Overview

The Maker (MKR) token was created by MakerDAO (2014) and its principal purpose is to underpin and secure the DAI token which launched in 2017. MKR is also used as a governance token for participation in the governance decision associated with the Dai ecosystem. Holders of MKR make key decisions on the operation and future of the system.

The Maker ecosystem contains two cryptocurrencies. The first, called Dai, is a crypto-backed cryptocurrency and the flagship product of the Maker ecosystem. Maker is a Distributed Autonomous Organization (DAO) on the Ethereum blockchain with a platform designed to keep the DAI price stable. MakerDAO uses the MKR token to act as a counterweight to price fluctuations. This combo is the basis of a simple crypto banking system built on blockchain technology that allows for simpler international payments and peer-to-peer transfers.

Maker Strengths

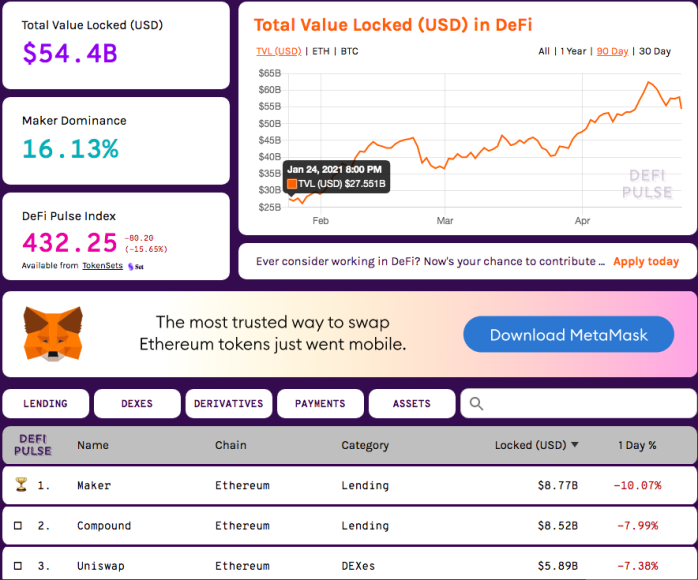

- Maker is one of the first DeFi projects and still currently boasts the highest total value “locked” (TVL) in a DeFi application at ~$8.7 billion.

- DAI is the leading decentralized, permissionless, trustless stablecoin that plays an integral role in Ethereum’s DeFi ecosystem with ~$3.5 billion in circulation. It remains the top choice for anyone looking to transact in a stablecoin without a trusted third-party.

- Over 400 apps and exchanges now use DAI and DAI has become a common trading pair within the DeFi ecosystem.

- Maker continues its commitment towards the full decentralization of MakerDAO with the transfer of MKR token control from the Maker Foundation to Maker governance in March 2020.

Maker Weaknesses

- The historic March 2020 Ether price collapse and subsequent network congestion proved to be a long-tail systemic risk to Maker at the time. The system essentially did not perform as intended and allowed some users to lose all their collateral.

- The issuance of new MKR after the fallout of March 2020 undid years of MKR value accrual and also illustrated the possibility of future MKR holder dilution in the future.

- Regulatory clarity around the MKR token is non-existent but a strong case can be made for it to be deemed a security under the US Howey Test.

- In a move to reduce dependence on solely Ether, Maker now accepts multiple assets as collateral, including centralized stablecoins and assets. Introducing centralized collateral may reduce price volatility but opens up new censorship attack vectors.

- Because DAI’s stability is predicated on over-collateralization and incentive mechanisms within the Maker system, it exhibits more volatility than its fiat-backed counterparts and rarely trades at exactly $1.

Important Links

- MCD Whitepaper

- Purple Paper

- Github

- Medium

- More

- Wallets - Ledger and TREZOR

- Where to buy? Coinbase and Gemini

Use Case

The Maker ecosystem contains two cryptocurrencies. The first, called Dai, is a crypto-backed cryptocurrency and the flagship product of the Maker ecosystem. Maker is a Distributed Autonomous Organization (DAO) on the Ethereum blockchain with a platform designed to minimize price fluctuations in its own stablecoin, Dai, against the US dollar. This combo is the basis of a simple crypto banking system built on blockchain technology that allows for simpler international payments and peer-to-peer transfers. Maker (and Ethereum) creates a decentralized, peer-to-contract lending platform by locking Ether into a smart contract as collateral and then minting the stable coin, Dai. Dai's stability is achieved through a dynamic system of collateralized debt positions, autonomous feedback mechanisms, and incentives for external actors. Once generated, Dai can be freely sent to others, used as payments for goods and services, or held as long-term savings.

