Remember when we all cheered because BlackRock, Apollo, and the rest of Wall Street finally decided to play in our sandbox? Real World Assets (RWAs) were supposed to be the ultimate bridge. The pitch we were sold was intoxicating: bring trillions of dollars in yield-bearing physical assets on-chain, legitimize decentralized finance once and for all, and everyone gets rich.

But dig into the on-chain data. Look closely at what these institutions are actually doing with these tokens. That utopian narrative falls apart fast.

They aren't just using the blockchain for secure, transparent custody. They are weaponizing DeFi’s composability. What we are witnessing is the construction of an unregulated, hyperscaled shadow banking system built right on top of our permissionless liquidity pools. Wall Street is importing its toxic, off-balance-sheet leverage directly into Web3. And if you aren't paying attention to the mechanics of this trap, you are going to be their exit liquidity.

The Private Credit Shakeout: Backing Tokens with Bad Debt

If you want to understand the trap, you have to look at the collateral.

Right now, the $1.8 trillion traditional private credit market is bleeding through a severe, prolonged shakeout. Even Apollo Global Management CEO Marc Rowan is sounding the alarm, warning of a "race to the bottom" in lending standards driven by a massive overexposure to software-as-a-service (SaaS) companies.

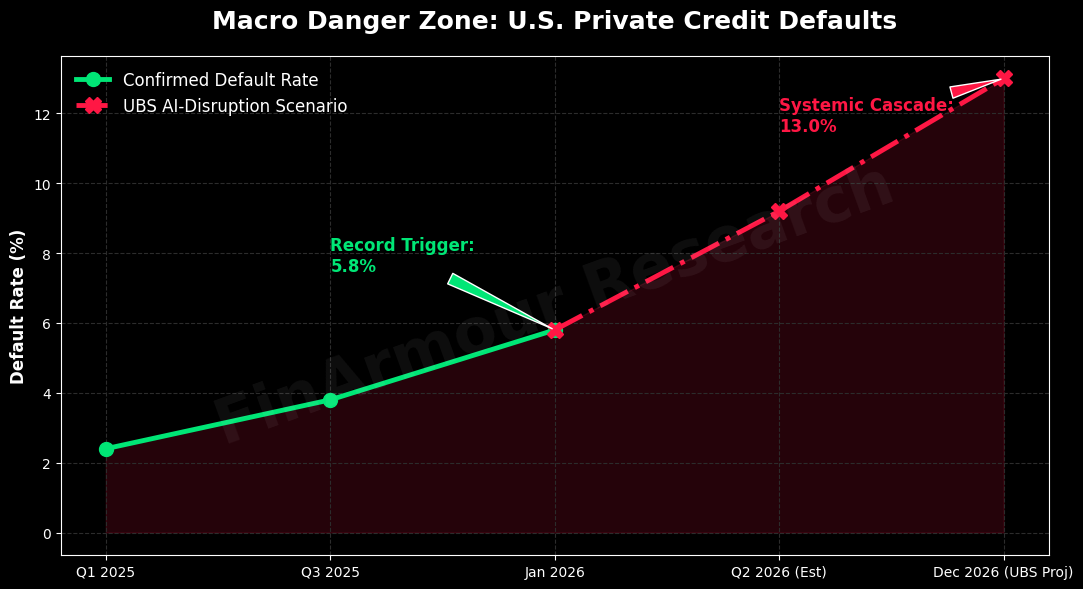

The empirical data is absolutely terrifying. By January 2026, the U.S. private-credit default rate hit a record 5.8%. And it gets worse. Macroeconomic models out of UBS are projecting an aggressive disruption scenario where AI implementation could push that default rate to a staggering 13% before the year is out.

When these corporate borrowers default in the real world, the off-chain credit funds take a massive capital hit. How do non-bank lenders hide this? They allow distressed borrowers to pay via "payment-in-kind" (PIK) interest instead of actual cash. It’s a classic accounting trick to maintain a facade of solvency. But here is the kicker: those exact distressed funds are now being digitized, tokenized, and deployed as core collateral across DeFi.

Think about it. If the fundamental physical collateral backing decentralized loans is rotting away, the blockchain protocols are facing a mathematically guaranteed chain reaction of undercollateralization.

Leveraged Looping and the ERC-3525 Disguise

So, how does the rot spread? Through a programmatic cycle institutions politely call "folding." The rest of us call it leveraged looping.

