Generally speaking, when a poker player, goes “All-in”, it’s because he/she is confident that they have a winning hand. Going all-in usually has one of two outcomes. You’ll either win big or you’ll lose it all.

Well after much research I’ve decided to go all-in on crypto.

Now before you deem me a degenerate gambler, hear me out. All-in for me won't leave me destitute if it doesn't work out.

While I do have the utmost confidence in block-chain technology and it's future impact, my decision to go all-in on cryptocurrency isn’t some foolish bet on the price of Bitcoin.

Allow me to explain.

When I say I’m all-in on crypto, I mean, besides my work retirement, I no longer invest in the stock market, and I convert all of my dollars into stable-coins (crypto assets pegged to the U.S. dollar). Specifically the stable-coin, $USDC.

$USDC is owned by the federally regulated Coinbase exchange, and runs on the Ethereum blockchain. Each individual $USDC token is backed by an actual U.S. dollar held in a reserve bank account which is continually audited and is insured up to $250,000 per person.

Ok... but why?

There are 3 reasons I made this decision

1. Passive investments: $USDC along with The Coinbase Card, allows me to passively invest in crypto. When you convert your dollars into $USDC on Coinbase, you can spend it using their VISA debit card.

Each purchase is rewarded with 4% cash back, paid in your choice of a list or crypto assets. I choose to collect my 4% in Stellar Lumens ($XLM) and convert it to whatever other crypto I’m bullish on or send it to another exchange, as its one of the fastest and cheatest crypto assets to send.

I use my Coinbase card from everything from bills to gas and groceries. By doing so, I’m building a portfolio of crypto assets as a byproduct.

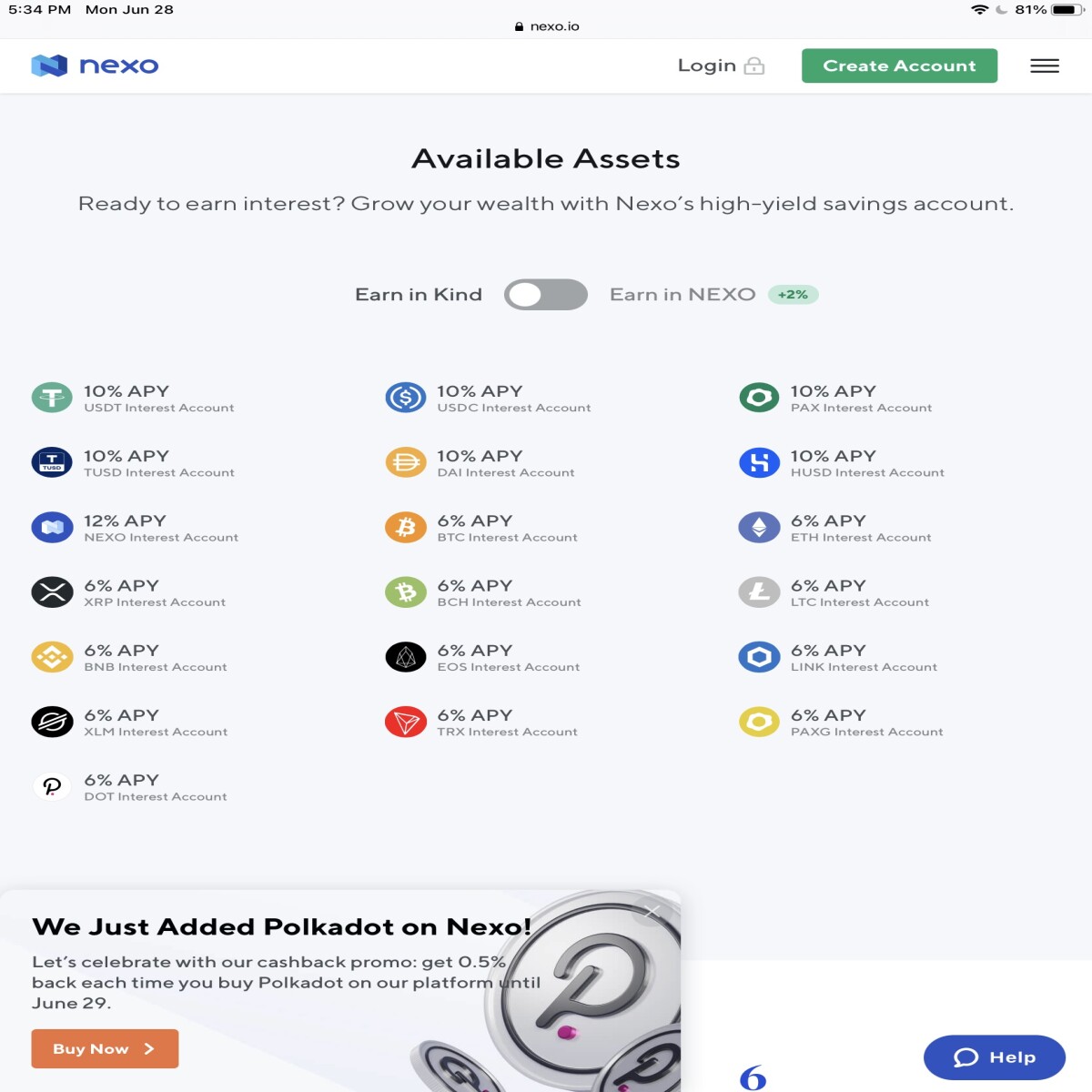

2. Interest rates: Things get exciting when you move $USDC off of Coinbase. By moving $USDC onto a platform that offers loans collateralized by crypto deposits, you can earn 8%- 12% interest on stable-coins.

Just holding $USDC on Coinbase pays an interest rate of 0.15% APY.

That's nothing to get excited about, but seeing as though I essentially use Coinbase as a checking account, it beats the absolutely nothing that I get from my actual checking account.

Below is a list of 5 platforms that offer at least 8% on $USDC deposits. These platforms can double as a savings account for your $USDC.

There are potentially higher interest yield for stablecoins available in De-Fi. I wrote about this in another blog, “The Early Bird gets the Worm”.

3. Undervalued crypto Investments: By the time a crypto project hits Coinbase's radar, it’s usually relatively mature.

There are many amazing projects being built, that have yet to have their day in the sun. They’re usually found on smaller exchanges such as Kucoin or decentralized exchanges such as Sushi Swap

Having $USDC readily available gives me the ability to deploy capital to places inaccessible by the U.S. dollar and invest in these earlier stage Gems.

FYI I specifically mentioned KuCoin here because part of their mission statement is to find undervalued crypto “Gems” and add them to their exchange. That’s a story for another day.

This may not be the most popular financial strategy, but it makes sense to me and that’s all the confirmation I need to go for it.

I’ll leave you with one of my favorite quotes.

“In order to lead the orchestra, you must first turn your back to the crowd.”

Thanks for reading :)

***

All feedback is welcomed. Tell me if you agree or why I’m crazy.

TIP Jar

ETH / ERC 20’s

0x91e4797a91BAC4D5B0b4dC4f24C66d48C185B2BB

BNB

bnb16n92g0qeefhpyemp9nuqkdtq6ljr5zyt6ke9cz

BTC

bc1q64cqp8g6fkx0vuwvgf6r9ya5n59w3a0dv2l3pu