Everybody knows by now about the SHIB whale wallet (recently split the balance into more wallets) which bought USD 8,000 worth of the meme tokens last year and is now worth close to USD 3.6 Bn as of the time of writing this article. This number was even higher when $SHIB had reached its all-time high (ATH) as reported by many publications. Crypto Twitter reacted to the news with surprise, joy, envy, concern – among a mixed range of emotions.

A major concern among many was that this wallet owner could inadvertently be subjected to an unrealized capital gains tax. The US Treasury Secretary Janet Yellen has only recently hinted at the possibility of such a tax on the richest of the rich. If the proposal is passed, some of these people would receive a massive tax bill for unpaid liabilities from on-paper gains. However, it is not yet a Bill and will not impact a vast majority of people just yet.

Nonetheless, in a few months from now, another tax season will be upon us. And still, crypto accounting and taxation guidance is unclear in many jurisdictions. There is no specific standard or clear accounting code for cryptocurrencies. This is because the nature of crypto is not defined in many places – whether it is to be considered as property, commodity, currency or something else. Moreover, the dynamics of pseudonymity, airdrops, DAOs, NFTs, meme coins, mining, hard forks, rug pulls, DeFi (Decentralized Finance) etc. is unlike that seen in TradFi (Traditional Finance). It is important to note, however, that some regulators like the IRS in the US treat crypto as an asset/property.

Every tax season brings dilemmas like these for crypto degens. Haha (Meme source: r/ethtrader)

For simplicity’s sake, tax advisors recommend following the same standards of GAAP (Generally Accepted Accounting Principles) for crypto as well. Whether it is from mining, payments, airdrops, forks, trading or staking, any earning is suggested to be categorized under either ordinary income, business income or capital gains based on the nature of transaction.

Cost-basis for calculating income or gains is always as on the date of receipt of crypto. Accounting order for calculating cost is usually on a First-In-First-Out (FIFO) basis. When the holding period of an asset is 12 months or more (in the US), any gains on it are considered as long term capital gains (LTCG). For other jurisdictions (like India), holding period of 36+ months is considered for LTCG of assets.

Fiat currency-to-crypto transactions are usually considered as non-taxable events. But all crypto-to-crypto and crypto-to-fiat transactions are considered to be taxable events. Hence, by this logic, using crypto to purchase goods and services is also a taxable event. Merely moving crypto funds from one of your wallets/accounts to another one owned by you is not a taxable event though. Any donations are considered to be tax deductible for donors. Moreover, businesses can account for the cost of equipment as deductibles if mining is part of their operations.

Exhibits of why crypto tax accouching is not straightforward (source: 1, 2)

Keeping all of these pointers in mind, individual crypto users can either do their own book-keeping or use one of the many tools available online to simplify this process. There’s BearTax, TokenTax, Accointing and many more. Because of my previous familiarity with the Accointing platform, I decided to run a few accounts and addresses through it to test it out.

Accointing allows users to record crypto transactions, track portfolio over multiple time frames, and analyze the performance of each asset. This is similar to other portfolio tracking apps available in the market. The feature I found unique is the ability to classify transactions based on holding period. This helps in calculating tax liability and planning tax savings.

Accointing splits total crypto profits into short term and long term capital gains (LTCG) for any given date. On this platform, Short Term Capital Gains (STCG) refers to profits realized on assets sold within 1 year from the date of receipt/purchase, while LTCG refers to profits realized after 1 year.

One needs to first link their exchange account(s) and/or wallet address(es) and import all transactions through the Wallets -> Wallets page tab. Accointing supports over 300 wallets (including Metamask, Coinbase, Atomic Wallet etc.) and exchanges (including Binance, Coinbase, FTX, OKEx etc.). If you are squeamish about connecting your wallet, you can also add it by just entering the address in the Add Wallet page. Major blockchain networks like Bitcoin, Ethereum, BSC, Polygon, Polkadot etc. are supported.

A simple and comprehensive dashboard for crypto traders

Once all transactions have been imported, head to Taxes -> Holding Period to view a summary of all assets and their values. Drag the slider bar to any date, and you’ll see what your total STCG and LTCG will be as on that date. You can also select each asset and find its corresponding break up. Clicking on the Details dropdown for each asset provides more insights.

By knowing the breakup of STCG and LTCG for every asset, you can reduce your tax liability through loss harvesting. Click here for detailed instructions on how this can be implemented properly. After your tax calculation is complete, you can head over to Taxes -> Report to create detailed tax reports. These reports can be downloaded and used for filing.

Self-explanatory metrics for Holding Period

Accointing supports filing guidelines for US, UK, Switzerland, Australia and Germany. There are also resources available which explain how to either personally file reports or approach professional services. The holding period and tracking features (on mobile and desktop) are free-to-use irrespective of the number of transactions. The tax report is also free to generate for up to 25 transactions. For more transactions, the tax report can be generated from a paid plan.

BearTax is another popular crypto tax accounting software. Users can choose from one of the available paid subscriptions with the lowest one costing USD 10/year. There are no free plans. You can check your gains/losses for free, however.

Import all your crypto trades onto the BearTax platform, review trades, assign them the right prices, and process them using FIFO or LIFO method. Thereafter, you can generate tax documents automatically and send them to your accountant directly.

BearTax currently supports the crypto tax filing process for the USA, Canada, Australia, and India. An audit trail file is provided, which contains the entire history of transactions and taxable events. You can also schedule a private doubt clearing session with a professional accountant through the platform in case you have any questions on crypto taxation.

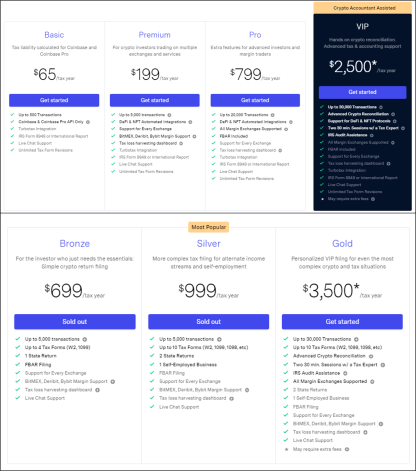

On the higher end of the pricing spectrum is TokenTax, which offers a range of paid plans with different features. There are no free plans in TokenTax and the paid plans range anywhere between USD 65/year to USD 3,500/year.

Two sets of paid plans in TokenTax - Simple Accounting (top) and Accounting + Filing (bottom)

After importing crypto transactions to TokenTax, you can track capital gains and losses, and compute tax liability for every transaction. You can also avail of the Tax Loss Harvesting tool to minimize liability.

The higher tiers of TokenTax’s subscription levels provide various professional services. For example, users can employ the services of TokenTax’s crypto tax filing team to complete the full tax return filing process on their behalf. Some of the higher plans also offer support for NFT accounting.

A professional tax suite is available as well for certified accountants and filing professionals. This can be used to generate tax reports for multiple clients at the same time.

Active traders, unlike me, should make use of the advanced features in the platforms mentioned above. But for HODLers and infrequent traders with fewer transactions, the basic plans should suffice for all reporting needs. TLDR: Get your books in order, preferably using a platform to avoid mistakes while filing. Even if you have made losses in a year or didn’t receive any payments or don’t have any taxable events, it is prudent to have the numbers in place to avoid unpleasant surprises like tax due notices. Take the help of a professional if you are unsure.

Disclosure: The author has no vested interest in any of the websites mentioned above. These do not constitute any financial advice whatsoever.

This article is a repost of my recent HackerNoon article.

Cryptocurrency and Blockchain demystified brought to you by Ghumat