Maker (MKR) claims the distributed stabilization section allows “anyone, anywhere” to use Dai freely and confidently, assured that it will maintain purchasing power. A stable digital currency enables the next generation of financial applications which were currently precluded by the industry's infamous volatility.

The Maker contract is one of the largest decentralized applications (dApps) on the Ethereum blockchain. It is the first decentralized finance (DeFi) application to be significantly adopted and was designed by a variety of contributor groups including Maker Foundation developers, external partners, and other individuals.

Maker’s main function is to underpin MakerDAO’s stablecoin, Dai. Dai is described as a decentralized, permissionless, collateral-backed cryptocurrency soft-pegged to the US dollar. Dai is held in cryptocurrency wallets or on trading/exchange platforms and is supported on Ethereum’s blockchain. MKR is MakerDAO’s secondary token, serving as the administration token of the MakerDAO ecosystem. MKR is needed for paying the fees accrued within MakerDAO’s ecosystem. The dual token concept was created to align incentives to better help maintain price stability and address the prior issues surrounding an open, decentralized stablecoin.

Dai provides a solution to counterparty risk by creating an over-collateralized stablecoin in which its solvency is not reliant upon trusted third parties. All Dai is backed by Ether that is held in public, transparent smart contracts on the Ethereum blockchain. This allows any user to verify the system’s health/backing in real-time, unlike the legacy financial market. Additionally, users can transact with one another in a peer-to-peer (P2P) fashion anytime and from anywhere without the need to trust a bank or counterparty.

Decentralized Finance (DeFi) governance tokens, like MKR, are proving to be a big disruption to the financial system. Powered by blockchain technology, this new wave of applications and services could help bring financial services to the underbanked, reduce transaction costs, and enhance security, all while providing users a seamless experience from anywhere in the world.

Technology

MKR is an ERC-20 token on Ethereum and thus cannot be mined. Instead, it is created (and destroyed) in response to Dai price fluctuations to keep the Dai price around $1. MKR is used to pay transaction fees on the Maker system and it collateralizes the system. It stabilizes the value of Dai through a dynamic system of Collateralized Debt Positions (CDPs), autonomous feedback mechanisms, and appropriately incentivized external actors.

In order to take out a loan or “vault” within the Maker system, users must deposit any of the several accepted crypto-tokens into the Maker vault and then are able to borrow Dai against the value of those tokens. Typically, the collateral must be at least 150% of the value of the loan. The protocol then charges borrowers a stability fee for borrowing Dai. This fee is variable and subject to the discretion of Maker governance. Ultimately, the stability fees collected by all the Dai loans are used to buy MKR from the open market and then burn it. This stability fee/burning mechanism is the primary source of value accrual for MKR.

This new automated lending service could help to bring financial services to the underbanked, enhance security, and reduce transaction costs.

Dai is an ERC-20 token that is built and exists on the Ethereum blockchain, and thus, Ethereum provides the infrastructure for consensus. Dai is a credit created from Maker vaults that’s soft-pegged to the value of the US dollar.

Maker controls the Dai-USD peg with its Target Rate Feedback Mechanism (TRFM). The Target Rate determines the price changes needed for Dai to reach the Target Price of $1 during market volatility.

Maker requires oracles to provide real-time market price information to the system to adjust the Target Rate when needed. Oracles and Global Settlers are external actors and not native to the platform. Another key exogenous actor in the Maker ecosystem is Keepers. Keepers are independent entities, incentivized by profitable opportunities within the Maker system to contribute to the system. Keepers can also make a profit trading Dai and arbitraging the spread when Dai deviates from its $1 peg.

MakerDAO protocol, being an Ethereum dApp, is subject to the blockchain’s latency. The current block time of Ethereum’s blockchain is ~10 seconds with the network able to process ~15 transactions per second.

Economics

Maker (MKR) is the governance token of the MakerDAO and Maker Protocol— a DAO and a software platform, respectively. Both are based on the Ethereum blockchain— which allows users to issue and manage the Dai stablecoin. Initially conceived in 2015 and fully launched in December 2017, Maker is a project with the task of operating Dai, a community-managed decentralized cryptocurrency with a stable value soft-pegged to the US dollar. MKR tokens act as a kind of voting share for the organization that manages Dai. While Maker does not pay dividends to its holders, it does give the holders voting rights over the development of Maker Protocol.

