Legacy credit card markets are mathematically engineered to suppress retail yield. Banks extract massive interchange fees at the point of sale, keeping the lion's share and starving consumers with arbitrary "reward points" that hold zero liquid value.

This article breaks down how Jupiter Global, running on Solana chain and integrated with Rain’s Visa network, bypasses this bottleneck to deliver a sustainable 4% baseline cashback. Users in the United States, APAC, and select European regions have an incredibly narrow window to exploit this early-bird capital incentive before the current promotional phase expires at the end of this month.

Before diving into the mechanics, it is critical to contextualize the scale of this active rollout—this is a global architecture, not a region-locked product:

- The United States (Live): Residents are the most heavily incentivized, capturing the full 4% cashback natively today, as the card's infrastructure provider, Rain, is headquartered in New York City.

- APAC & Global (Live): Non-European global regions are already actively onboarding without friction.

- Europe (Highly Selective Phase): This sovereign spend architecture is finally breaching the heavily regulated European theater, obliterating the standard 0.2% legacy yield cap. However, onboarding is strictly limited to a hand-picked list of permitted countries.

1. The Broken European Baseline

When you tap a standard European debit or credit card, the merchant pays a capped regulatory interchange fee of exactly 0.2% to 0.3%. Because the bank's revenue from the transaction is structurally suppressed, funding meaningful retail cashback is impossible. This ceiling has starved the European market of high-yield spending vehicles, leaving users trapped with arbitrary "reward points" that barely cover the cost of annual account maintenance.

Jupiter Visa Platinum card in virtual form (from July available as physical as well).

2. The Infrastructure: The Jupiter Mobile One-Stop Shop

To access the card, users must first download the Jupiter Mobile App directly from either the Google Play Store or the Apple App Store. The application acts as a dual-engine financial hub:

The Web3 Native Engine (100% Self-Custodial)

Upon installation, the app automatically generates a standard, Solana-based crypto wallet. You retain full control of your private keys. From this interface, you can seamlessly receive, send, and trade tokens across the ecosystem.

The Jupiter USDC Spend Engine (Custodial)

Sitting separately from your self-custodial wallet is the Jupiter Spend account. This specific account is not self-custodial. To use the card, you fund this account either by sending USDC directly to its generated on-chain address or by routing EUR / USD via a standard bank account transfer (there are no fees involved).

The virtual Visa Platinum card activates instantly and can be added directly to Google Pay or Apple Pay for immediate real-world use across 150M+ merchants globally.

Tap the image to watch the official Jupiter Global video on X / Twitter.

By utilizing Rain, a Banking-as-a-Service infrastructure provider and Visa Principal Member, Jupiter issues a true Visa Platinum Bank Identification Number (BIN) tied to this spend account. This provides two massive structural advantages over standard crypto cards:

Uncapped Velocity

Because the card settles directly against your on-chain USDC wallet, there are no artificial daily or annual spending limits. It enables limitless capital deployment without legacy banks restricting your transaction flow.

High-Trust Routing

Standard crypto debit cards are frequently blocked by hotels and car rental agencies due to their low-tier prepaid classification. The Jupiter card registers at the terminal as a high-trust Visa Platinum BIN, allowing merchants to seamlessly process large pre-authorization security holds without auto-declining the transaction.

3. The Strategic Trade-off: Instant USDC Yield Over TradFi Fluff

A sustainable, high-yield system requires sacrifice. Visa Platinum traditionally carries expensive insurance riders, such as rental vehicle coverage, extended warranties, purchase protection, and DragonPass lounge access. Issuers pay massive premiums to network partners to maintain these.