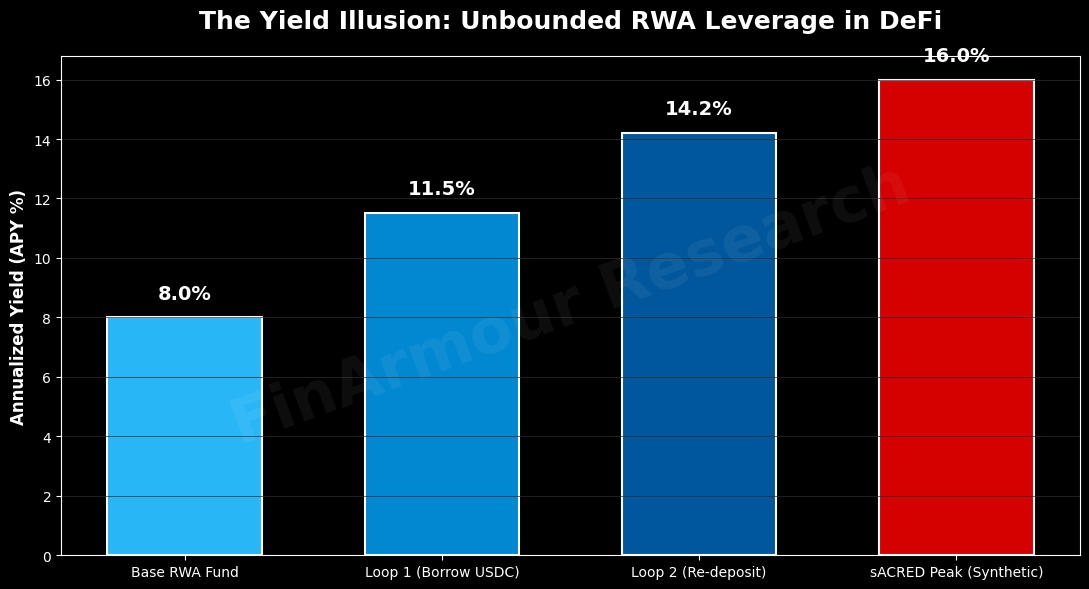

Here’s the playbook. An institutional player takes a tokenized private credit fund—maybe yielding a modest 8% to 12%—and drops it into a decentralized money market like Morpho, Kamino, or Drift. Against this collateral, they borrow a stablecoin like USDC. Then, they instantaneously route those borrowed stablecoins right back into purchasing more of the exact same yield-bearing RWA token. Deposit it again.

Rinse and repeat.

Take Apollo’s tokenized credit fund (ACRED) and its smart wrapper, sACRED. Investors are utilizing this within DeFi protocols to engage in recursive looping strategies, artificially amplifying base private credit yields up to an astonishing 16%. Let’s call it what it is: pure, unbounded off-balance-sheet leverage.

But it gets darker. They are recreating the 2008 Mortgage-Backed Securities (MBS) crisis down to the exact technical details. Back in 2008, Wall Street bundled sub-prime mortgages into highly rated CDOs. Today, developers are using the ERC-3525 semi-fungible token standard to achieve the exact same obfuscation. Smart contracts use the "digital container" feature of ERC-3525 to slice highly non-standard, illiquid private credit into senior, mezzanine, and junior tranches.

The underlying default risk is completely abstracted away from the retail investor. All you see is a shiny, highly-rated senior token.

The Physical-to-Digital Air Gap

Here is the fatal structural flaw in the entire RWA thesis: the timing mismatch.

DeFi operates on block time. Smart contracts execute transactions, trigger algorithmic margin calls, and force liquidations in a matter of milliseconds. But the actual physical assets backing those tokens? They settle on analog time. Liquidating a commercial loan takes days, weeks, or even months.

Because physical assets require subjective human appraisals and quarterly NAV updates, we rely heavily on decentralized oracle networks like Chainlink to feed pricing data on-chain. But oracles lag when dealing with illiquid real-world assets.

If a corporate borrower defaults off-chain on a Tuesday, the blockchain doesn't immediately know. The RWA token effectively becomes a "zombie asset." It keeps trading at a false premium in your favorite DeFi liquidity pools until the oracle finally publishes the delayed NAV update.

And when that oracle finally flashes the devaluation to the ledger? The smart contract doesn't pause to negotiate a workout. It doesn't care about market conditions or human forbearance. It simply liquidates.

The deUSD Contagion: A Post-Mortem

For anyone who thinks this systemic risk is just theoretical FUD, I suggest you look at the corpse of Stream Finance.