MKR is an ERC-20 token, meaning that it runs on and is secured by the Ethereum blockchain. Ethereum, in turn, is secured by its Ethash proof-of-work function and is subject to the gas fees of the Ethereum network. As of Q2 2021, ~3% of the ETH supply is locked up in Maker.

All accrued fees on MakerDAO are paid in MKR. The protocol purchases MKR off the secondary market and burns it, ensuring proper alignment incentive between MKR token holders. The burning of MKR reduces its supply in circulation through its intentional destruction. It is an effective method for increasing and stabilizing the price of MKR with the increased value given to the holder resembling that of a dividend.

MakerDAO Protocol token burning is a cyclical function for MKR. During these times, MKR is destroyed to balance Dai’s supply to keep Dai’s peg to the US dollar aligned when demand is low. At times, these events can be profitable. Overall, the general tokenomic of MKR is weighted and balanced with Dai. Seeing that Dai is the most trusted, non-fiat-backed stablecoin in the cryptoverse, MKR is sure to stay relevant in the DeFi space.

With demand for stablecoins increasing, and the interest rate for borrowing Dai now sitting above zero, yield seekers have more of an incentive to hold MKR, as it can generate revenue in the form of interest repayments. Whether or not it continues to hold this price remains to be seen, but it is clear that the MKR token was well overdue to regain some of its lost ground against the rest of the DeFi market.

Because MKR did not conduct an ICO, it is not subjected to the same kind of selling pressure that other projects may face. Venture Capitalists are more than likely to have the patience to allow startups, like MakerDAO, to flourish over time, unlike ICO investors who seek immediate returns. This causes problems for early investors when early market performance for a token or coin is bombarded with sale orders of ICO investors dumping on the market, crippling early investors as well as their portfolios.

Governance

MKR is the governing token of Dai. MKR holders stake MKR and govern the Maker Protocol which sets standards for both MKR and Dai. This staking in the MakerDAO ecosystem allows holders to approve new assets as potential collateral as long as they adhere to the subject risk requirements, parameters, and safety measures of Dai (e.g., liquidation ratios, stability fees, savings rates, and debt ceilings). The decisions that the holders make affect what kind of assets can be locked into the Dai network. These measures enable the MakerDAO’s governance of the Dai credit system. The holders of MKR become stakeholders and are the decision-makers in its broader ecosystem from fiat-collateralized stablecoins that are soft-pegged to the US dollar.

Furthermore, stakeholders have many other responsibilities like reaching consensus on important community goals and evaluating views on executive voting proposals. Stakeholders ratify governance proposals originating from the MakerDAO forum signal threads, determine the values of system parameters that will be put to an executive vote, and ratify risk parameters for new collateral types as presented by risk teams.

MKR holders can cast votes, the results of which impact the overarching MakerDAO system. Votes are tallied on the amount of MKR that votes for a change, not the number of MKR holders. While stakeholders are participating in a vote, their MKR is locked into a voting contract. Users can go to the official website to participate in and/or monitor current votes. Historical voting results and stats around voting participation can be found here.

Work towards full decentralization of MakerDAO continued with the transfer of MKR token control from the Maker Foundation to Maker governance in March 2020. By April 2020, community discussions and governance calls took place about the best way to maintain a fully decentralized Maker Protocol and become completely responsible for every aspect of the DAO. MKR stakeholders can also participate in governance polls which are used to gather community sentiment about potential changes.

Vulnerabilities

Two major MKR vulnerabilities were reported by media outlets in 2019, but both were resolved shortly after they were brought to attention.

In the spring of 2019, blockchain security group Zeppelin and cryptocurrency exchange Coinbase audited the Maker Voting Contract. As a result of the audit, Zeppelin disclosed a vulnerability that would have allowed tokens to be permanently locked within the MakerDAO voting contract. As a result, Maker updated the contract.

In the fall of 2019, Micha Zoltu published a blog post about how an individual with 40,000 MKR could steal all of MakerDAO’s collateral. As mentioned in the Governance section, a substantial holder of MKR can have more weight in votes than many small, individual holders. As such, while this vulnerability was active, an individual could have compiled more than 50% of MKR and created an executive contract to steal MakerDAO’s collateral, then approved it on their own, and had the results take effect immediately. As such, there is now a 24-hour hold placed on such activities.

Maker launched a bug bounty program on HackerOne in July 2019. HackerOne lists the average bounty for Maker Ecosystem Growth Holdings as between $250 and $500. In November 2019, MakerDAO raised bounties to $5000 for bugs of medium severity, $10,000 for bugs of high severity, and $100,000 for bugs of critical severity.

