If you want more cryptocurrency analysis including full-length research reports, trading signals, and social media sentiment analysis, use the code "Publish0x" when subscribing to CryptoEQ.io to make your first month of CryptoEQ just $10! Or just click the button above!

Maker Strengths

- Maker is one of the first DeFi projects and still currently boasts one of the highest total value “locked” (TVL) in a DeFi application at ~$19 billion.

- DAI is the leading decentralized, permissionless, trustless stablecoin that plays an integral role in Ethereum’s DeFi ecosystem with ~$9 billion in circulation. It remains the top choice for anyone looking to transact in a stablecoin without a trusted third-party.

- Over 400 apps and exchanges now use DAI and DAI has become a common trading pair within the DeFi ecosystem.

- Maker continues its commitment towards the full decentralization of MakerDAO with the return of 84,000 MKR tokens from its development fund to MakerDAO's governance module in Q2 2021.

Maker Weaknesses

- The historic March 2020 Ether price collapse and subsequent network congestion proved to be a long-tail systemic risk to Maker at the time. The system essentially did not perform as intended and allowed some users to lose all their collateral.

- The issuance of new MKR after the fallout of March 2020 undid years of MKR value accrual and also illustrated the possibility of future MKR holder dilution in the future.

- Regulatory clarity around the MKR token is non-existent but a strong case can be made for it to be deemed a security under the US Howey Test.

- In a move to reduce dependence on solely Ether, Maker now accepts multiple assets as collateral, including centralized stablecoins and assets. Introducing centralized collateral may reduce price volatility but opens up new censorship attack vectors.

- Because DAI’s stability is predicated on over-collateralization and incentive mechanisms within the Maker system, it exhibits more volatility than its fiat-backed counterparts and rarely trades at exactly $1.

Economics

Maker (MKR) is the governance token of the MakerDAO and Maker Protocol— a DAO and a software platform, respectively. Both are based on the Ethereum blockchain— which allows users to issue and manage the DAI stablecoin. Initially conceived in 2015 and fully launched in December 2017, Maker is a project with the task of operating DAI, a community-managed decentralized cryptocurrency with a stable value soft-pegged to the US dollar. MKR tokens act as a kind of voting share for the organization that manages DAI. While Maker does not pay dividends to its holders, it does give the holders voting rights over the development of Maker Protocol.

MKR is an ERC-20 token, meaning that it runs on and is secured by the Ethereum blockchain. Ethereum, in turn, is secured by its Ethash proof-of-work function and is subject to the gas fees of the Ethereum network. As of Q4 2021, ~2.5% of the ETH supply is locked up in Maker.

From the origination of the Maker project, the first iteration of DAI was known as Single Collateral DAI (SCD) because it had only one asset serving as collateral, Ether. SCD was launched in December 2017 and served as the only widespread stablecoin alternative to the “usual” company-backed stablecoin projects like USDT and USDC. DAI’s decentralized, permissionless features allowed it to become an integral piece of the Decentralized Finance (DeFi) ecosystem, the industry that seeks to build decentralized financial products on top of smart contract-enabled blockchains, eliminating middlemen and rent-seeking entities.

In November 2019, MakerDAO upgraded the protocol to transition from Single Collateral DAI (SCD) to Multi Collateral DAI (MCD) by adding Basic Attention Token (BAT) as additional collateral outside of just Ether. Since then, Maker has added more custodial/less decentralized assets like USDC, WBTC, TUSD, PAX, and USDT.

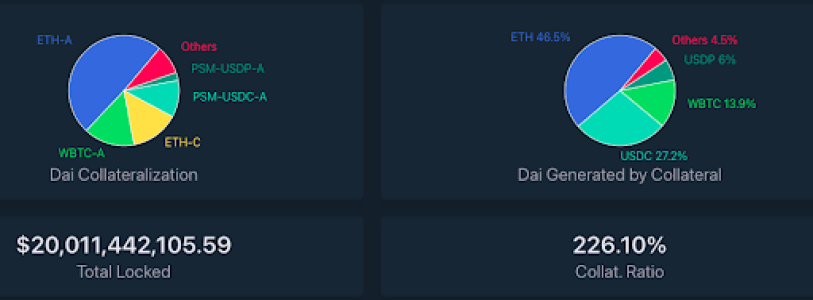

On the left is the total amount of collateral that is backing DAI and on the right is the DAI minted by different collateral types. Source: DAIstats

Additionally, the Maker community rolled out other important protocol changes like the introduction of the DAI Savings Rate (DSR) which allows DAI holders to earn yield. DAI holders can also deposit DAI into other DeFi loan dApps to earn yield. DeFi Score by Codefi, lists DAI yields as high as ~18%. However, DeFi rates are typically highly variable based on current liquidity and demand, with historical rates much closer to ~5%.