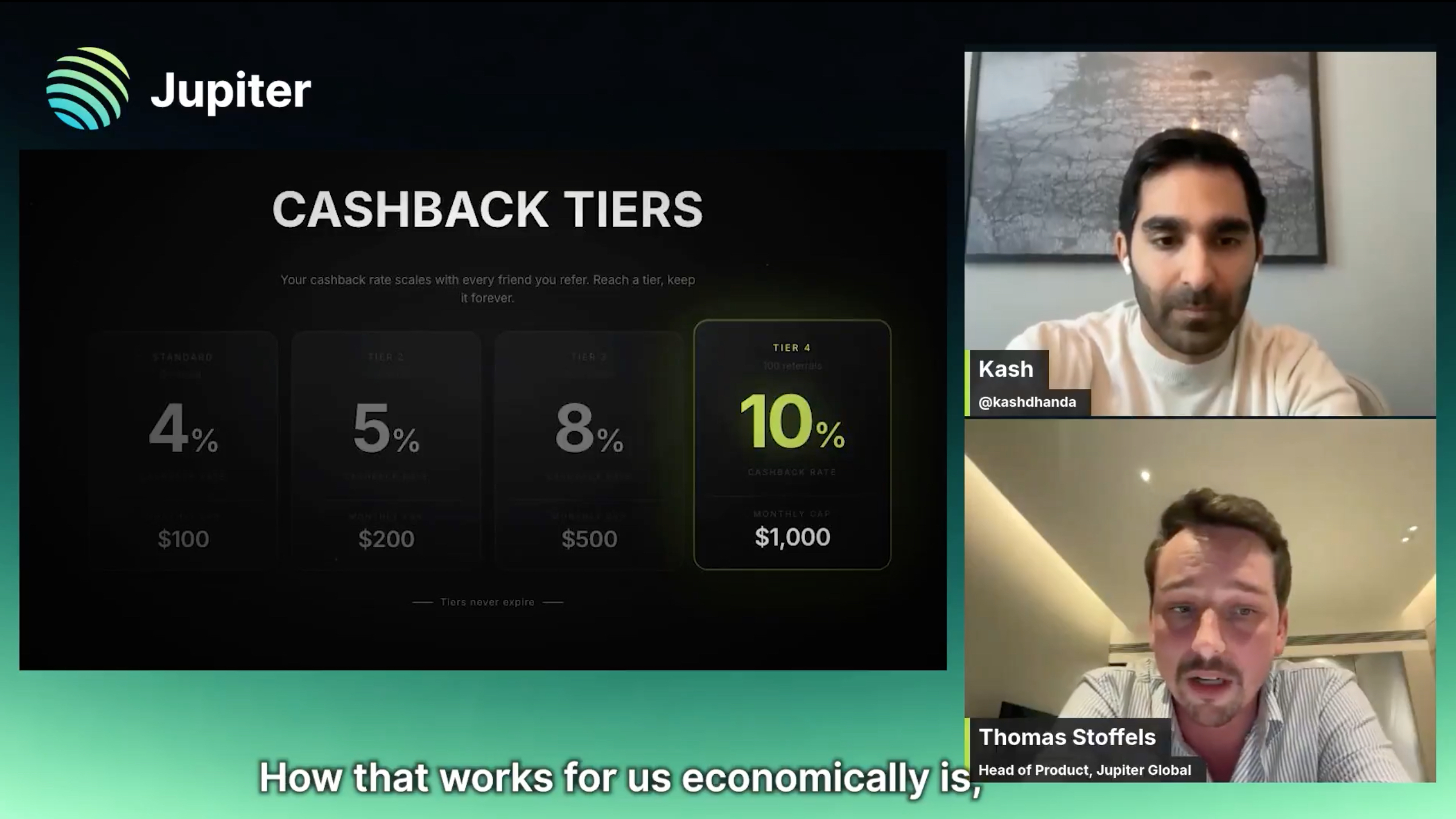

Jupiter made a strategic trade-off: they completely stripped away the traditional TradFi insurance and travel fluff. By eliminating these overhead costs, Jupiter redirects the entire premium budget into funding a massive 4% base cashback floor (which scales up to 10% via referrals).

Crucially, cashback is credited in USDC the exact moment a transaction settles. It lands instantly in your spend balance, ready to be deployed immediately for further purchases or sent back out to your self-custodial wallet. For active daily spenders, capturing raw, uncapped, instant stablecoin yield is vastly mathematically superior to an extended warranty or a lounge pass utilized once a year.

Tap the image above to watch the 1-minute breakdown of the cashback tiers on X / Twitter.

4. The Global Yield Equation

Because the card operates globally, the net profitability varies depending on the FX penalty applied by the network when converting USDC to local fiat at the point of sale. The geographic arbitrage breaks down as follows:

- The US Baseline: 0% FX fee. Users capture the full, unadulterated 4% yield on all daily USDC spending.

- The European Region: 1% FX fee. Users absorb the cross-border conversion cost but still net a 3% positive yield on every swipe, obliterating the 0.2% legacy EU standard.

- Global / APAC: 1.8% FX fee. Even at the highest penalty tier, users in Latin America and Asia net a minimum 2.2% pure profit, a rate virtually impossible to find in local TradFi markets outside the United States.

