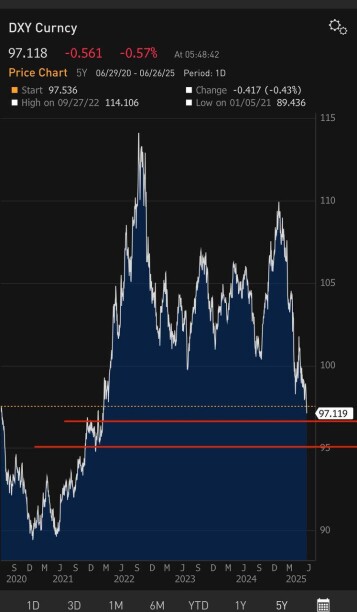

The Signal is Clear: The US Dollar Index (DXY), the benchmark measure of the greenback's strength against a basket of major currencies, has decisively broken below critical multi-year support and continues its descent. As of today, it hovers around 97.1, marking levels not witnessed since the turmoil of Spring 2022. This isn't just a dip; it's a significant technical breakdown with profound implications for global markets.

Why This Dollar Weakness is Rocket Fuel for Risk Assets:

-

Global Liquidity Surge:

A weaker dollar acts as a massive liquidity injection into the global financial system. Why? The world is drowning in USD-denominated debt. When the dollar depreciates:-

Debt Burden Relief: The real value of debt owed by governments and corporations (especially in emerging markets like Brazil, India, or Turkey) decreases. This frees up capital and reduces default risks.

-

EM Breathing Room: Emerging markets gain crucial respite. Servicing dollar debts becomes cheaper, easing pressure on foreign reserves and potentially allowing for more accommodative domestic policies.

-

Capital Flight to Growth: Cheaper dollars incentivize capital to flow out of USD assets and into higher-yielding, higher-growth opportunities globally – stocks (especially EMs), commodities, and cryptocurrencies.

-

-

A Calculated Policy Move, Not an Accident:

This dollar weakness is far from random. In a world saturated with record levels of debt post-pandemic and facing slowing growth, policymakers are tacitly (or actively) encouraging a controlled devaluation:-

The "Lesser Evil": With traditional tools like Quantitative Easing (QE) potentially off the table for now or politically sensitive, a weaker dollar becomes a crucial lever. It effectively exports inflation and boosts the competitiveness of US exports.

-

Debt Sustainability: For the US itself, a weaker dollar makes its own colossal debt burden slightly more manageable over time. It's a delicate balancing act, but one clearly being pursued.

-

-

The Market's Crystal Ball: Front-Running the Flow:

Never underestimate the market's anticipatory power. Institutional capital moves on expectations, not lagging headlines. The current broad-based rally is the market pricing in the tidal wave of liquidity a falling DXY unleashes:-

Simultaneous Surge: Witness the synchronous strength – Bitcoin breaking resistance, global equity indices (S&P 500, Nasdaq, Euro Stoxx, Nikkei) pushing higher, industrial metals (Copper) and energy (Oil) finding bids. This isn't coincidence; it's the "Weak Dollar Trade" in action.

-

Gold's Double Play: Even traditional safe-havens like Gold benefit, as a weaker dollar makes dollar-priced commodities cheaper for foreign buyers and gold serves as an alternative store of value amidst currency depreciation concerns.

-

History Rhymes: The Blueprint for Rallies

Look back at pivotal market turning points:

-

Mid-2020: DXY peaked and rolled over. What followed? A historic, liquidity-fueled rally in everything – stocks, crypto, commodities.

-

Early 2017: A sustained DXY downtrend preceded the massive crypto bull run and strong global equity performance.

-

(Current) 2025: The DXY breakdown below the crucial Spring 2022 support level (around 98.00-98.50) is flashing the same potent signal. It's the market whispering: "Liquidity is returning; risk is back on."

Crucial Considerations & Potential Pitfalls:

-

The Fed Factor: Any surprise hawkish pivot from the Federal Reserve (delayed cuts, talk of hikes) could provide short-term support for the dollar, temporarily disrupting the trend.

-

Geopolitical Shockwaves: Major unforeseen events (escalating conflicts, systemic risk events) could trigger a "flight to safety," boosting the dollar rapidly.

-

Inflation Reacceleration? If falling DXY significantly fuels imported inflation in the US/EU, it could force central banks to maintain tighter policy for longer than markets currently expect.

Trading the Trend: Where to Look

-

Cryptocurrencies: The prime beneficiaries of excess liquidity and a "risk-on" impulse. BTC, ETH, major altcoins.

-

Emerging Market (EM) Assets: Equities (EEM ETF), bonds (local currency debt), currencies.

-

Commodities: Industrial metals (Copper - HG), Energy (Oil - CL, BZ), Agriculture (Corn, Wheat).

-

Non-US Equities: European (Euro Stoxx 50), Japanese (Nikkei), and other developed markets.

-

Gold (XAU/USD): As a hedge against dollar weakness and potential future inflation.

The Unmistakable Takeaway:

While volatility is inevitable, the current DXY trajectory is a powerful tailwind. As long as the dollar's downtrend holds, the path of least resistance for global risk assets – led by crypto and equities – is demonstrably higher. This is the historical playbook unfolding once more. Ignore it at your portfolio's peril. Monitor DXY levels (next major support near 95.00) and central bank rhetoric, but position for the liquidity wave.

![How Fear of Piracy [Destroyed] a 20-Year Tech Lead](https://cdn.publish0x.com/prod/fs/cachedimages/3731945950-5c99dbb082c081853735e98f1f9444ea30dc5a195fc83eee84721476c11215db.jpg)