A more recent and consequential vulnerability was discovered on March 12, 2020, known as “Black Thursday.” On this day, Ethereum (ETH) saw a dramatic price drop, losing ~30% of its value in approximately 24 hours. During the sell-off, the Collateralized Debt Position (CDP) started to automatically liquidate as Ethereum fell at a record pace. Some owners of liquidated loan positions received none of their Ethereum back. Again, the CDP liquidation process is supposed to cost approximately 13% of the collateral, not 100%. The 0% return in CDP collateral was a shortcoming caused by a combination of two things: 1) the deviation between ETH's value as interpreted by the oracles and the actual market price, and 2) network congestion. This resulted in liquidators of loans (known as "Keepers") failing to properly sell the collateral.

After some time, some clever market participants realized they could get transactions through but with a bid of $0 on the collateral instead of the fair value. Since the network was so congested, these were the only bids and they won the auction, meaning some individuals paid nothing for millions in free assets. Many vaults that were up for partial liquidation were fully liquidated and since the collateral was given away for free, there was no Dai left to pay off the debt of liquidated borrowers.

While not a vulnerability, one final downside to the MKR/Dai system is that Dai carries more volatility than other stablecoins. While it can trade below $1, Dai has regularly traded above $1, creating the term “Dai Premium.” If Dai is greater than $1, selling any other cryptocurrencies for Dai will result in less of that asset compared to simply selling for USD or another stablecoin with a lesser premium. This creates the obvious choice to not sell into Dai when given another choice.

Network Effect

MakerDAO has an active forum that garners thousands of views. As of Q2 2021, they also have a Twitter presence of more than 80,000 followers and more than 6,000 members in their Telegram channel. A subreddit about the topic of MakerDAO has 18,500 subscribers, as of the time of writing.

The MakerDAO forum discussions tend to be strongly related to MakerDAO governance, as well as technical discussions and suggestions. Whereas, the MakerDAO subreddit tends to contain more informal, conversational discussions, including commenting on recent news and asking questions about getting involved in the MKR and Dai community.

According to CoinGecko, MKR ranks #35 globally in terms of MarketCap and is available at 100 exchanges at the time of writing, including Binance, Gemini, and Coinbase Pro. As of Q1 2021, 995,762 MKR are in circulation, with a max supply of 1,005,577 MKR. The price of Maker as of Q1 is $1,467 with a market cap of $1,458,988,621 and a trading volume of $180,858,970.62 over 24 hours.

Maker also holds the honor of having the most total value “locked” (TVL) in a DeFi application at ~$8.7 billion.

Total Value Locked (TVL) of top DeFi projects. Image credit: DefiPulse

The Maker Foundation gives grants to select blockchain projects that support the use of Maker and DeFi. Some of the projects funded by Maker Foundation grants include GSN and PoolTogether.

As for Dai, the overall Dai supply has seen explosive growth since inception, specifically in 2020. In November 2020, Dai market cap surpassed $1 billion and in Q2 2021, it now sits ~$3.6 billion. Over 400 apps and exchanges now use Dai and Dai has become a common trading pair within the DeFi ecosystem.

Team

The Maker project and team are a respected group in the crypto and blockchain community and have considerable respect within the submarkets of DeFi.

Rune Christensen is MakerDAO’s Executive Officer and Co-Founder since its beginning in 2013. Rune also co-founded Try China, a company providing international recruiting, after studying International Business at the Copenhagen Business School. In Maker’s early development, Rune would hold radio talks lasting hours discussing his vision of decentralized finance (DeFi).

Steven Becker is the President and COO of MakerDAO. Steven received both his Bachelor of Business Science in Finance (with honors) and Master of Science in Financial Mathematics degrees from the University of Cape Town. Before establishing Maker, he founded Cubit Capital, a financial planning and investment advising company in 2012. Steven also operated as an Executive Director/CEO and Shareholder at Polus Capital, an investment management company that provides “entrepreneur-friendly” capital to growing businesses.

Mariano Conti is the head of smart contracts at MakerDAO and remains a public figure and advocate for the MakerDAO project.

Prominent investors in the project include Polychain Capital, Dragonfly Capital, a16z Crypto, Placeholder, and others. One can stay connected to this project via the website chat, events, and forum. They also have a relatively moderate presence on Twitter, Telegram, and Github

User Experience

Maker is an ERC-20 token built on the Ethereum network, so it is supported by any wallet that supports Ethereum. The most popular hot wallets include MetaMask and MyEtherWallet, while Trezor and Ledger remain the most notable hardware wallets. Transaction speeds and cost largely depends on Ethereum network traffic, but one can expect considerably quick and easy transactions compared to other blockchain networks. However, MakerDAO and Dai are only supported by Ethereum which limits its potential adoption and user’s options when interacting with MKR.