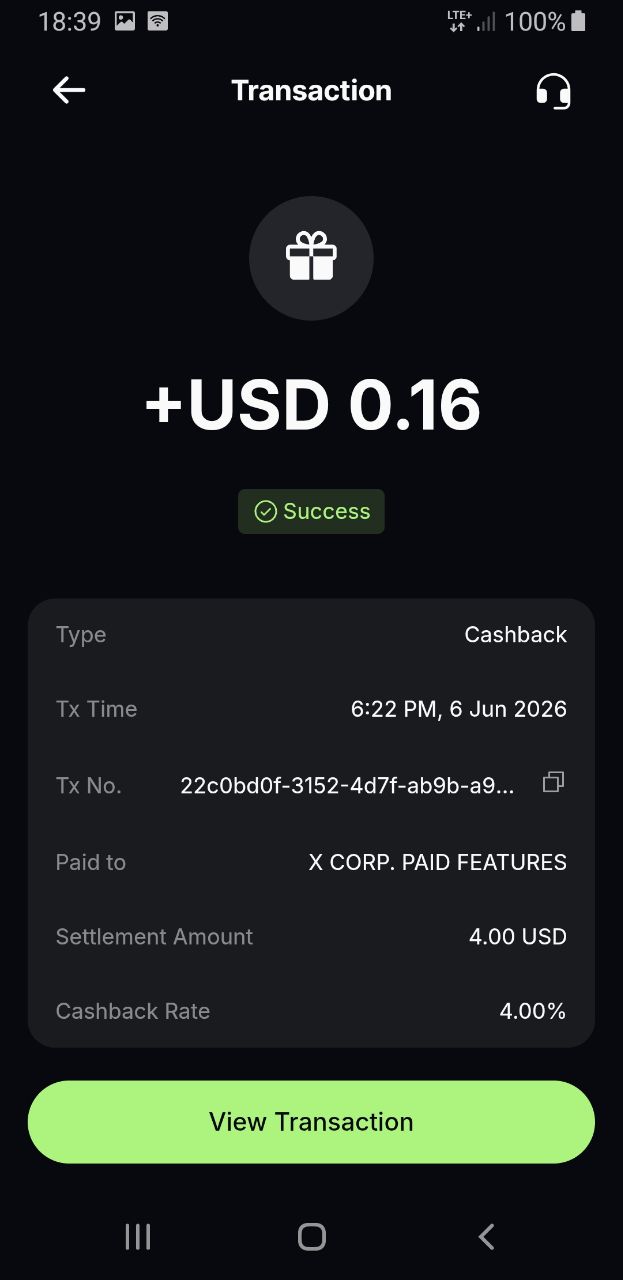

Live transaction settling on-chain: A USD-denominated subscription bypassing European FX fees to capture the pure 4% baseline.

5. The Path to Integration

The account deployment process takes less than 3 minutes and carries zero account fees. However, the onboarding landscape has shifted to manage regional compliance and strict liquidity caps:

⚠️ CRITICAL REGIONAL UPDATE: While APAC regional onboarding remains open without friction, Europe is operating under tight country-level ringfacing. Right now, ONLY residents of the following select nations can successfully bypass the waitlist and onboard onto the system: Canada, France, Greece, Indonesia, Italy, Netherlands, Portugal, Spain, Switzerland, United Kingdom.

The End-of-June Identity Deadline

The current early-bird promotion is live only until the end of this month (June 30th). If you are a referee looking to secure the high-yield capital incentives, there is an absolute clock on your deployment:

- Complete KYC by June 30th: You must register and completely finish your identity verification (Know Your Customer) before the calendar turns to July. Failure to complete KYC by this deadline disqualifies your profile from locking in the promotional campaign parameters.

- The 30-Day Spending Clock: The moment your KYC is fully cleared and verified, a personalized, internal 30-day countdown timer activates. You are granted exactly 30 days from your specific clearance date to reach a cumulative spending threshold of $1,000.

To put this math into a tangible perspective: the $1,000 spend requirement is entirely cumulative. If a resident routes the purchase of a new $1,000 laptop through the card, or simply accumulates that same amount organically via groceries and utilities over their activated 30 days, they capture the $40 native baseline yield (4%) plus the $100 early-bird bonus simultaneously. That creates an effective 14% return ($140) instantly credited in USDC. For both high-ticket deployment and standard daily routing, this completely overrides the utility of legacy point systems.

This exclusivity is a massive structural advantage for early adopters looking to capture the initial liquidity incentives. Entering the invite code RDLJCPH9 during the initial setup does not instantly print a virtual card across all of Europe for everyone today. Instead, for the authorized countries listed above, it places you securely in the priority queue and hardcodes your eligibility for the $100 early-bird bonus. This bonus unlocks upon clearing your $1,000 cumulative spend target within your active 30-day window, stacking directly on top of your standard nominal cashback. You earn both simultaneously.

Take action and download the app, enter code RDLJCPH9, and clear your KYC before the end of June to start your 30-day spend timer.

For more intel on blockchain tech, crypto & market insights from the perspective of {meta}cognitive and behavioural economics but not only, join me at my X / Twitter account and follow at Publish0x.