In April 2021, MKR governance voted and passed an executive order that allows real estate assets as collateral in the form of an ERC-20 token. Two separate interest-bearing tokens will be created, DROP and TIN, as non-fungible tokens (NFTs) tied to individual deposits from New Silver, the real estate partner in this initiative. Adding real-world assets has always been on the roadmap for Maker and the new addition significantly increases the number of loans that can be produced as such a large market of collateral is now available.

All accrued fees on MakerDAO are paid in MKR. The protocol purchases MKR off the secondary market and burns it, ensuring proper alignment incentive between MKR token holders. The burning of MKR reduces its supply in circulation through its intentional destruction. It is an effective method for increasing and stabilizing the price of MKR with the increased value given to the holder resembling that of a dividend.

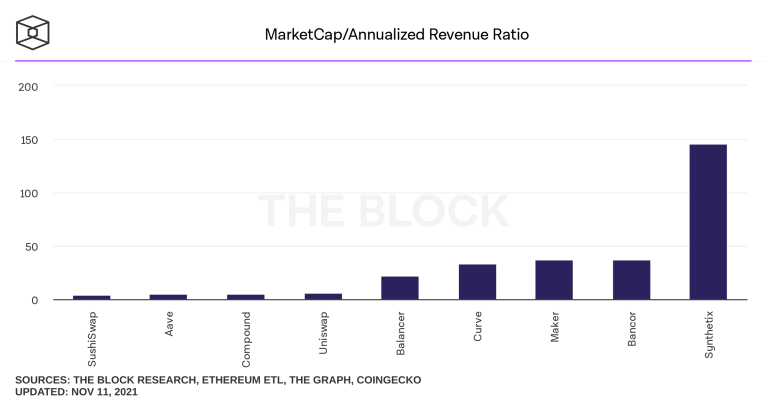

A comparison of DeFi "blue chips" and their market cap to revenue ratio. MKR remains comparable to peers in this regard with SNX being the outlier. Image credit: TheBlock

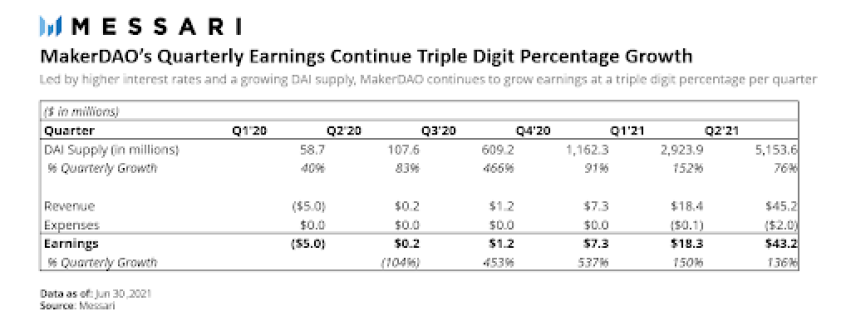

A significant milestone for MKR holders, Maker finally began raising interest rates away from zero in Q3 2020, translating to significant returns for MKR holders. Annualized earnings to MKR holders topped $27 million and in 2021 saw even more dramatic growth with projected annual returns of ~$200 million if all parameters remained steady throughout the remainder of the year.

MakerDAO earnings. Source: Messari

However, much of this growth has come with adding centralized assets as collateral, although this trend has reversed somewhat in the back-half of 2021. Nonetheless, centralization concerns remain. Greater than one-third of Maker’s collateral comes from centralized assets such as USDC and WBTC. While adding other collateral types helps with diversification and central downside risk, Maker could also be exposing itself to a new attack vector through its centralized assets. As of Q4 2021, ~40% of the DAI supply was generated by USDC and WBTC via the PSM. While, the majority of DAI is still backed by ETH, vaults created by the PSM with USDC only have liabilities against the DAI they created. This means that not all the ETH backing DAI necessarily backs each DAI liability.

MakerDAO hopes to create both a reliable stablecoin in DAI and a system of fair credit for everyone with the inclusion of MKR. Unlike other cryptocurrencies, MKR does not have a max token supply, predictable issuance schedule, nor “halving” event. The total supply is variable and dependent upon adoption and the amount of DAI loans issued.

Maker also did not hold an ICO. Instead, the project raised $12 million in venture funding led by Andreesen Horowitz and Polychain Capital in December 2017. MKR launched with 1 million MKR tokens and has distributed them to early adopters and through three private sales. The current circulating supply is 1,000,000 MKR as of Q2 2021.

DAI is rarely worth exactly $1 – it typically hovers between $0.98 and $1.02. Instead of mining, it’s issued by purchasing a collateralized debt position (CDP), Maker’s smart contracts that act as a loan. Once the loan is paid off (along with MKR fees), the DAI is destroyed as the smart contract is fulfilled.

