You are reading an excerpt from our free but shortened abridged report! While still packed with incredible research and data, for just $20/month you can upgrade to our FULL library of 50+ reports (including this one) and complete industry-leading analysis on the top crypto assets.

Becoming a Premium member means enjoying all the perks of a Basic membership PLUS:

- Full-length CORE Reports: More technical, in-depth research, actionable insights, and potential market alpha for serious crypto users

- Early access to future CORE ratings: Being early is sometimes just as important as being right!

- Premium Member CORE+ Reports: Coverage on the top issues pertaining to crypto users like bridge security, layer two solutions, DeFi plays, and more

- CORE report Audio playback: Don’t want to read? No problem! Listen on the go.

TradFi vs. DeFi

Traditional finance (TradFi) was established based on lending and borrowing practices, forming the backbone of economic growth and financial stability for generations. In recent years, however, significant technological advancements have allowed decentralized finance (DeFi) to rise, emerging as a transformative take on finance through the permissionless and trustless nature of blockchain ledgers.

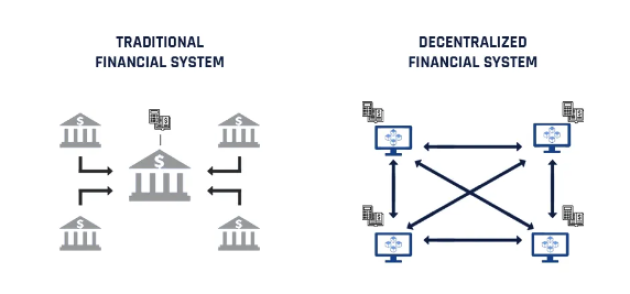

TradFi revolves around the essential roles of banks and financial institutions as intermediaries. They facilitate the movement of funds and engage in the critical task of assessing borrower's creditworthiness. Market conditions, central bank policies, and macroeconomic factors dynamically influence interest rates in TradFi. They are integral to the symbiotic relationship between lenders seeking returns and borrowers needing capital.

DeFi, led by protocols like Aave, disrupts this traditional model by enabling peer-to-peer or peer-to-protocol transactions through smart contracts. This eliminates the need for traditional intermediaries. Interest rates in DeFi are determined algorithmically based on supply-demand dynamics, utilization ratios, and protocol-specific methodologies. These rates are frequently adjusted to align with current market conditions.

While TradFi and DeFi lending systems have distinct characteristics and benefits, the evolution toward a more inclusive and transparent financial future is evident. DeFi, with its innovative use of blockchain technology and smart contracts, offers a compelling alternative to the traditional financial model, promising to reshape the landscape of global finance.

Borrow/Lending Mechanics

Lending, at its core, is a contractual agreement where one party, the lender, provides assets to another, the borrower, with the expectation of future repayment, often with interest. This setup compensates the lender for the risk of the transaction, with the aim that the returned amount exceeds the initial loan. Government and corporate bonds exemplify traditional models based on trust in the borrower's repayment promise.

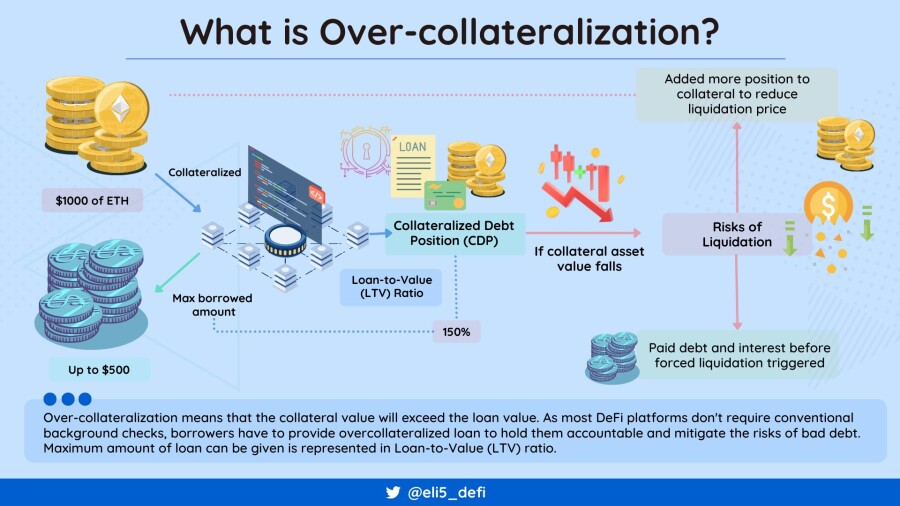

Contrastingly, in the realm of blockchain and cryptocurrencies, anonymity complicates trust-based transactions. Here, loans require collateral exceeding the loan value (over-collateralization), safeguarded by algorithms or smart contracts, thus eliminating counterparty risk and streamlining costs. However, this innovation brings its own set of challenges, notably smart contract vulnerabilities, capital efficiency problems, and the need for protocols to navigate hostile digital environments.

