If you want more cryptocurrency analysis including full-length research reports, trading signals, and social media sentiment analysis, use the code "Publish0x" when subscribing to CryptoEQ.io to make your first month of CryptoEQ just $10!

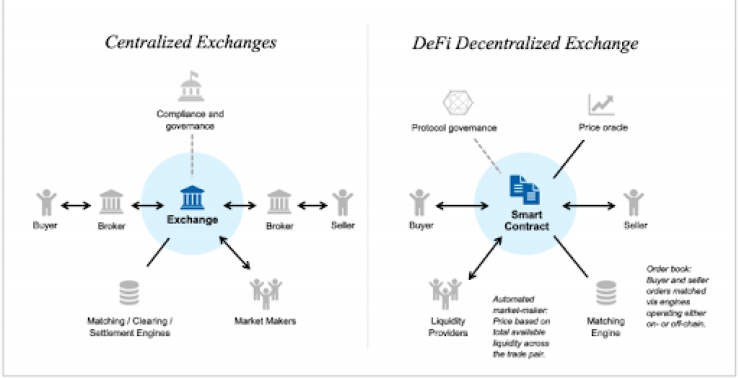

Uniswap is one of the largest decentralized exchanges and automatic market makers built on Ethereum. An automated market maker (AMM) is a specific type of DEX that relies on a mathematical formula to price assets instead of an order book where buys and sells are matched like on Coinbase or Gemini. Traditional market-making utilizes giant firms with extensive resources to create a tight bid-ask spread on an order book exchange. Automated market makers decentralize this process, enabling anyone to create a market for any two tokens on a blockchain. Prices discovery is purely mathematical.

DEX vs CEX. Image credit: Wharton

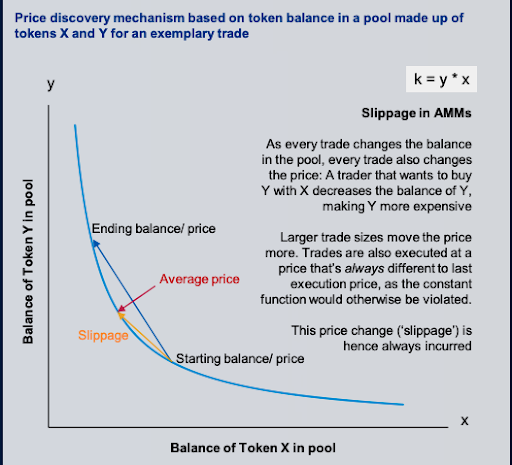

Uniswap works on a Constant Product Market Maker model that ensures the product of the two asset in the pool must always remain constant while the price for trading against the pool is based on the ratio of the two tokens to each other. In order to enable anyone to provide liquidity and earn fees on any assets, Uniswap uses a mathematical formula to rebalance liquidity providers' deposits. Uniswap uses the formula x * y = k.

- x is the amount of one token in the liquidity pool

- y is the amount of another

- k is a fixed constant

Both x and y are rebalanced based on their price and liquidity variations to one another. The goal is for the value of k to remain constant, despite these changes and split 50/50 between both assets in the pool. Essentially, the ratio of value between the two tokens must always remain the same.

Liquidity providers (LPs) add funds to the AMM pool which creates the market for each trading pair. LPs will deposit an equivalent value of two tokens e.g. 50% ETH and 50% AAVE to the ETH/AAVE pool. When a trader draws from that liquidity pool, the mathematical formula will set the price so that the balance of ETH-AAVE remains in balance.

The advantage of the x*y=k formula is that it enables liquidity at infinitely high or low prices of each asset since neither asset can ever be fully depleted. The disadvantage is that the relationship between x and y is not linear but rather asymptotic as shown in the chart below. This results in very high slippage once prices move into the more extreme ends of the curve. If the ratio of the assets in the pool changes by a wide margin, execution prices suffer and slippage increases.

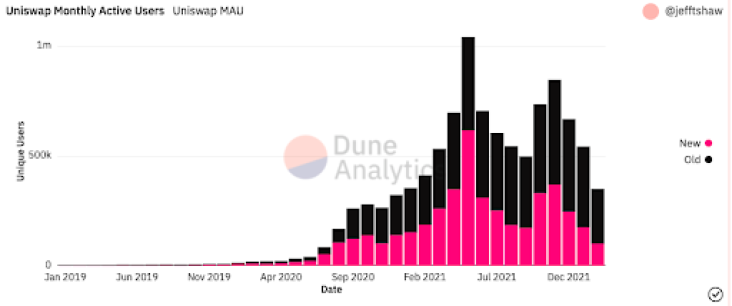

The most popular liquidity pairs on Uniswap include WETH/USDC, WETH/USDT, and WETH/WBTC. Uniswap boasts monthly active users in the hundreds of thousands, leading the DeFi DEX industry.

Uniswap v2

As previously discussed, Uniswap originally launched in 2017 but has since released updated versions of the protocol. Uniswap V1 set the foundation of on-chain token swaps and decentralized liquidity pools that rewarded users for providing liquidity of underlying token pairs, such as DAI to ETH or DAI to USDC. Uniswap V2 introduced ERC-20 to ERC-20 token swaps, a price oracle, flash swapping (allowed you to withdraw any ERC-20 token at no upfront cost), and support of non-standard ERC-20 tokens. Uniswap V3 (discussed later) introduced concentrated liquidity, multiple fee tiers (allows liquidity pools to be appropriately paid for taking on risk), and 4000x capital efficiency (allowing earning higher returns on equity).

The number of daily traders in 2021on Uniswap v2 mostly ranged between 30,000 and 60,000, peaking in May 2021 at ~100,000. After the H1 peak, the number of daily traders declined substantially and mostly stayed there. This can be attributed to the release of v3 as well as the rise in alt-L1 DeFi thanks to Ethereum’s rising gas fees. However, in 2021, the USDC/WETH pool, the most active v2 pool, facilitated nearly $30B worth of trades, exclusively through V2.

Uniswap v3

There are two significant differences that V3 introduces in its design: concentrated liquidity and multiple fee tiers. On Uniswap V2, users provide liquidity evenly along all of its markets’ price curves. This is somewhat inefficient since there does not need to be equal amounts of liquidity for ETH at $1 vs $3500.

The concentrated liquidity gives individual liquidity pools control over what price range their funds are allocated to. This allows for individual positions to be fused together into a single pool to make one combined curve for traders to trade against. Liquidity pools can focus capital within a custom price range so pools can provide larger amounts of liquidity at desired prices. This mechanism allows for individualized price curves and increases the customizability of liquidity positions. In doing so, traders can trade against the combined liquidity pool of all curves with no gas increase per liquidity provider. Trading fees are then collected and dispersed at a given range appropriately.

Multiple fee tiers allow for liquidity pools to be compensated for taking risks. There are three fee tiers per pair: 0.05%, 0.30%, and 1%. These options make sure that liquidity pools are customized to their margins according to certain pair volatility of the tokens. This may lead to some liquidity fragmentation, but the Uniswap team believes that most pairs will calibrate to an appropriate fee tier. Uniswap expects for liquidity pools to take more risk on non-correlated pairs like ETH/DAI and to take on less risk in correlated pairs like USDC/DAI. Correlated pairs are expected to sit at around 0.05% fees and .30% fees for pairs like ETH/DAI. 1% swap fees will be more appropriate for riskier pairs. Fees in V3 are more flexible and can be turned on by governance for each pool; these fees can be between 10% and 25% in liquidity pools fees.