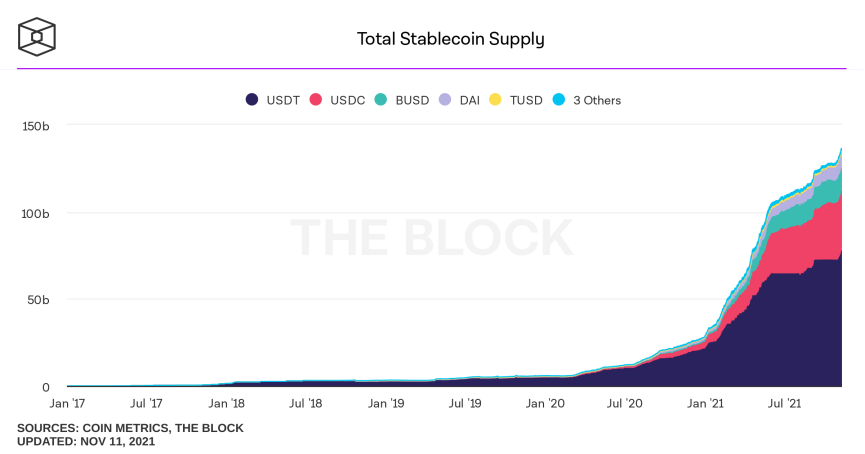

To purchase the DAI stablecoin, you need to convert your ETH to wrapped Ethereum (W-ETH). This is how decentralized exchanges like 0x enable exchanges between ETH and tokens on the Ethereum blockchain. As of Q4 2021, there are ~9 billion DAI in circulation. Stablecoins saw an incredible rise in 2020-21 on Ethereum and DAI was no exception. Tether’s USDT token settled $580 billion on Ethereum, Circle’s USDC stablecoin settled $239 billion on Ethereum, and DAI came in third settling $98 billion.

Image credit: TheBlock

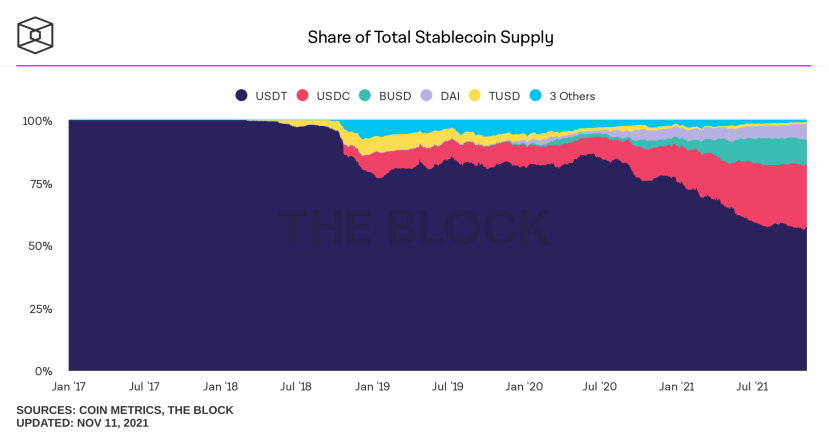

Since 2020, DAI has increased its market share in the stablecoin market. This led to DAI’s market share increasing from 3% to 7%. DAI also has the highest velocity of all stablecoins, in part due to its smaller size.

DAI percentage of overall stablecoin market. Image credit: TheBlock

Converting between MKR, DAI, and ETH is done on Oasis Direct, MakerDAO’s decentralized token exchange platform that also supports other ERC20 tokens on the Ethereum blockchain. Other exchanges like Radar Relay, HitBTC, Kyber, and Ethfinex also support DAI and MKR, and over $1 million worth of each is traded DAIly. Maker recently announced a partnership with AirSwap DEX, too.

MakerDAO creates DAI using Vault/CDP smart contracts to collateralize the assets. This means it’s backed by ETH instead of fiat currency and the CDPs ensure there’s always enough ETH assets on hand to cover the DAI supply. Essentially, CDP contracts hold ETH, and if a black swan event occurs such as ETH crashing before anyone has a chance to react, MKR is liquidated on the open market to cover the losses.

Such an event happened on March 13, 2020, dubbed “Black Thursday” discussed in further detail in the Vulnerabilities section. Afterward, Maker added USDC as another collateral type to try and become less dependent on ETH and its volatility. This allows the protocol to re-collateralize, increase DAI supply, and improve arbitrage incentives. After USDC, Maker added even more custodial/less decentralized assets like WBTC, TUSD, PAX, and USDT. Custodial assets represent about one-third of MakerDAO’s collateral base. This creates an issue within the DAI ecosystem. If DAI’s primary value proposition is that it’s permissionless and decentralized unlike USDC, USDT, etc. then adding centralized assets erodes some of DAI’s appeal.