Nevertheless, a loan, in its simplest form, allows one to leverage their assets to generate additional cash flow or increase market exposure. Historically, lending has been a pivotal practice dating back to ancient civilizations. It underpinned economic development, with Sumerian temples devising the concept of loans and credit.

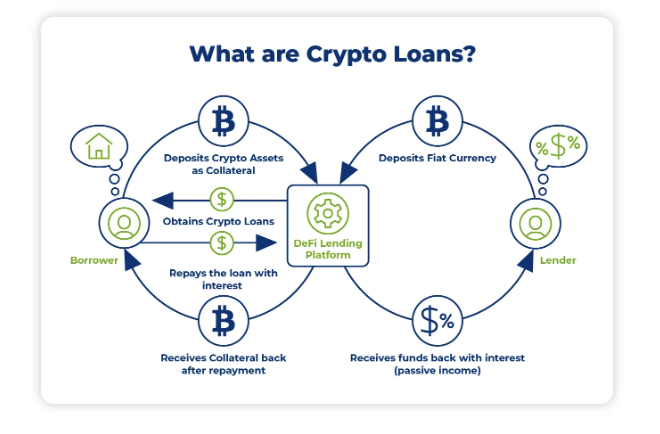

DeFi lending presents a transparent and straightforward approach compared to traditional systems. A user deposits an asset and borrows against it up to the protocol's stipulated Loan-to-Value (LTV) ratio. Interest is then paid for borrowing, typically driven by supply, and these payments are funneled to the lenders providing the assets. However, crypto's inherent volatility can make the process risky, leading to liquidation if borrowed too aggressively and collateral prices drop.

Lending protocols have gained popularity in DeFi due to the potential passive income they provide. Users deposit their assets and earn yields, which increases their cryptocurrency holdings over time. Additionally, lending allows for greater market exposure. Traders often borrow assets to leverage their positions, making it a favorite tool among investors.

In DeFi, the borrow/lend system operates peer-to-peer, primarily facilitated by smart contracts on blockchain networks. This decentralized approach eliminates the need for traditional financial intermediaries like banks, making the process more direct, efficient, and accessible.

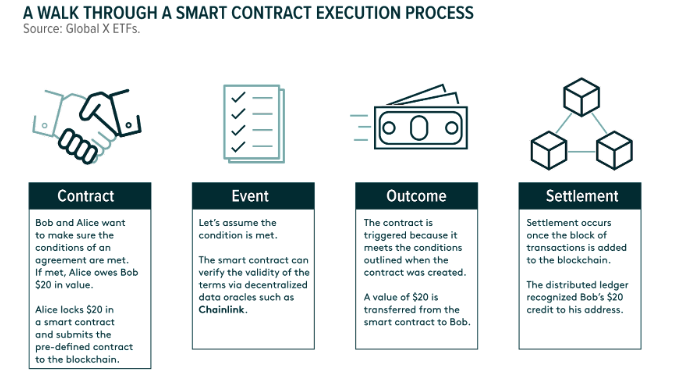

Transactions in DeFi lending and borrowing are managed and executed by smart contracts. These automated, self-executing contracts with pre-defined rules ensure transparency, security, and trust in the absence of centralized authorities.

A key feature of these DeFi lending agreements, as mentioned previously, is the requirement for over-collateralization. Borrowers must lock in collateral, typically in the form of cryptocurrencies, that exceeds the value of their loan.

This mechanism mitigates the risk of default, which is particularly pertinent given the absence of traditional credit scoring systems in DeFi. However, there are many valid criticisms that the model is inherently inefficient. For example, say someone would like to borrow $1,000 in a stablecoin like DAI. Depending on the associated collateral requirements, that individual may have to put up $1,500 in value as collateral. This is to say that while over-collateralization does enable peer-to-peer lending over blockchains, there are sure to be more capital-efficient methods moving forward as technology improves.