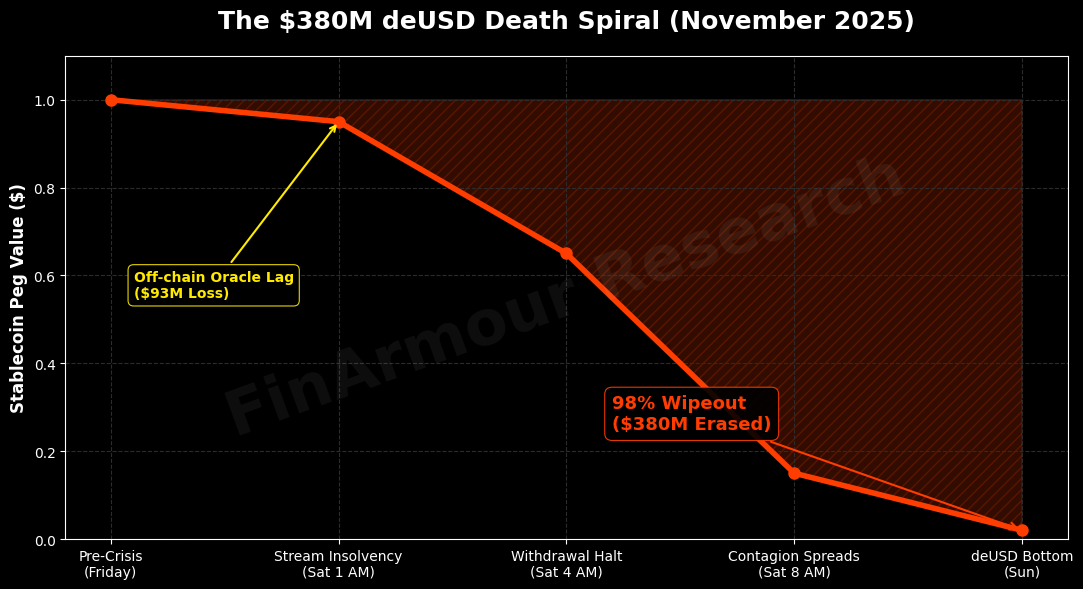

In November 2025, the theoretical dangers of RWA contagion materialized with devastating velocity. Stream was operating a massive synthetic asset protocol issuing derivative tokens (like xUSD) backed by on-chain collateral but pegged to off-chain yields. An external, off-chain fund manager responsible for generating these yields managed to lose $93 million over a single weekend trading anomaly.

Because DeFi thrives on absolute composability, Stream’s synthetic tokens had already been aggressively rehypothecated. Independent on-chain analysts from the YieldsAndMore (YAM) collective mapped out a staggering $285 million contagion web. Those toxic xUSD tokens were deeply entangled as foundational collateral across seven different blockchain networks, hitting major protocols like Euler, Silo, Morpho, and Sonic.

The most devastating blow fell upon Elixir Network’s deUSD, which had massive exposure to Stream. When Stream recognized its insolvency and halted withdrawals, the contagion spread instantly. The deUSD stablecoin lost its peg immediately, collapsing by 98% in a matter of hours.

Nearly $380 million in value was erased across interconnected protocols in a single weekend. It proved, definitively, exactly what happens when you back algorithmic and yield-bearing stablecoins with opaque, concentrated corporate risk.

The Inevitable Liquidation Cascade

Let’s stop pretending. The trillion-dollar RWA sector is not a transparent foundation for a new financial paradigm. It is a meticulously interconnected debt trap designed to privatize gains during the bull run and socialize the catastrophic losses when the music stops.

When an RWA token de-pegs due to a delayed oracle update or an off-chain default, algorithmic margin calls will drain stablecoin liquidity pools across decentralized exchanges in seconds. This creates a massive, violent spike in decentralized borrowing rates. The forced selling of on-chain assets will further depress their price, triggering subsequent layers of algorithmic liquidations. It is a self-fulfilling death spiral.

Institutions and DeFi platforms are treating RWA tokens as highly liquid cash equivalents simply because the digital tokens themselves trade 24/7. This is a fatal macroeconomic misconception. Leverage without underlying liquidity is an absolute liability.

The corporate default rates are rising. The underlying real-world collateral backing the DeFi ecosystem is quietly rotting away. When the timer finally runs out, there will be no centralized circuit breakers or bailouts to save the market.

Make sure you know exactly what is sitting in your liquidity pools before the algorithm decides to sell.