You are reading an excerpt from our free but shortened abridged report! While still packed with incredible research and data, for just $20/month you can upgrade to our FULL library of 50+ reports (including this one) and complete industry-leading analysis on the top crypto assets.

Becoming a Premium member means enjoying all the perks of a Basic membership PLUS:

- Full-length CORE Reports: More technical, in-depth research, actionable insights, and potential market alpha for serious crypto users

- Early access to future CORE ratings: Being early is sometimes just as important as being right!

- Premium Member CORE+ Reports: Coverage on the top issues pertaining to crypto users like bridge security, layer two solutions, DeFi plays, and more

- CORE report Audio playback: Don’t want to read? No problem! Listen on the go.

Liquidity

Liquidity is indispensable for the operation of DeFi protocols. Consider Aave, the largest lending protocol in the DeFi space. Aave comprises a supply side that provides liquidity and a demand side that pays interest on loans distributed to liquidity providers.

Aave's pool functions as a utility, allowing borrowers to leverage their existing assets. Without suppliers in the pool, borrowers would have no assets to access, rendering the pool non-functional. Similarly, when the pool's utilization rate reaches 100%, suppliers can no longer withdraw their assets, and borrowers cannot take out loans. In such cases, the pool loses its functionality.

To maintain its functionality, Aave relies on liquidity. The more capital it attracts, the better its utility becomes. However, many DeFi protocols face a challenge known as the "cold-start problem," where attracting sufficient liquidity initially is a hurdle. Liquidity is crucial for functionality and security. When protocols surpass a liquidity threshold, typically a few million dollars, they gain legitimacy and become established. The prevalence of incentives in attracting liquidity underscores its importance to investors.

Enhancing liquidity efficiency allows protocols to share market liquidity, providing sufficient functionality to each viable protocol. This widens the range of choices available to users, fosters competition, and expands DeFi's overall use case.

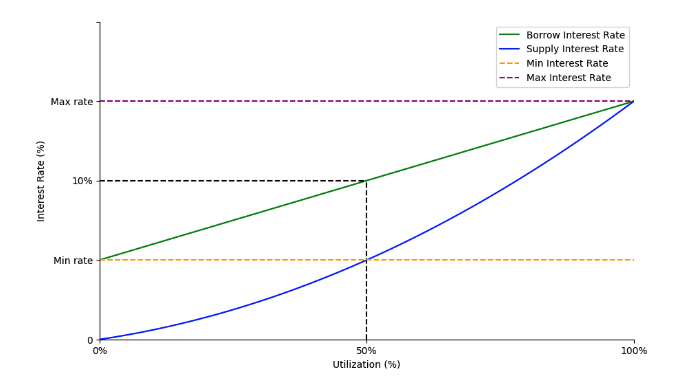

Aave employs a dynamic interest rate model that encourages market participants to be more efficient. When the utilization rates are high, the supply annual percentage rate (APR) naturally increases, motivating users to deposit funds. Similarly, the borrow APR spikes, compelling users to repay their borrowed funds. This financial mechanism promotes better efficiency in capital allocation, and similar mechanisms can be observed across the DeFi landscape, encouraging market participants to act with increased efficacy.

Furthermore, liquidity efficiency benefits users by improving their yield. Modern protocol business models can be simplified into three constituent parts: the supply side, which offers a service in the form of liquidity; the demand side, which pays for the service; and token holders, which receive financial dividends. Higher liquidity efficiency leads to increased revenue for the supply side, more cost-effective services for the demand side, and better returns for token holders.

Lending/Liquidity Pools

A lending pool is an essential component of DeFi protocols, functioning as a smart contract that allows users to deposit assets, typically ERC20 tokens, with the intent of lending these assets to other users. Borrowers, on the other hand, can interact with the lending pool by depositing collateral assets, enabling them to secure instant loans.

Compared to traditional finance, DeFi lending pools offer significant advantages, such as:

- DeFi lending is not restricted by the 1:1 availability of funds for loans. Instead, a lending pool aggregates deposits from multiple users, creating a substantial inventory of tokens to accommodate loans on demand.

- DeFi eliminates the need for rigid repayment schedules. Loans are issued against collateral, and borrowers have the flexibility to repay their loans whenever they choose.

A natural question arises: why would someone borrow assets in a DeFi lending protocol if they have to provide equally valued (or even overvalued) assets as collateral? The answer lies in the unique trading methodology enabled by DeFi lending protocols: leverage.

Suppose you have a bullish outlook on Wrapped Bitcoin (WBTC) and are confident its value will surge. You could deposit WBTC (e.g., $100 worth) into a lending protocol, borrow a stablecoin such as USD Coin (USDC), and use the borrowed funds to purchase more WBTC (e.g., $50 worth). In this case, your exposure to WBTC would increase to $150 from an initial $100 investment. Furthermore, you could deposit the additional WBTC as collateral to borrow even more USDC, a process known as over-leveraging, until the protocol's borrowing power limits are reached.

Conversely, if you have a bearish outlook on WBTC, you could deposit USDC as collateral, borrow WBTC, and exchange it for more stablecoins. If WBTC's price drops as predicted, you can repurchase the borrowed amount at a lower cost, repay the loan, and keep the excess USDC, effectively opening and closing a short position on WBTC.

To incentivize users to maintain their deposits in lending pools, interest is accrued over time as a percentage of a user's deposit, calculated by the protocol. As users' assets remain in the lending pool, their interest accruals increase. The protocol must account for each user's share of the pool without actively updating the shares of other users, as doing so on-chain would be inefficient and costly for depositors.

To address this issue, DeFi protocols employ issuing interest by minting and burning ERC20 tokens, referred to as "Pool Tokens," which represent a lender's proportion of deposited assets in the lending pool. This "pool token" design automatically adjusts the share dilution of other "shareholders" to reflect the minting and burning of "shares" in proportion to the deposit or withdrawal of their underlying assets.