government contract on the impending project. Whether it was for consulting services or to offer their cutting-edge technology, these commentators did not hesitate to let the Fed know that they wanted in on the action,” Nicholas Anthony highlighted.

In addition to these commenters, there are service providers who have had or still have contracts with the European Central Bank. Their feedback, therefore, seems to be aimed at protecting and even strengthening their business relationships.

An obvious reluctance of the banking world on a digital dollar

While the plan for an official digital dollar already appears to be not only possible but imminent, many banks and other financial players have questioned the Fed's motives. With one main argument: while it presents opportunities for improvement, there is no single, obvious benefit that justifies the Fed launching a CBDC.

“Many of the potential benefits cited by proponents of a CBDC are uncertain and many of them are mutually exclusive and thus could not be realized simultaneously,” the Bank Policy Institute (BPI) had wisely pointed out.

A CBDC would be a solution in search of a problem. “The accessibility of cryptocurrencies, prepaid cards, fintech services, and check cashing continues to reduce the burden of being unbanked in the United States. Again, it seems that the solutions currently present are better suited to today's problems than the prospect of a CBDC in the future,” punctuates analyst Nicholas Anthony.

Letting the Fed code its own digital currency would be even worse than letting it print it out of thin air as it currently does …

In Bitcoin We Trust Newsletter: Everything around Bitcoin, Blockchain, and the cryptocurrency market