Maker and Dai support an ecosystem of financial services and the project’s blog is a fantastic user resource for learning and following all of their products and services. Additionally, the GitHub page clearly explains basic concepts, terminology, how to vote, etc. This includes Oasis- trading tokens, borrowing Dai, and earning interest. Governance, voting on changes, and current polls have their own forum. Migrating from SCD to MCD, managing deposits and collateral positions, and opening new vaults can be done from the main website as well. Additionally, third-party dashboards like InstaDapp, Zerion, and Zapper are a user-friendly way to take out and pay back loans. In October, a major update to the MakerDAO voting portal was released making it easier than ever for MKR holders to cast votes. Users can go to the official website to participate in and/or monitor current votes.

The site Dai Stats helps users follow the progress and health of Dai with stats like the stability fee, collateral types, collateral ratio, etc.

Regulation

Governments around the world have put forth very few statements about how they view and will regulate tokens other than Bitcoin and Ether. Smart contract tokens remain very new, niche, and foreign to most agencies still trying to understand the technology. While no official statements have been made about MKR, the SEC has commented on Ethereum (twice) – in conjunction with Bitcoin – declaring it is not a security. This is important for MKR, as it is built atop Ethereum and (eventually) Ethereum 2.0. The CFTC Chairman also publicly stated in October 2019 that Ether is viewed as a commodity by the U.S. regulatory body. However, in 2021 a new presidential regime with a slate of new regulatory leaders came into power which poses some uncertainty on whether they will continue ruling in line with the prior statements or have new interpretations.

According to the Howey Test, the strongest argument for MKR being classified as a security is its dependence and centralization around the “common enterprise” and “third party,” the Maker Foundation.

The Securities Framework Asset Ratings of the Crypto Rating Council (CRC) scored the MKR token a 4.5 out of 5 (5 equating to a security) and Dai a 1. They explain their rankings with the following: “In Multi-Collateral Dai, MKR is a governance token and a recapitalization resource. While Dai acts as the stablecoin created by users who provide their assets as collateral...(MKR) was sold privately to venture and crypto-affiliated investors. The Maker Foundation plays an ongoing role in supporting MakerDAO and the associated MKR and Dai network and community of owners, users, and holders supporting the Maker Protocol.”

Separate from MKR and securities law, the very idea of stablecoins or “crypto dollars” has recently come under attack from US regulators which, if passed, would essentially preclude Dai from continuing to exist as is. The STABLE Act was proposed in December 2020 and was written with “the intent to prevent abuse, opacity, and the potential rise of a stablecoin-based shadow-banking system.” However, the obligations that stablecoin issuers would have to abide by to avoid breaking the law are incredibly cumbersome and/or restrictive.

Road Map

MakerDao has made significant strides since it fully launched in 2014, most of which came in the last couple years. Dai represents the first stablecoin on the Ethereum protocol and has seen a dramatic rise in adoption since its release in 2017.

MCD’s stability, composability, and permissionless ability propelled this project as one of the most used cryptocurrencies in the DeFi space. Coinbase Commerce, a popular platform that helps small businesses adopt decentralized cryptocurrency payments, integrated Dai as a payment method in February 2020.

The amount of existing Dai reached 1 billion on November 13th 2020, five years after the announcement of the project and currently sits around ~3 billion.

The Marker organization intends to remain a fully decentralized project and has committed to the first 13 Maker Improvement Proposals (MIPs) introduced in April 2020. MakerDAO hopes to remain a top influencer in the DeFi space and is also working on improving the bridge from layer 2 solutions, like Optimism, back Ethereum layer 1 main chain.

MakerDAO will be launching a version of DAI on Optimism L2. Currently, Optimism requires a 7 day lockup period before a user can withdraw tokens back to the Ethereum base layer.Maker can reduce this lockup period and allow near-instant withdrawals of DAI by minting a token (fDAI) which represents a claim on the L1 DAI through a vault. After the 7 day period and finalization of the state on L2, fDAI can be closed out and the vault loan repaid with interest. In effect, Maker will create a constant flow of 1-week duration loans flowing out of Optimism and back into L1. The initial bridge looks to launch in Q2 2021 with the fast withdrawals in Q4 2021.