The war is over, go in peace. In just a few hours, however, two key data points will arrive to clarify the state of the U.S. economy and, consequently, the global financial outlook. Indeed, on Thursday, we will receive the U.S. GDP figures (final Q4 2025) alongside extensive data on the labor market and inflation.

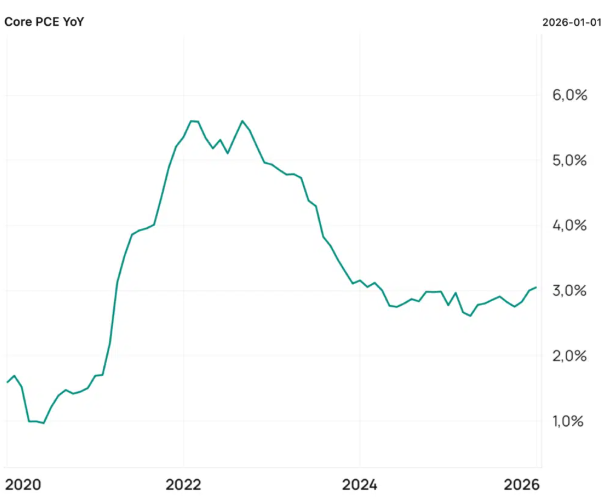

In fact, we will see the release of the PCE (Personal Consumption Expenditures), the index that measures consumer price movements: it is the most critical metric for the Federal Reserve when analyzing inflation trends. The data refers to February, therefore it does not include any potential increases caused by the war in Iran, and it is expected to remain at the same levels as January. We will also have the jobless claims, which have already provided several surprises in recent readings.

All the data for the next 24 hours: is tension rising again?

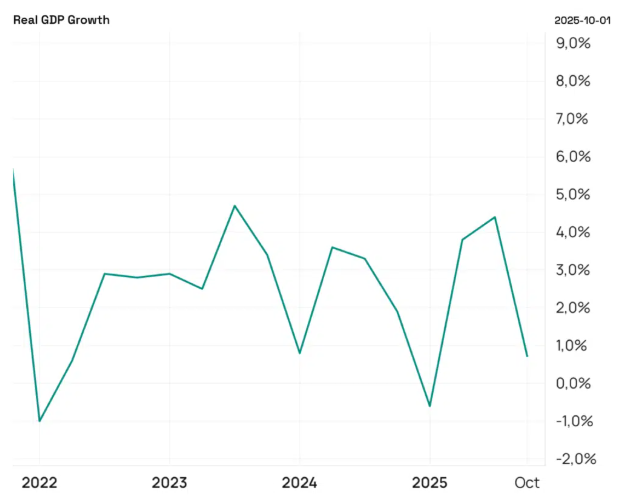

After moving past the war in Iran—at least for two weeks, as Alex Lavarello reported this morning in his 'Buongiorno Borse'—we can finally return our focus to macro data. Thursday, April 9th, will be a high-tension day, as we will see: U.S. GDP, final Q4 2025 reading This will be the definitive reading of the U.S. economy's performance in the final quarter of 2025. This figure has shifted multiple times during previous estimates. Finally, we will know the official result and gain a clear understanding of the actual performance of the U.S. economy. However, this is not the most important data point of the day.

Unemployment Claims These are a reliable gauge of labor market performance. Here too, we have seen significant swings over previous weeks, and it will be interesting to read the latest data, especially in relation to those from the last two months. The Federal Reserve continues to maintain a moderate level of concern regarding a potential downturn in U.S. labor market conditions. A reading that is worse than expected would provide even more reason for a rate cut. Markets will react as if this were the most important reading in the world. It isn't, but it is certainly worth following.

Forecast for new claims: 210k.

PCE

This is the most important data point. As we have noted multiple times on these pages, the PCE is the Fed’s benchmark index for assessing inflation trends. Among the various figures to be published on Thursday, the most interesting to follow will be the Core PCE YoY, which tracks price changes excluding energy and food (which are inherently highly volatile).

Forecasts: +3.0%

We are, as is evident, very far from the 2.0% target. To make matters worse—as pointed out by Williams—there are not only future concerns regarding oil prices but also more pressing issues stemming from tariffs. A lower-than-expected PCE reading would be welcomed with great enthusiasm by the markets.

Bitcoin and Crypto: Liquidity, Labor, and Recession

While markets might react more positively in the short term to a potential shift toward recession and a sluggish labor market, the best option for Bitcoin and crypto in the medium-to-long term is a slow return to normalcy. This return to normalcy should aim to avoid recessions, excessive shocks to the labor market, and the need for emergency rate cuts.

With inflation still running hot—having stayed above the target for more than five years—the path of emergency cuts would appear, in any case, to be an unfeasible route.